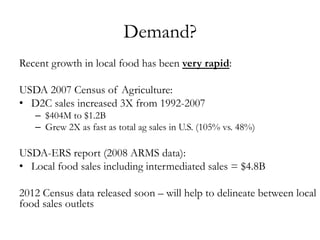

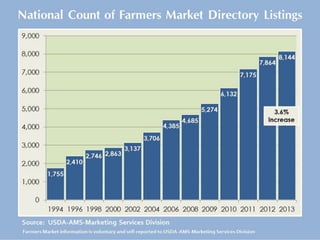

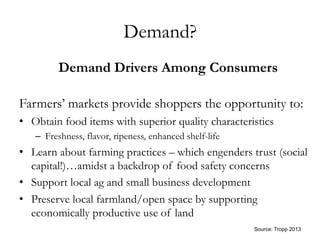

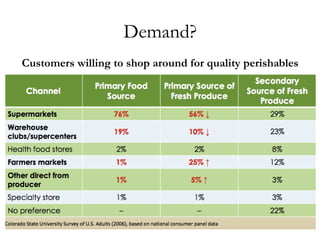

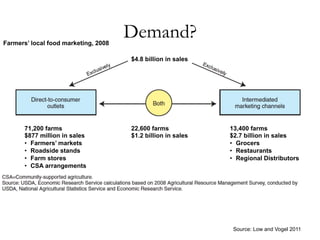

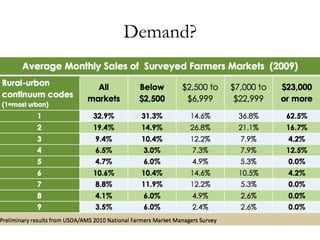

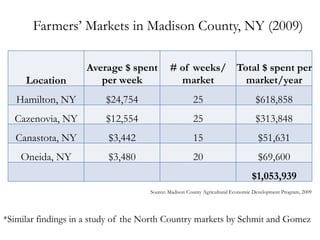

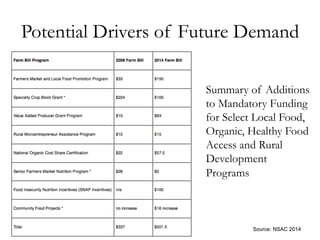

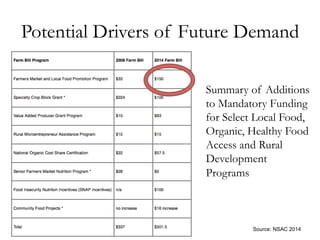

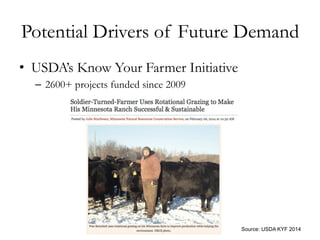

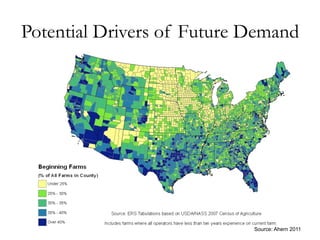

This document summarizes a presentation about the future role of farmers' markets in expanding the local food movement. It provides an overview of national farmers' market statistics and changing consumer preferences. While farmers' markets have grown rapidly, some data shows a slowing in new market growth. Barriers include markets being labor-intensive and not very profitable. Potential drivers of future demand include expanded nutrition assistance programs at markets, USDA local food initiatives, and growing numbers of winter markets and markets at healthcare facilities. Farmers' markets will continue playing an important role in providing entry points for small farms, though their role may evolve as producers access larger wholesale channels.