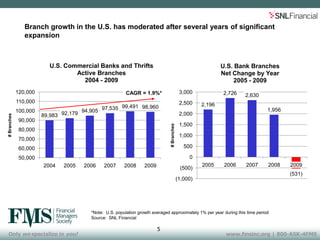

The document summarizes an upcoming presentation on branch network optimization for community banks. It provides background on SNL Financial, the company giving the presentation, and outlines the agenda which will discuss the current industry situation, analytical frameworks for optimization, a case study, and critical success factors. Branch growth has moderated in recent years and new technologies are impacting branch transactions, leading many banks to evaluate their branch networks.