Download as PDF, PPTX

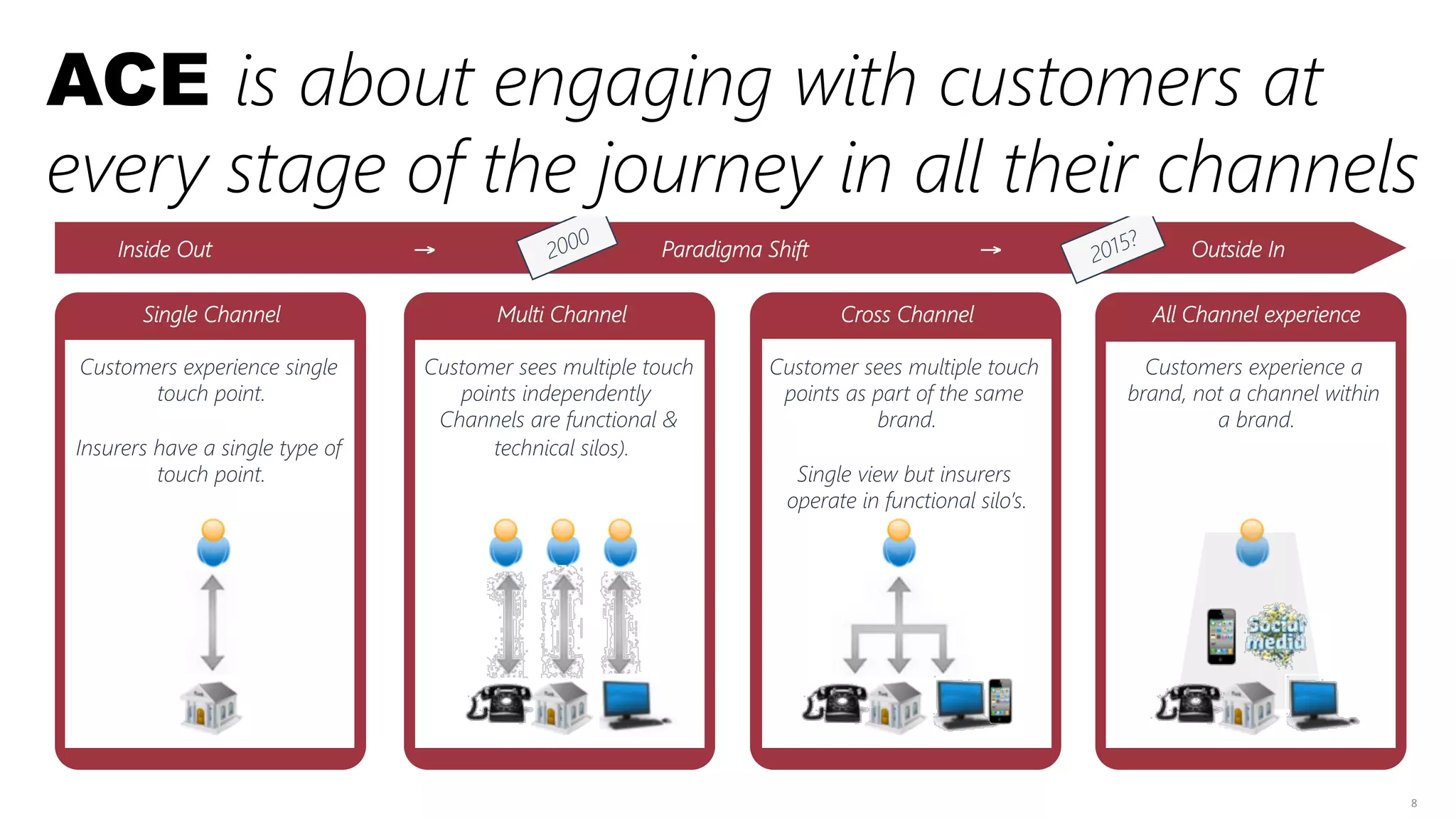

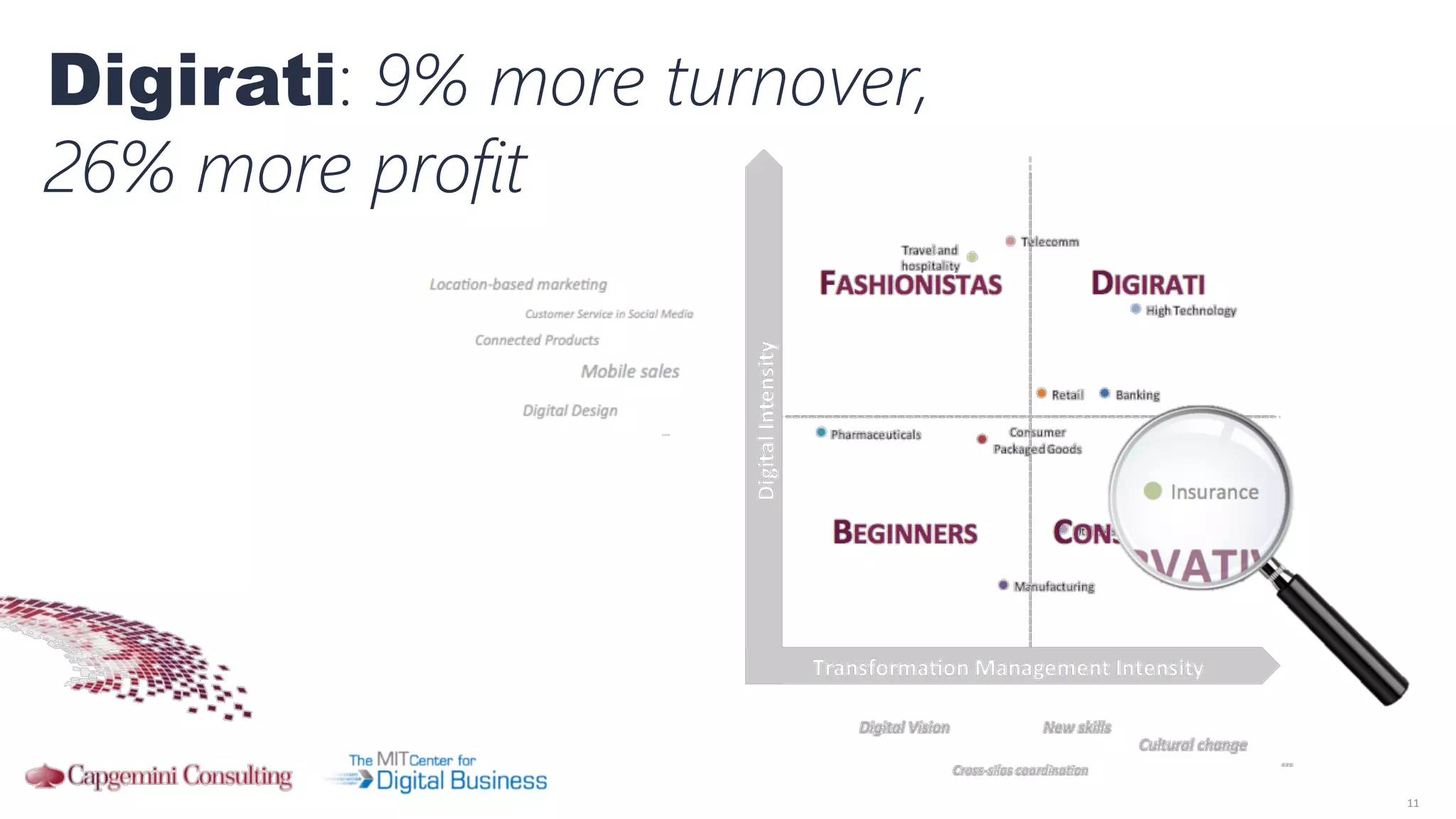

