Downloaded 17 times

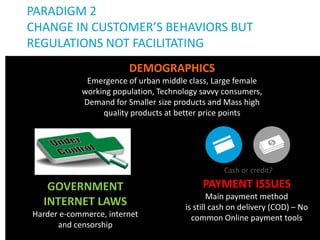

The document outlines five key paradigms of digital marketing in Vietnam, highlighting the pervasive nature of digital technologies and the gradual adaptation of e-commerce. It discusses changes in consumer behavior, challenges with payment systems, increasing consumer expectations, and the struggle for companies to secure digital talent. Additionally, it suggests strategies for improving digital marketing efforts, such as enhancing cross-channel experiences and localizing approaches to different cultural contexts.