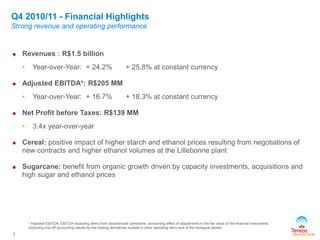

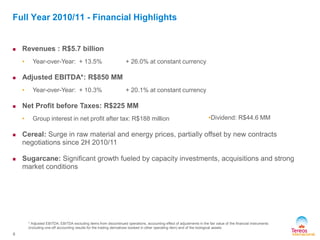

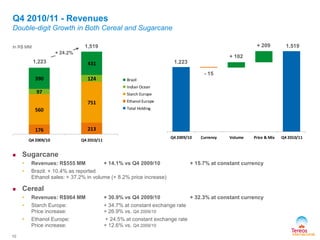

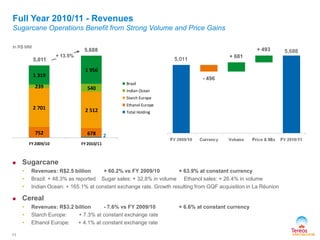

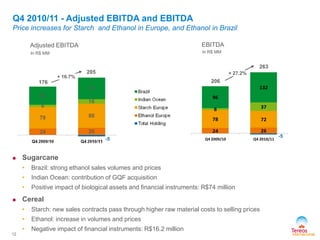

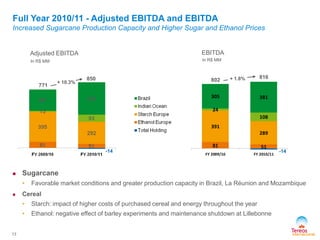

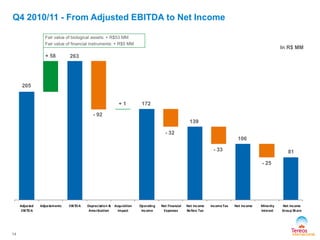

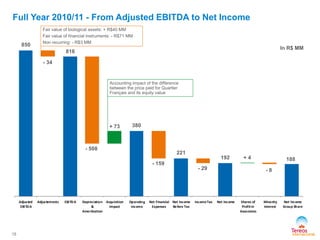

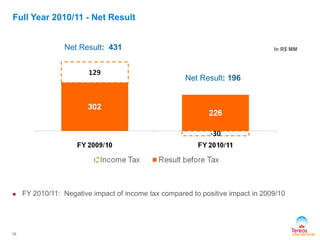

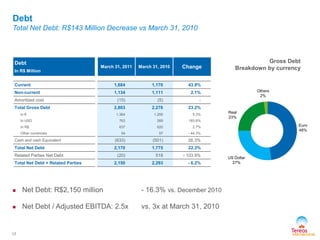

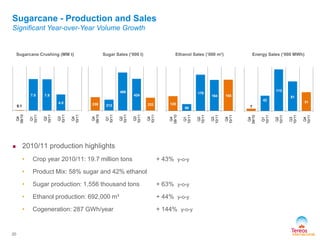

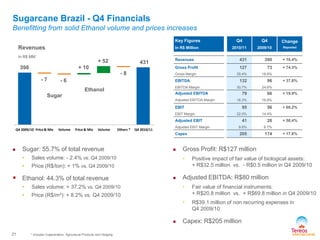

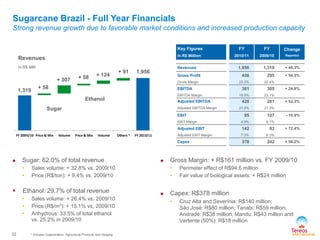

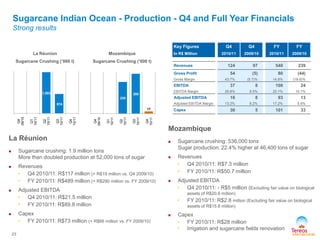

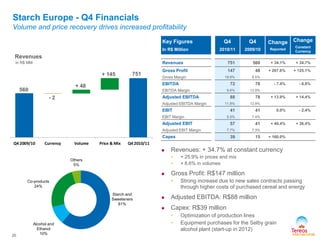

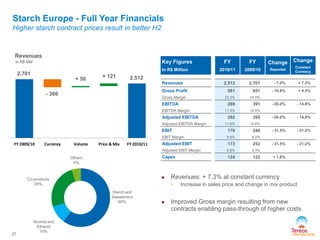

The document reports on the financial results of Tereos Internacional for the fourth quarter and full year of 2010/11. Key highlights include 24.2% revenue growth and 16.7% adjusted EBITDA growth for Q4, driven by double-digit increases in both cereal and sugarcane operations. For the full year, revenues grew 13.5% and adjusted EBITDA grew 10.3%, with sugarcane revenues increasing 60.2% due to higher volumes and prices. Net debt decreased 16.3% from the previous year. The company also announced several expansion projects and investments totaling over $1 billion for its sugarcane operations in Brazil.