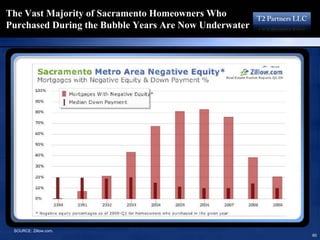

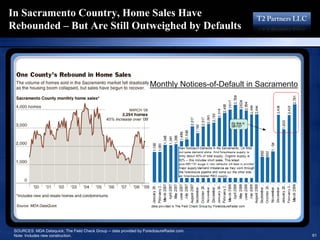

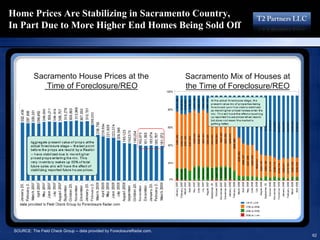

Download as PDF, PPTX

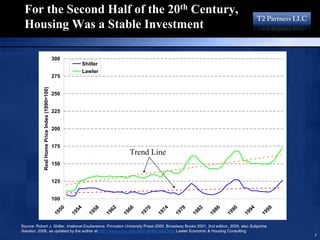

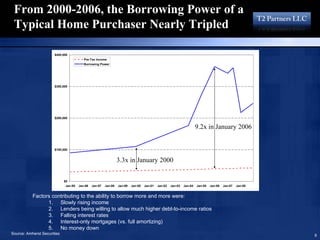

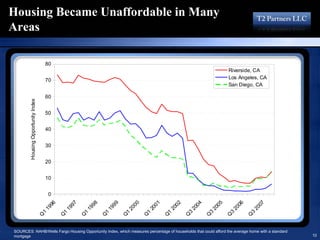

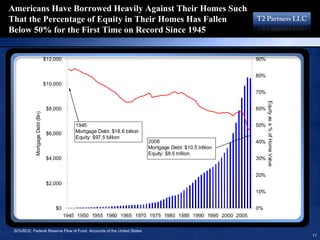

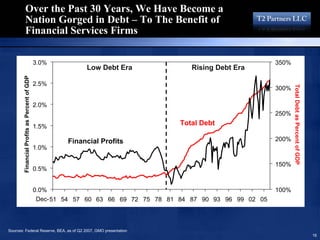

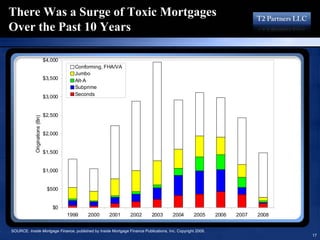

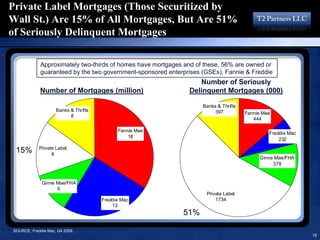

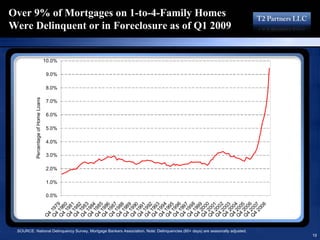

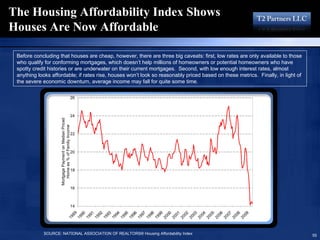

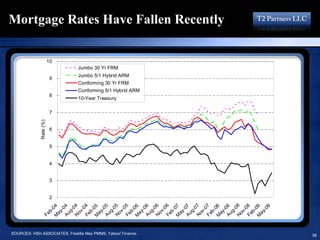

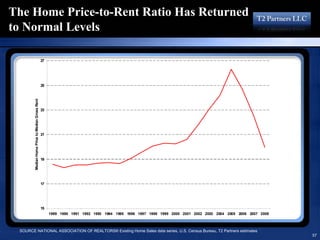

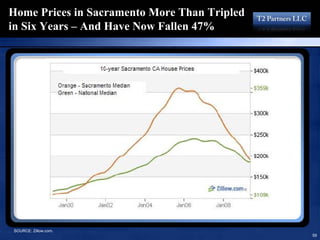

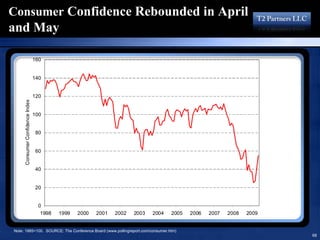

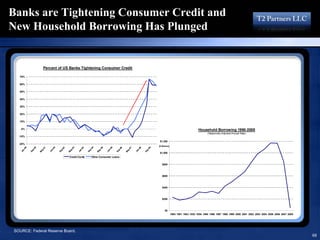

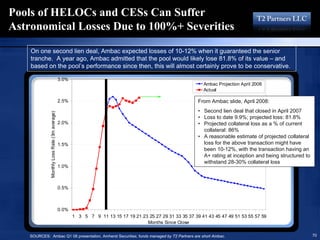

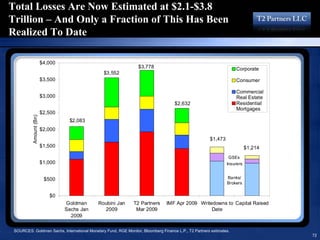

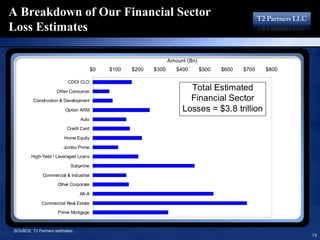

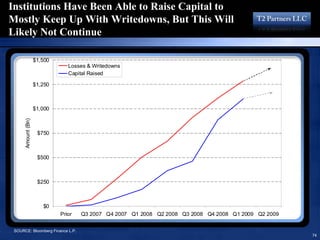

This document provides an overview of the ongoing housing and credit crisis and argues that more problems are still to come. It references an investing book about the mortgage meltdown that is currently the #1 bestseller. It also advertises an upcoming value investing conference and subscription newsletters. Two charts show that after decades of stability, housing prices exploded unstably upwards in the 2000s, indicating a bubble.