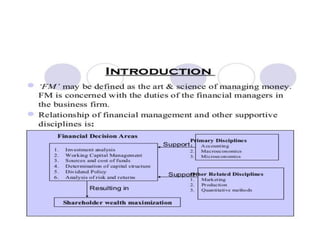

Meaning

• Financial ManagementFinancial management

is mainly concerned with the proper

management of funds. The finance manager

must see that funds are procured in such a

manner that risk, cost and control

considerations are properly balanced and

there is optimum utilization of fund

3.

Meaning of FinancialManagement

• Financial Management means planning,

organizing, directing and controlling the

financial activities such as procurement and

utilization of funds of the enterprise. It means

applying general management principles to

financial resources of the enterprise.

4.

Defination

• According toSoloman , “Financial

management is concerned with the efficient

use of economic resources”.

• According to Phillippatus , “Financial

management is concerned with management

decision that result in acquisition and

financing of long-term and short-term credits

for the firm

6.

Scope of financialmanagement

• The scope and functions of financial

management is classified in two categories.

• - Traditional approach

• - Modern approach

7.

Traditional approach

• Thetraditional approach Evolved during the

1920’s and 1930’s known as ‘Corporation

Finance’.

• According to this approach, the scope of the

finance function is restricted to “procurement of

funds by corporate enterprise to meet their

financial needs.

• The term ‘procurement’ refers to raising of funds

externally as well as the inter related aspects of

raising funds.

8.

Traditional approach

• Intraditional approach the resources could be

raised from the combination of the available

sources.

• The inter related aspects are the institutional

arrangement for finance, financial instruments

through which funds are raised and legal and

accounting aspects between the firm and its

sources of funds.

9.

Limitations of traditionalapproach

• This approach is confirmed to ‘procurement of funds’ only.

• It fails to consider an important aspects i.e. allocation of

funds.

• It deals with only outside I.e. investors, investment bankers.

• The internal decision making is completely ignored in this

approach.

• The traditional approach fails to consider the problems

involved in working capital management.

• The traditional approach neglected the issues relating to the

allocation and management of funds and failed to make

financial decisions.

10.

Modern approach

• Themodern approach is an analytical way of

looking into financial problems of the firm.

According to this approach, the finance

function covers both acquisition of funds as

well as the allocation of funds to various uses.

Financial management is concerned with the

issues involved in raising of funds and efficient

and wise allocation of funds

11.

Main Contents ofModern approach

• How large should an enterprise be and how

far it should grow?

• In what form should it hold its assets?

• How should the funds required be raised?

• Financial management is concerned with

finding answer to the above problems.

12.

Scope/Elements

• Investment decisionsincludes investment in fixed assets (called as

capital budgeting). Investment in current assets are also a part of

investment decisions called as working capital decisions.

• Financial decisions - They relate to the raising of finance from

various resources which will depend upon decision on type of

source, period of financing, cost of financing and the returns

thereby.

• Dividend decision - The finance manager has to take decision with

regards to the net profit distribution. Net profits are generally

divided into two:

– Dividend for shareholders- Dividend and the rate of it has to be decided.

– Retained profits- Amount of retained profits has to be finalized which

will depend upon expansion and diversification plans of the enterprise

14.

Investment Decision

• Oneof the most important finance functions is to intelligently

allocate capital to long term assets. This activity is also known as

capital budgeting. It is important to allocate capital in those long

term assets so as to get maximum yield in future. Following are

the two aspects of investment decision

• Evaluation of new investment in terms of profitability

• Comparison of cut off rate against new investment and prevailing

investment.

• Since the future is uncertain therefore there are difficulties in

calculation of expected return. Along with uncertainty comes the

risk factor which has to be taken into consideration. This risk factor

plays a very significant role in calculating the expected return of

the prospective investment. Therefore while considering

investment proposal it is important to take into consideration both

expected return and the risk involved.

15.

Financial Decision

• Financialdecision is yet another important function which a financial

manger must perform. It is important to make wise decisions about when,

where and how should a business acquire funds. Funds can be acquired

through many ways and channels. Broadly speaking a correct ratio of an

equity and debt has to be maintained. This mix of equity capital and debt

is known as a firm’s capital structure.

• A firm tends to benefit most when the market value of a company’s share

maximizes this not only is a sign of growth for the firm but also maximizes

shareholders wealth. On the other hand the use of debt affects the risk

and return of a shareholder. It is more risky though it may increase the

return on equity funds.

• A sound financial structure is said to be one which aims at maximizing

shareholders return with minimum risk. In such a scenario the market

value of the firm will maximize and hence an optimum capital structure

would be achieved. Other than equity and debt there are several other

tools which are used in deciding a firm capital structure.

16.

Dividend Decision

• Earningprofit or a positive return is a common aim of

all the businesses. But the key function a financial

manger performs in case of profitability is to decide

whether to distribute all the profits to the shareholder

or retain all the profits or distribute part of the profits

to the shareholder and retain the other half in the

business.

• It’s the financial manager’s responsibility to decide a

optimum dividend policy which maximizes the market

value of the firm. Hence an optimum dividend payout

ratio is calculated. It is a common practice to pay

regular dividends in case of profitability Another way is

to issue bonus shares to existing shareholders.

17.

Objectives of Financialmanagement

• The objective provide a framework for

optimum financial decision making. They are

concerned with designing a method of

operating the internal investment and

financing of a firm.there are two widely

discussed approaches under this, these are:

Profit Maximisation Wealth Maximisation

18.

