Download as PDF, PPTX

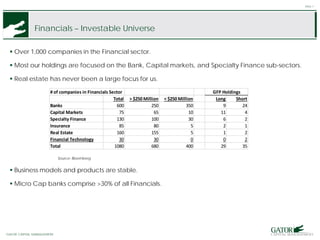

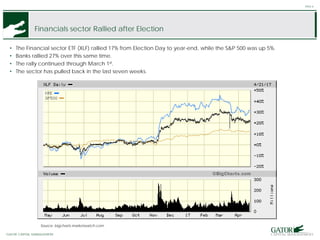

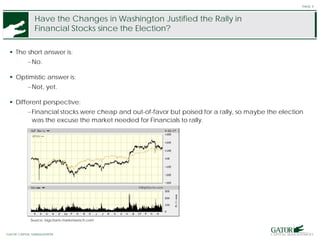

The document provides an overview and analysis of opportunities in the financial sector following changes in Washington. It summarizes recent performance of financial stocks, ways the sector could benefit from tax cuts, deregulation, higher interest rates, and economic growth. It then discusses attractive sub-sectors and provides details on potential long investments in financial guaranty firms, consumer finance, bank warrants, and alternative asset managers.