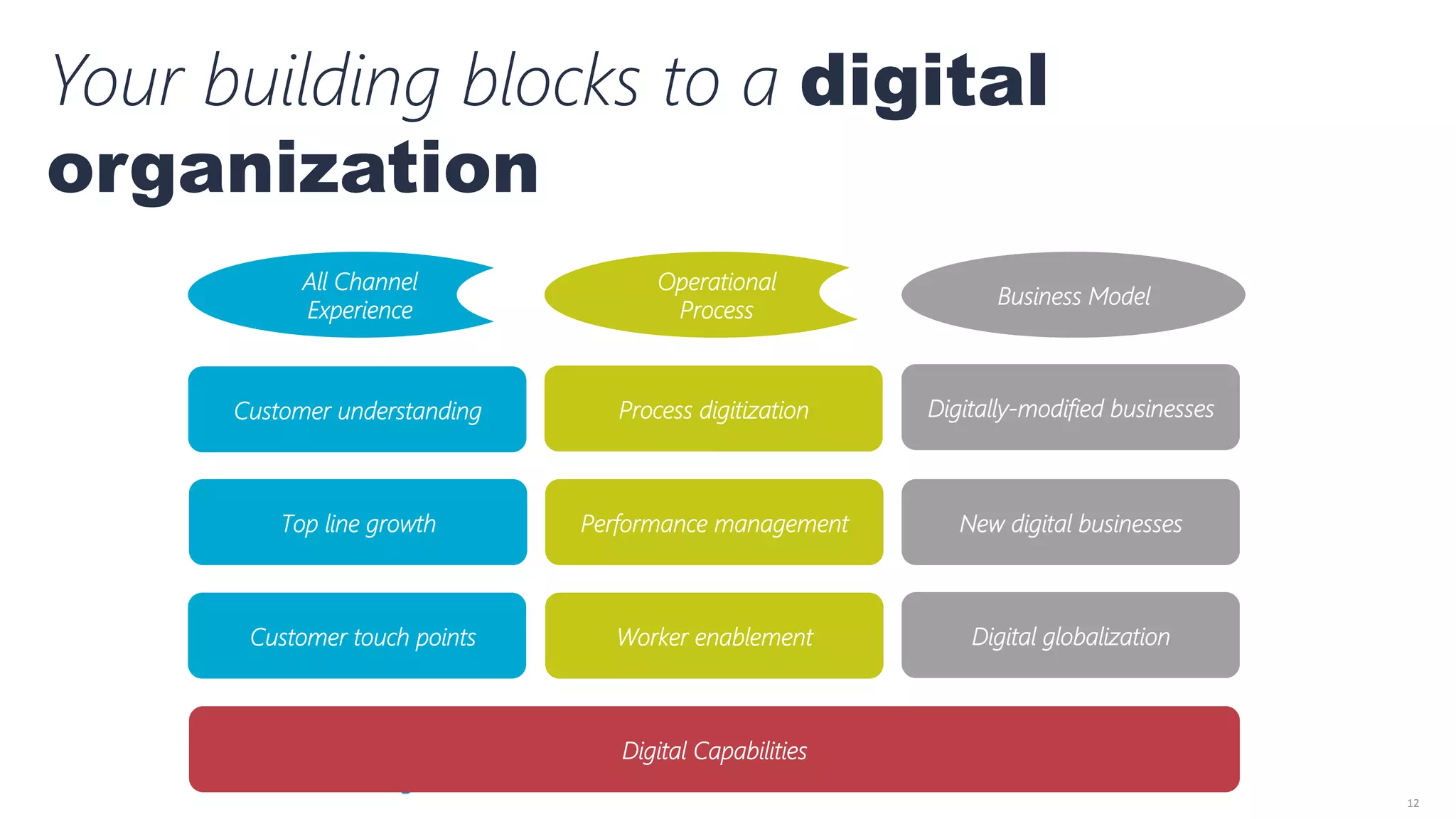

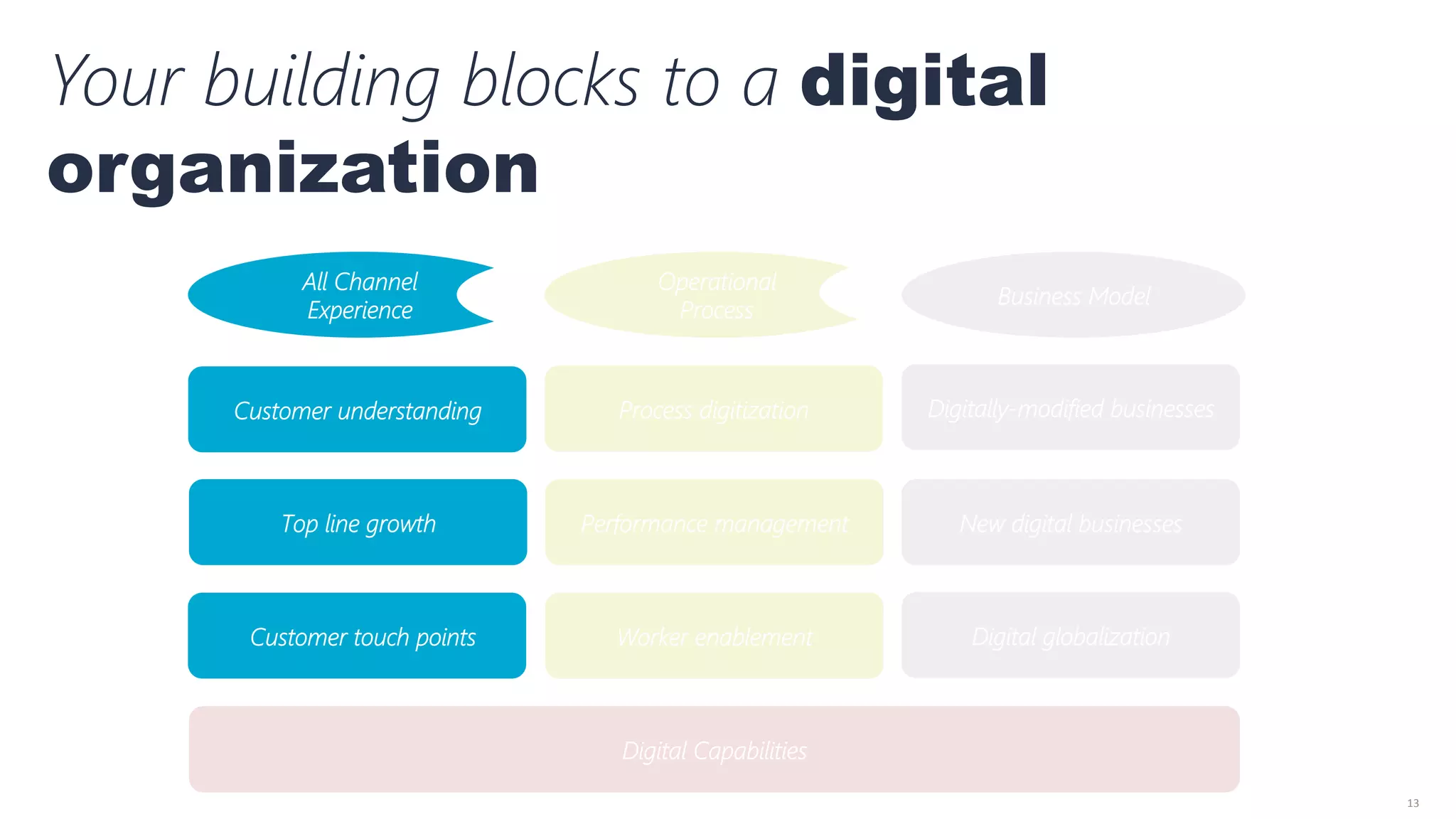

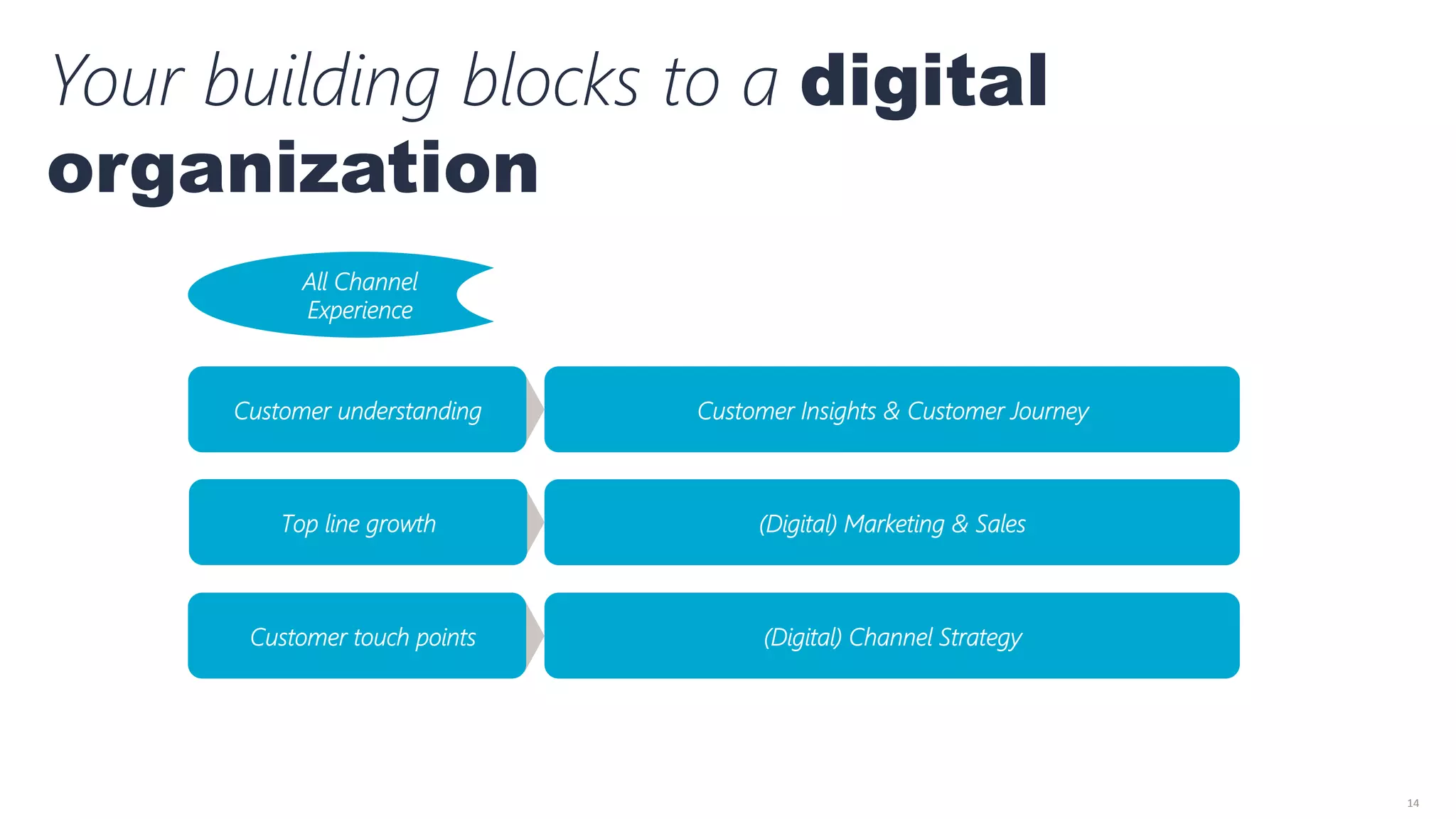