Profit Maximisation

• ProfitMaximisation Profit /EPS maximisation

should be undertaken and those that decrease

profits or EPS are to be avoided. Profit is the test

of economic efficiency. It leads to efficient

allocation of resources, as resources tend to be

directed to uses which in terms of profitability are

the most desirable. Financial management is

mainly concerned with the efficient economic

resources namely capital. The main technical flaws

of this criteria are : Ambiguity Timing of

benefits Quality of benefits

19.

Wealth Maximisation

• Wealthmaximisation is also known as Value or Net

present worth maximisation. Its operational features

satisfy all the three requirements of the operational of

the financial course of action namely, exactness,

quality of benefits, and the time value of money. Two

important issues related to the value/share price

maximisation are: Focus on stakeholders ,stakeholders

include groups such as employees, customers,

suppliers, creditors, owners and others who have a

direct link to the firm.

• EVA (Economic Value Added) –EVA is equal to the

after-tax operating profits of a firm less the cost of the

firm to finance investments.

20.

Wealth maximization vsprofit

maximization

• The financial management has come a long

way by shifting its focus from traditional

approach to modern approach.

The modern approach focuses on wealth

maximization rather than profit maximization.

This gives a longer term horizon for

assessment, making way for sustainable

performance by businesses.

21.

Sources Of Finance

•Sources of Finance :Capital required for a business

can be classified under two main categories, viz

• Fixed Capital, and - Working Capital. - every

business needs funds for two purposes. - for its

establishment and to carry out its day-to-day

operations.

• Long term funds are required to create production

facilities through purchase of fixed assets such as

:plant, - machinery, - land, - building, - furniture,

etc.

22.

Cont---

• Investment inthese asset represent that part

of firm’s capital which is blocked on

permanent or fixed basis and is called fixed

capital.

• Funds are also needed for short-term

purposes for the purchase of raw materials,

payment of wages and other day to day

expenses, etc. These funds are known as

working capital

23.

Cont---

• In factfinance is so indispensable today that is

rightly said that it is the life blood of

enterprise.

• With out adequate finance, no enterprise can

possibly accomplish its objectives.

• In every concern there are two methods of

raising finance, viz.,

• Raising of owned capital,

• Rising of borrowed capital

25.

Issue of shares

•The company’s owned capital is split into large

number of equal parts,such a part being called

a “share”.

• The person holding the share as shareholder

and becomes part-owner of the company.

• For this reason, the capital so raised is known

as “owned capital” and the shares are called

“ownership securities”.

26.

Issue of shares

•The share capital of the company is ideal for

meeting the long term requirements.

• It need not be paid back to the shareholders

within the life time of the company.

• The only exception is the sum raised by the

issue of redeemable preference shares.

27.

Types of shares

•A public company can issue two types of

share.

• Equity share

• Preference share

28.

Equity share

• Equityshare has number of special features

• The dividend on these shares are paid after

the dividend on preference share has been

paid.

• The rate of dividend depends upon the

amount of profits available and the intention

of directors

29.

Equity share

• TheEquity shareholders have the chance of

earning good dividends in times of prosperity

and run the risk of earning nothing in times of

adversity .

• The equity shareholders have a residual claim

on the company’s asset in case of liquidation.

• The company is controlled by the equity

shareholders and they are entitled to vote in

the meetings of the company.

30.

Preference shares

• Preferenceshares are those which carry preferential

right over other class of shares with regard to payment

of dividend and repayment of capital.

• The rate of dividend on preference share is a fixed one

• Preference Share are not traded on secondary market

but they are one of the best primary market

instrument for investors. 1. There are not easily

available: Usually, preference shares are most

commonly issued by companies to institutions.

31.

• Section 55of Companies Act, 2013 read with

rule 9 of the Companies (Share Capital and

Debentures) Rules, 2014 deals with issue &

redemption of preference share.

32.

Procedure of theissue:-

• Check whether issuing preference shares is authorized under the

Articles of the Company or not, if it is not so authorized then first

needs to amend the Articles of the Company.

• Conduct Board Meeting and call the General Meeting for this

purpose.

• An Explanatory Statement shall annexed with Notice calling the

General Meeting, and it shall contain the relevant facts regarding

the issue such as:-

– Size of the Issue, No. of Preference Shares, Nominal Value of the Shares

– Nature of the shares i.e. Cumulative/Non-cumulative,

Participating/Non-participating, Convertible/Non-convertible etc.

– Objective & Manner of the issue.

– Price at which shares are proposed to be issued & basis on which price

33.

• Terms ofissue, rate of dividend, terms &

tenure of redemption.

• Current shareholding pattern of the Company

• Expected dilution of Equity Shares upon

conversion (only if the nature of the issue is

convertible preference shares).

34.

Restrictions on issueof Preference

Shares under the Act:-

• There is a clear restriction on the Company to issue

irredeemable preference shares. A Company shall

redeem its preference shares within the time period of

20 years from the date of issue.

• However if a Company could not redeem its

preference share with-in this time period due to

unavoidable reasons then it may pass Special

Resolution with 3/4th Majority and file petition to the

NCLT and on the order of NCLT may issue preference

shares of same kind with similar rate of dividend for

some time period instead of redemption of existing

one.

![5) capital_budgeting_(1)_-(2)[1].ppt.pdf](https://cdn.slidesharecdn.com/ss_thumbnails/5capitalbudgeting121-250323135834-146732f6-thumbnail.jpg?width=640&height=640&fit=bounds)