![D

E

F

Other

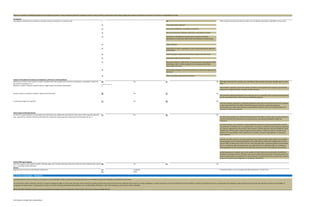

How many directors will this series have the right to designate?

How many directors will this series have the right to designate?

How many directors will this series have the right to designate?

How many directors will the investors have the right to designate? Enter “0” if none.

How many directors will the founders have the right to designate? Enter “0” if none.

How many directors will the founders and the investors have the right to jointly designate? Enter “0” if none.

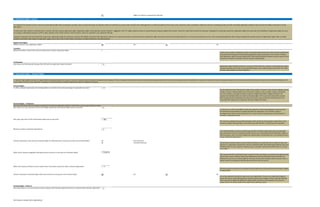

24. Voting Agreement – Common Designees

Yes No

The parties will often agree that one of the designees will be an officer of the company, such as the

Chief Executive Officer or President.

What position?

25. Voting Agreement – Mutual Designees

a majority

at least 66 2/3%

Other

a majority

at least 66 2/3%

Other

26. Board Observer Rights

Yes No

[1] Investor with Board Observer Rights

Name:

[2] Investor with Board Observer Rights

Name:

[3] Investor with Board Observer Rights

Name:

27. “Drag-Along” Rights

Yes No

Persons subject to the "drag-along" requirement: List the relevant individuals using the following format: “[Name], [Name] and [Name]”.

All preferred

Only this series of preferred

Other

a majority

at least 66 2/3%

Other

28. Right of First Refusal on Sales by Other Shareholders

Yes No

The company first, then the investorsThe right of first refusal will be granted to:

Investors will often require that any founder that intends to sell his or her shares offer those shares first to the company and the investors. The primary purpose of the right of first refusal is to provide the company and the investors with the ability to keep the company’s capital stock within the existing ownership group. If the founders or other major stockholders elect to exit the company, the investors will

want the ability to purchase their shares so that the investors may either obtain greater control over the company or prevent the transfer of control to non-strategic or hostile parties. Rights of first refusal are typically granted to the investors and applied against the founders (although, occasionally, these rights may also be granted to founders or applied against other major stockholders).

Right of First Refusal

Will sales by founders or other stockholders be subject to a right of first refusal?

The "drag-along" will be triggered if a sale is approved by:

What is the minimum percentage vote of the investors required (in addition to the approval of the board) to trigger the "drag-

along" rights?

If you select “Other” and enter another amount, include the words “at least” (e.g., “at least 75%”).

A “drag-along” provision obligates stockholders that are subject to the “drag along” to vote to approve a transaction that is otherwise approved by a specified percentage of the stockholders. Common holders may sometimes have different interests than preferred holders, particularly where liquidation preferences will have the effect of minimizing the return to the common holders. “Drag-along” rights provide

the investors with some assurance that the founders and other major common holders (who are typically the focus of “drag along” provisions), and, in some cases, other shareholders, will not attempt to block a sale of the company through the exercise of class voting rights or otherwise.

Shareholders should exercise caution in agreeing to be subject to “drag-along” provisions. Shareholders should understand the implications of being subject to the “drag along” and should carefully assess any associated obligations. In addition, those subject to the “drag along” should ensure that there are appropriate limitations and exceptions.

“Drag-Along” Rights

Will the founders be subject to "drag-along" rights?

(#1 of 3)

(#2 of 3)

(#3 of 3)

Minority investors (that do not otherwise have the right to appoint a director) may ask for the right to have a non-voting observer attend board meetings. In addition, an investor forced to relinquish a board seat as board seats get allocated to new investors will sometimes be given board observer rights. There are important qualifications and limitations that should apply to board observer rights, and it is

important that the rights and limitations are carefully documented.

Board Observer Rights

Will any investors require board observer rights?

Mutual Designee

Investor approval required for a mutual designee: If entering another amount, include the words “at least” (e.g., “at least

75%”).

Founder approval required for a mutual designee: If entering another amount, include the words “at least” (e.g., “at least

75%”).

Mutual Designee(s)

Officer as Common Designee

Is one of the common designees required to be an officer?

Series C Designee(s)

Preferred Designee(s)

Common Designee(s)

Series A Designee(s)

Series B Designee(s)

X

Y

Term Sheet in Simple Terms (Deb Sahoo)](https://image.slidesharecdn.com/00-130817180352-phpapp01/85/00-term-sheet-in-simple-terms-deb-sahoo-13-320.jpg)

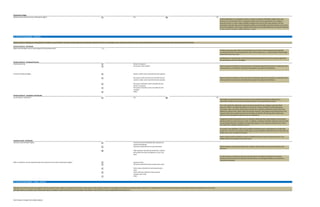

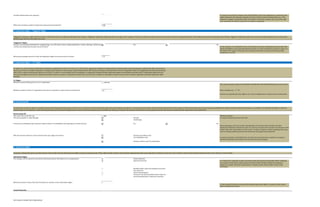

![The company only

The investors only

Yes No

The most common approach is to provide the company and the eligible investors with the right to

purchase all or any portion of the offered shares. This approach provides the most flexibility to the

company and the eligible investors.