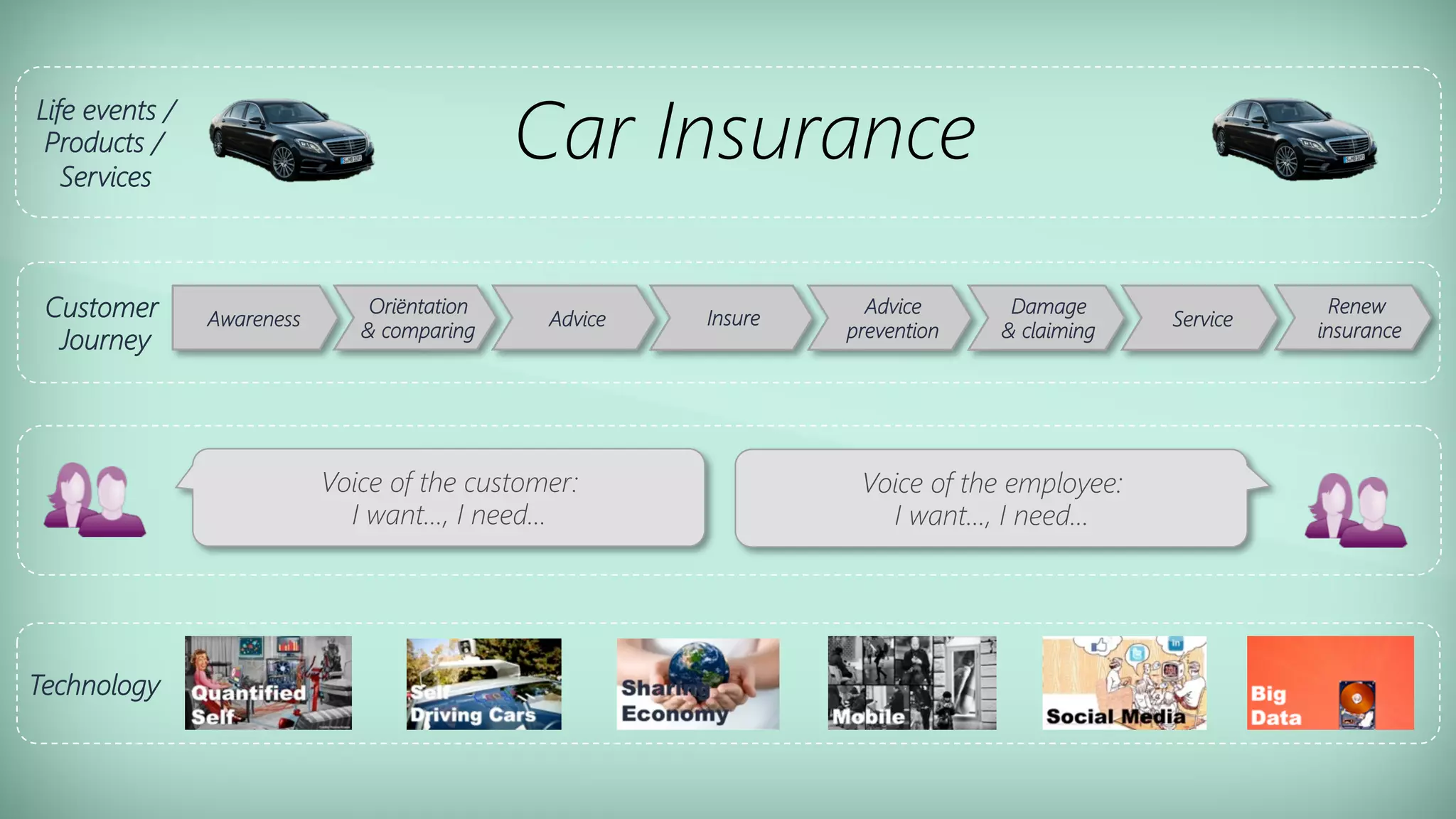

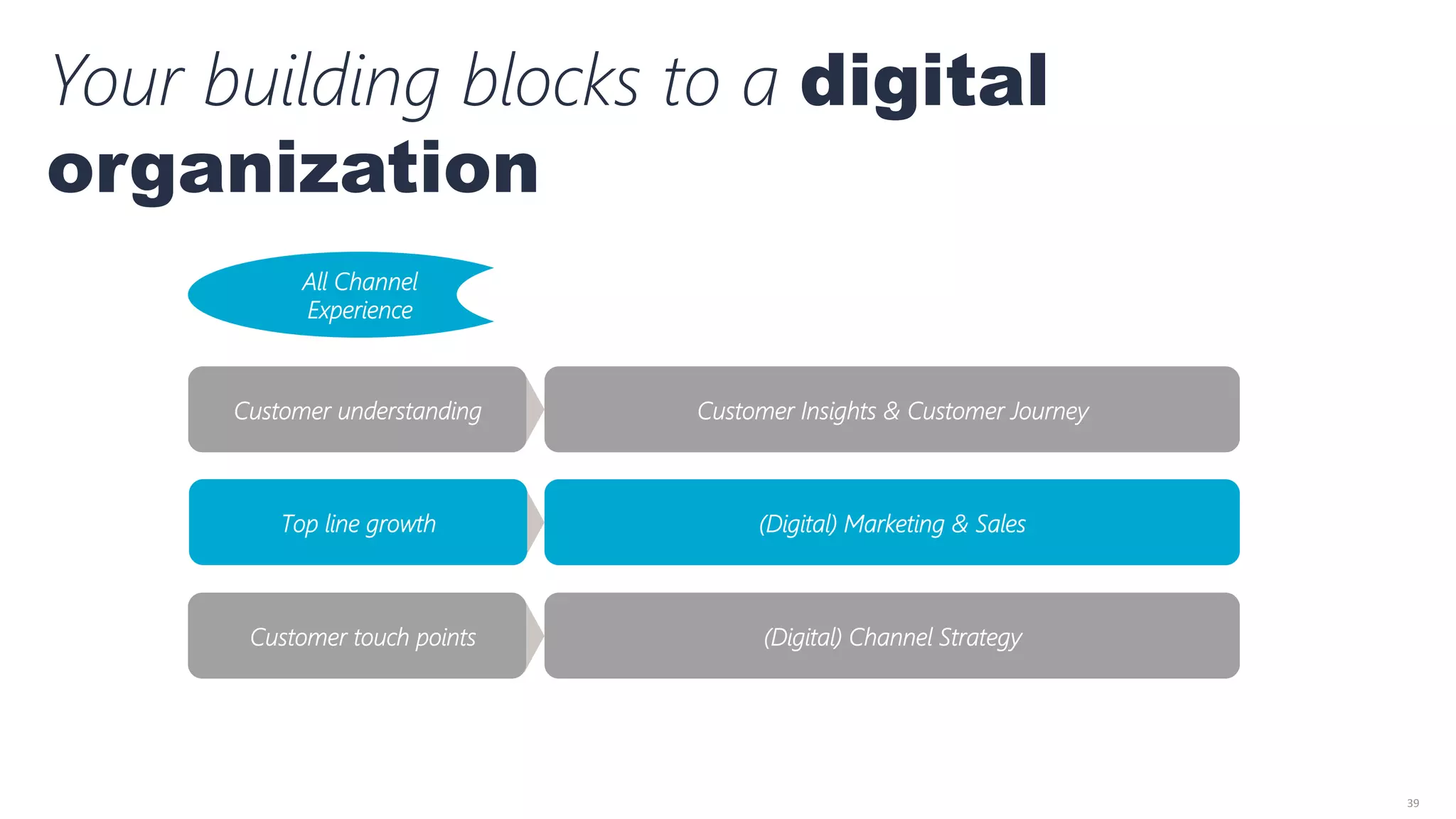

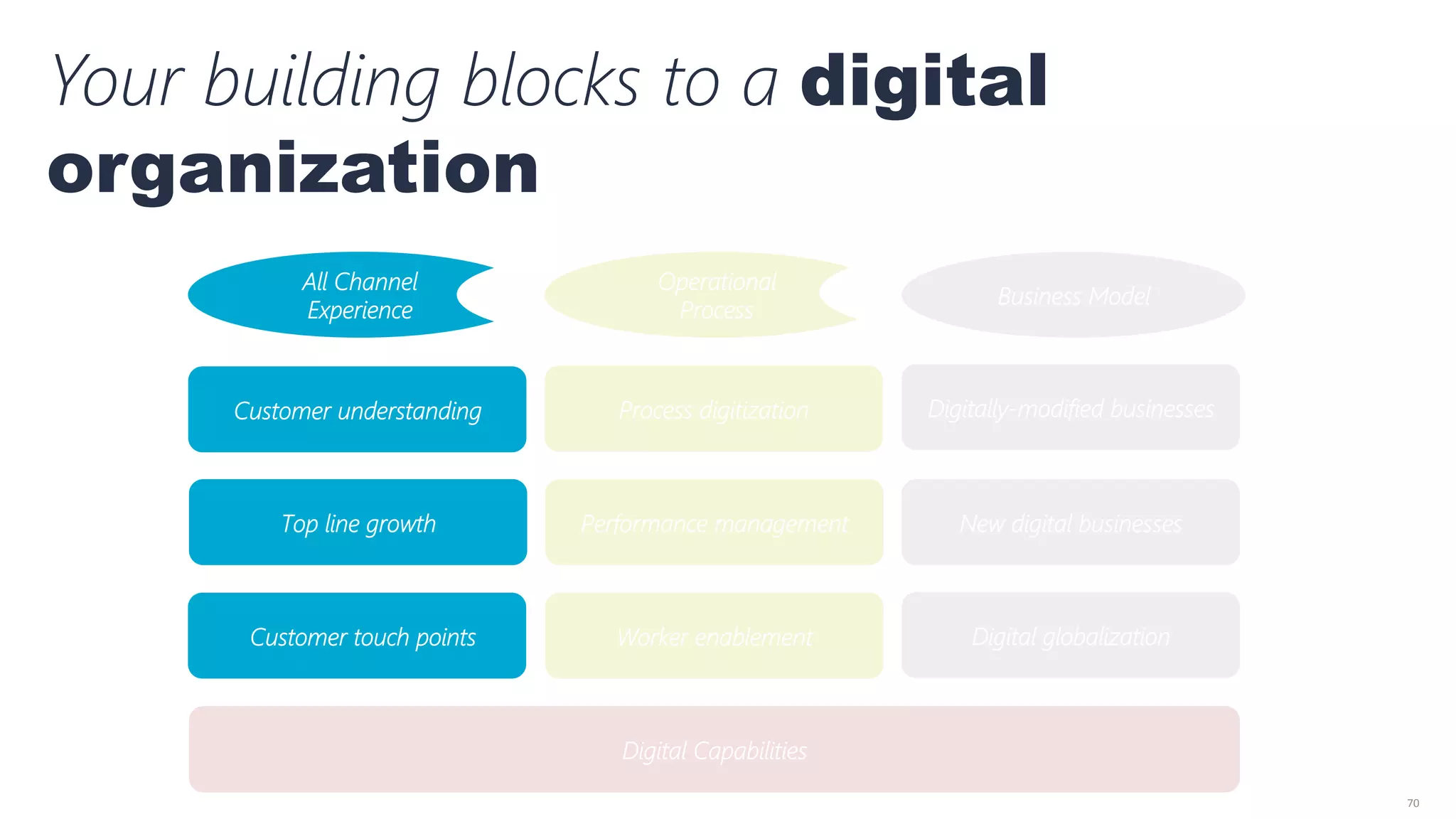

