Uploaded byDeb Sahoo, MBA(Finance), MS(EE), BTech(EE),

15. dcf vs bgf

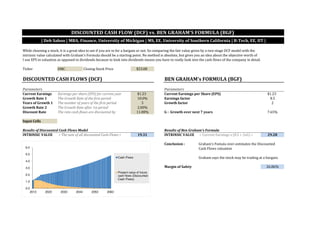

The document compares two valuation methods - discounted cash flows (DCF) and Ben Graham's formula - to determine the intrinsic value of a stock. Using parameters like current earnings per share, growth rates, and discount rate, the DCF model estimates the stock's intrinsic value at $19.31, while Graham's formula estimates it at $29.28. The conclusion is that Graham's formula may overestimate the value compared to DCF, but both methods can provide an initial view of a stock's worthiness as a bargain.

15. dcf vs bgf

- 1. I use EPSin valuation as opposed to dividends because to look into dividends means you have to really look into the cash flows of the company in detail. Ticker EMC Closing Stock Price $23.08 DISCOUNTED CASH FLOWS (DCF) BEN GRAHAM's FORMULA (BGF) Parameters Parameters Current Earnings $1.23 Current Earnings per Share (EPS) $1.23 Growth Rate 1 10.0% Earnings factor 8.5 Years of Growth 1 5 Growth factor 2 Growth Rate 2 2.00% Discount Rate 11.00% G : Growth over next 7 years 7.65% Input Cells Results of Discounted Cash Flows Model Results of Ben Graham's Formula INTRINSIC VALUE 19.31 INTRINSIC VALUE = Current Earnings x (8.5 + 2xG) = 29.28 Conclusion : Graham says the stock may be trading at a bargain. Margin of Safety 26.86% Earnings per share (EPS) for current year Graham's Fomula over-estimates the Discounted Cash Flows valuation DISCOUNTED CASH FLOW (DCF) vs. BEN GRAHAM'S FORMULA (BGF) | Deb Sahoo | MBA, Finance, University of Michigan | MS, EE, University of Southern California | B-Tech, EE, IIT | While choosing a stock, it is a great idea to see if you are in for a bargain or not. So comparing the fair value given by a two-stage DCF model with the intrinsic value calculated with Graham's Formula should be a starting point. No method is absolute, but gives you an idea about the objective worth of The Growth Rate after 1st period The Growth Rate of the first period The number of years of the first period The rate cash-flows are discounted by = The sum of all discounted Cash-Flows = 0.0 1.0 2.0 3.0 4.0 5.0 6.0 2013 2023 2033 2043 2053 2063 Cash-Flows Present value of future cash flows (Discounted Cash-Flows)