Founders may prefer that the company and/or the eligible investors purchase all or none of the

offered shares (on a cumulative basis) since a partial purchase may undermine a founder’s ability to

sell all of the shares (i.e., prospective purchasers may be unwilling to purchase a smaller stake).

All preferred

Only this series of preferred

All outstanding securities (on an as-exercised

and as-converted basis)

The company's fully-diluted capitalization

(including full option pool)

Shares held by all investors with the right of

first refusal

Yes No

An over-allotment right (which is sometimes called a “gobble-up”) would enable investors that fully

exercise their rights of first refusal to have a second chance to purchase any of the offered shares not

otherwise purchased by the company or the investors. This investor-favorable provision is not

uncommon.

From the investor’s perspective, an over-allotment option provides additional protection against

outside parties becoming stockholders in the company. Founders may object since an over-allotment

option can serve to more effectively block any transfer to a third party.

There is a stronger basis for the over-allotment right if the investors are required to purchase all or

nothing in connection with the exercise of their rights of first refusal.

A qualified public offering (i.e., a public offering

that would trigger the automatic conversion of

the preferred)

Any IPO A “qualified public offering” is one that meets the price/proceeds thresholds required to cause the

automatic conversion of the preferred stock into common. Use of the “qualified public offering”

definition protects investors from the loss of their rights prior to the time that they can secure a

certain minimum return on their investment. While it is not contemplated that investors would

continue to have a right of first refusal on sales by founders after the company is public (whether or

not the company’s IPO is a “qualified public offering”), the “qualified public offering” requirement

provides the investors with an additional means to influence the decision as to whether to go public.

29. “Co-Sale” Rights

Yes No

All preferred

Only this series of preferred

Yes No

It is uncommon to give co-sale rights to other founders.

Yes No

An over-allotment right would enable investors that fully exercise their co-sale rights to sell additional

shares to the extent other investors do not fully exercise their co-sale rights. This is an investor-

favorable right.

A qualified public offering (i.e., a public offering

that would trigger the automatic conversion of

the preferred)

Any IPO A “qualified public offering” is one that meets the price/proceeds thresholds required to cause the

automatic conversion of the preferred stock into common. Use of the “qualified public offering”

definition protects investors from the loss of their rights prior to the time that they can secure a

certain minimum return on their investment. While it is not contemplated that investors would

continue to have co-sale rights after the company is public (whether or not the company’s IPO is a

“qualified public offering”), the “qualified public offering” requirement provides the investors with an

additional means to influence the decision as to whether to go public.

30. First Refusal/Co-Sale Restrictions - Founders

[1] Founder

Name of founder to be subject to first refusal/co-sale obligations: Use arrows to add names.

[2] Founder

Name of founder to be subject to first refusal/co-sale obligations: Use arrows to add names.

Termination

The co-sale rights will terminate upon:

(#1 of 2)

(#2 of 2)

Will the founders also have co-sale rights?

Over-Allotment Rights

Will the investors have an over-allotment option with respect to the co-sale rights?

Will sales by founders or other stockholders be subject to co-sale rights?

Who will have co-sale rights on sales by founders?

Termination

The right of first refusal will terminate upon:

“Co-sale” rights enable investors to participate in any sales of the company’s capital stock by founders or other large stockholders. Co-sale rights are principally designed to protect investors’ interests in a situation where founders or others attempt to sell a significant block of common stock. Investors may want the option to participate in the sale since the sale of a controlling interest may involve a control

premium and may have the effect of foreclosing other avenues to liquidity. In addition, investors may generally want an opportunity to liquidate their investment if the founders are seeking to exit the enterprise.

Co-Sale Rights

Will participating investors have an over-allotment right with respect to unsubscribed shares?

Investors

Who will have the right of first refusal on proposed transfers by founders?

The right will be allocated pro rata among investors based on:

Company

Will the company be required to purchase all the shares proposed to be transferred if it exercises its right of first refusal?

Deb Sahoo

Term Sheet in Simple Terms (Deb Sahoo)](https://image.slidesharecdn.com/00-130817180352-phpapp01/85/00-term-sheet-in-simple-terms-deb-sahoo-14-320.jpg)

This document summarizes key terms related to a preferred stock financing. It discusses warrant terms, offering size and valuation, liquidation preferences, participation rights, and conversion rights. The main points covered are: - Warrants may be issued with bridge loans or preferred stock financings and allow the holder to purchase shares at a set exercise price. - The term sheet will specify the pre-money valuation, number of shares sold, and whether warrants are included. - Liquidation preferences typically return the purchase price to investors first and are often 1-2x the purchase price. Participating preferred may share residual proceeds. - Conversion rights allow preferred stock to convert to common stock, usually automatically upon an

![Sample Silicon Valley Series A Term Sheet from DLA Piper [SVNewTech]](https://cdn.slidesharecdn.com/ss_thumbnails/svnewtech-series-a-termsheet-100108184114-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)