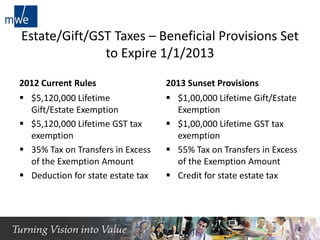

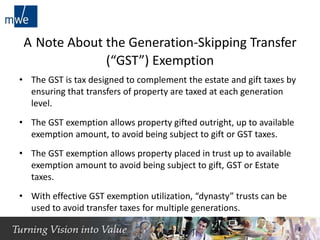

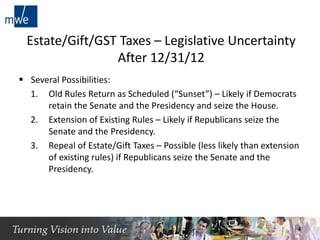

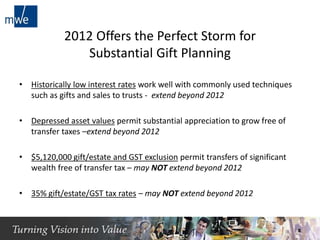

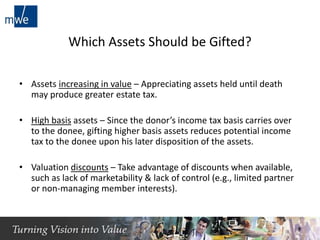

This document discusses opportunities for gift and estate planning in 2012 given that beneficial estate and gift tax provisions are set to expire on January 1, 2013. It notes that the lifetime gift/estate and GST tax exemptions will decrease substantially, as will the tax rate, unless action is taken. It recommends making gifts now to take advantage of the higher $5.12M exemptions and lower 35% tax rate before they expire. Specific techniques discussed include outright gifts, trusts, GRATs, QPRTs, life insurance trusts, and sales to intentionally defective grantor trusts.

![Slirp 4 9 09 Final[1]](https://cdn.slidesharecdn.com/ss_thumbnails/slirp4909final1-12667828759198-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![July.August 2011 Estate Planner[1]](https://cdn.slidesharecdn.com/ss_thumbnails/bhgjulyaugust2011estateplanner1-13106468939217-phpapp01-110714075251-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)