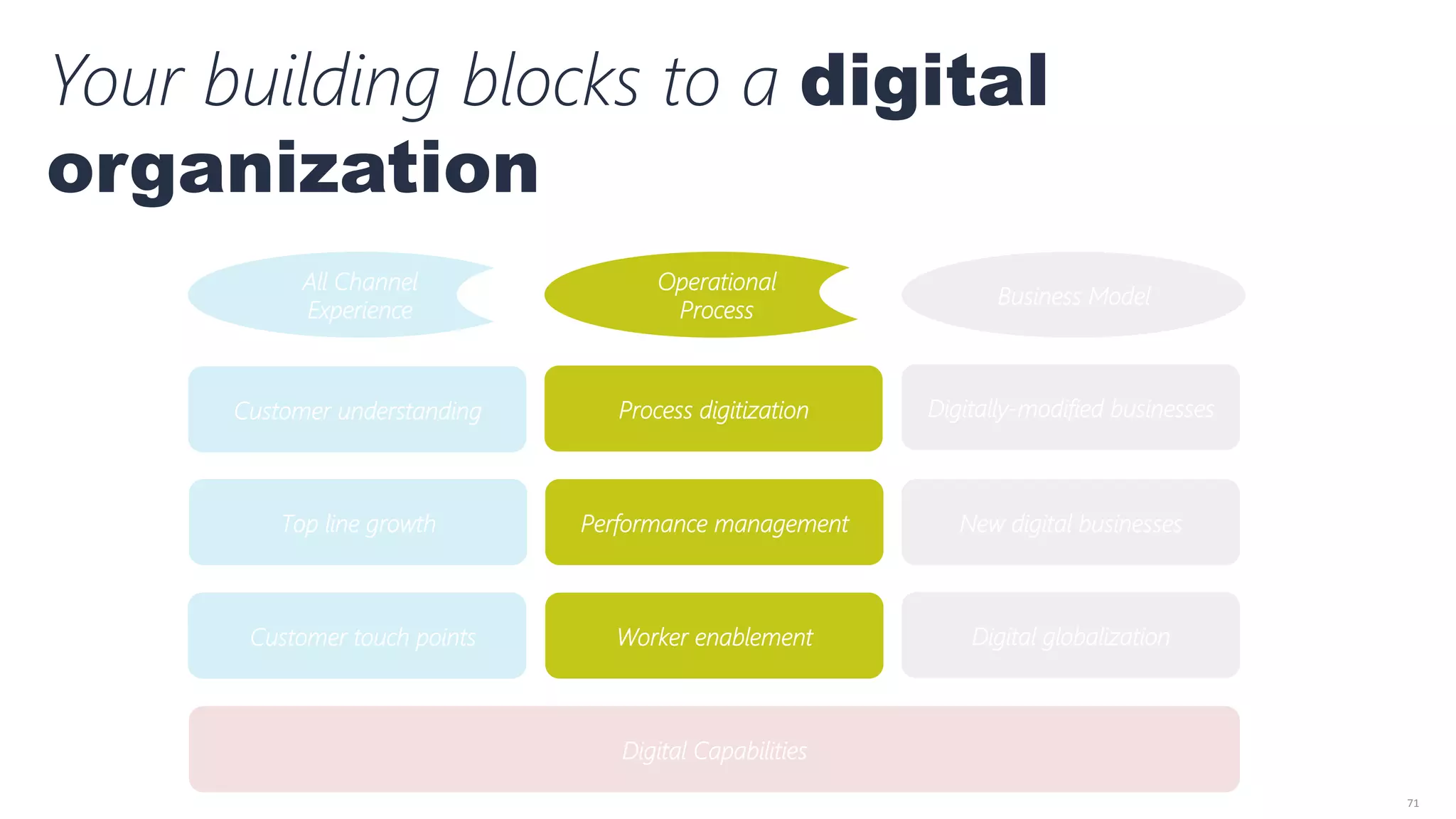

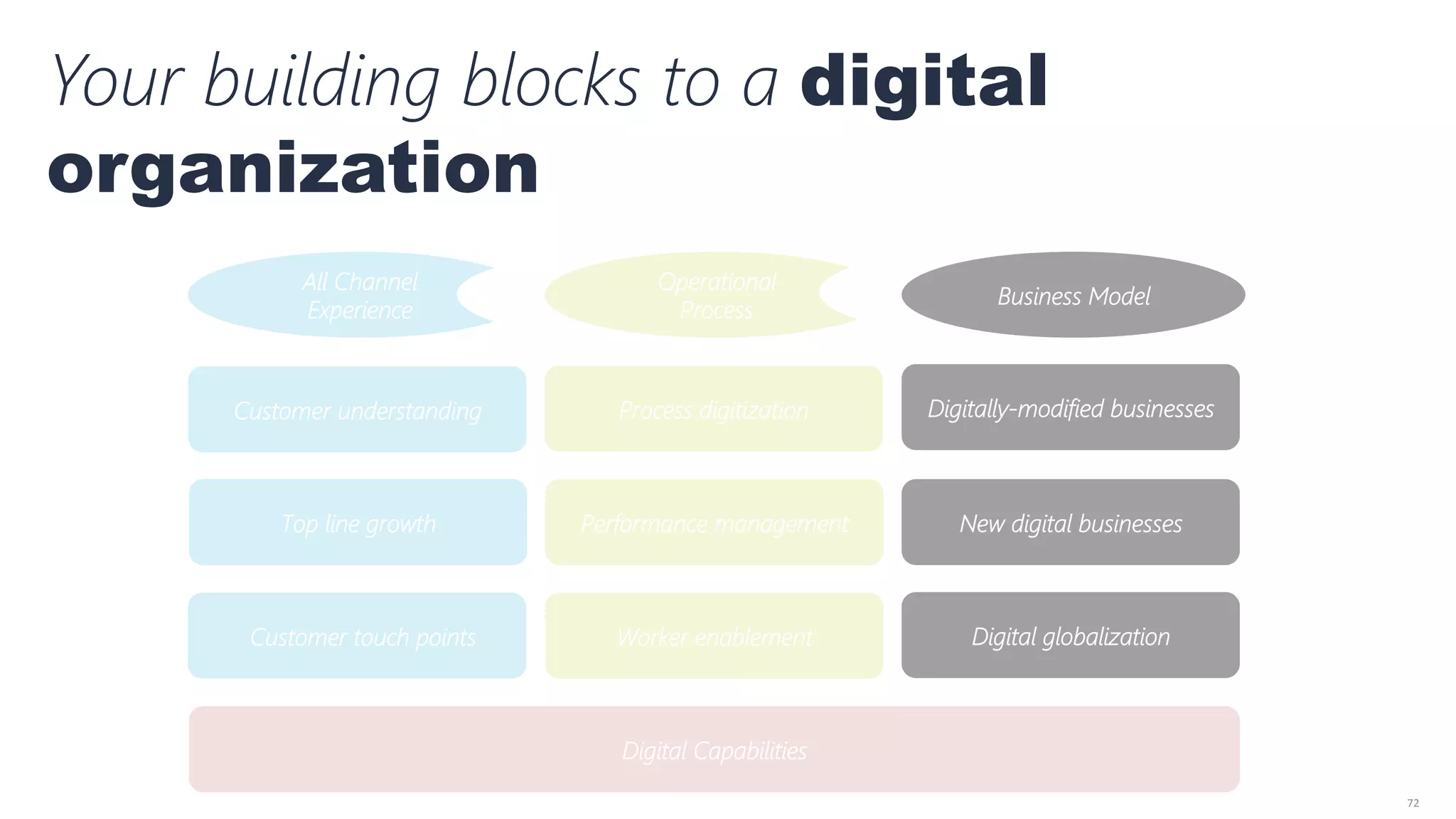

The document discusses the need for the insurance and banking industry to adapt to changing customer behaviors and technological advancements to provide an all-channel experience. It highlights the importance of transparency, customer engagement, and the integration of digital strategies to meet evolving customer expectations. Additionally, it addresses challenges posed by regulations and the necessity for companies to become more adaptable and data-driven in their operations.