Downloaded 60 times

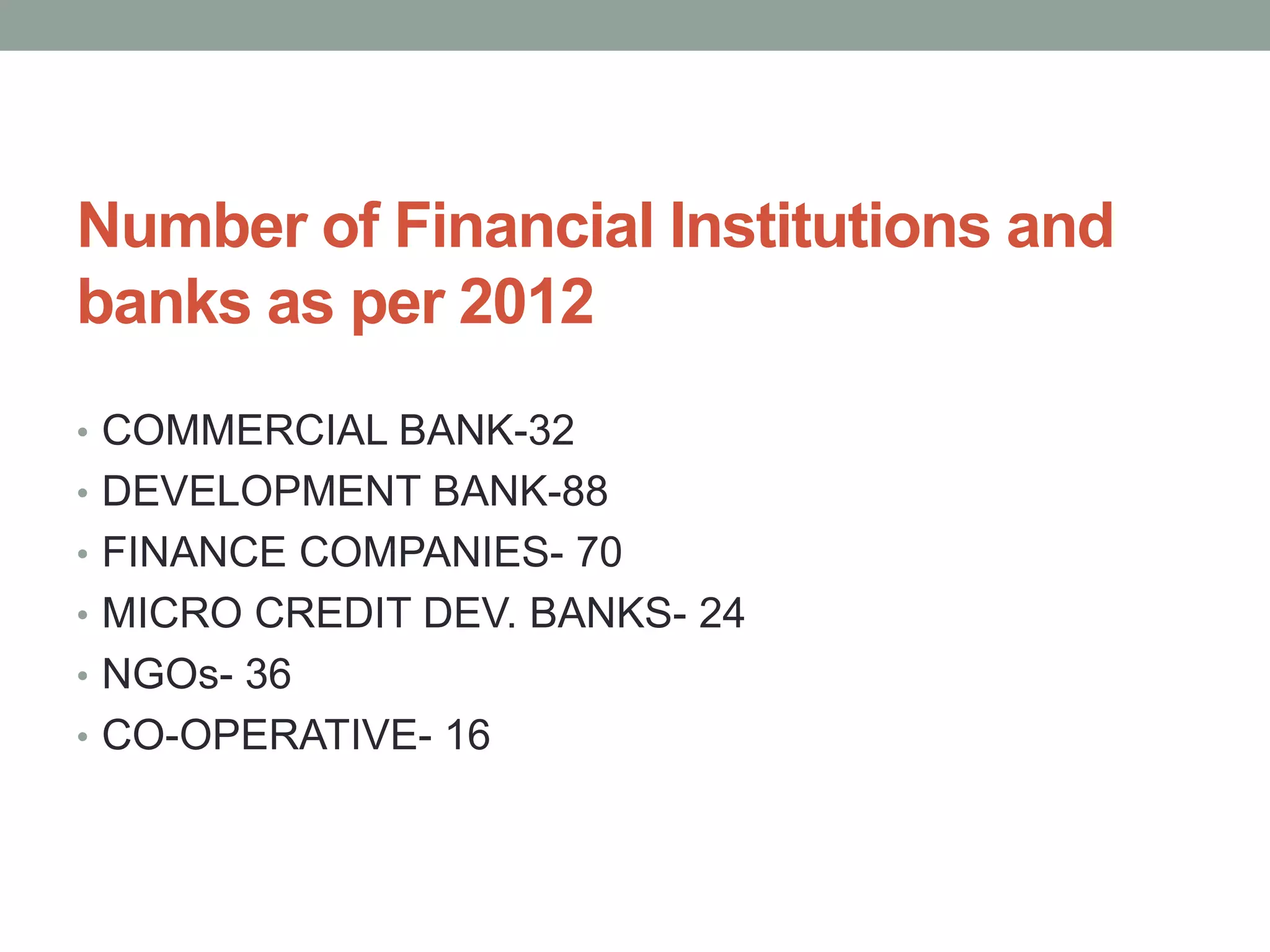

Financial institutions play a key role in the economy by facilitating transactions and the flow of money. In Nepal, there are various types of financial institutions that serve different functions: - Commercial banks accept deposits and provide business loans and basic investment services. Nepal's first commercial bank was Nepal Bank Ltd. - Development banks like the Nepal Development Bank Limited provide medium and long-term financing to support sectors like industry and agriculture. - Other financial institutions in Nepal include finance companies, microcredit banks, cooperatives, and non-governmental organizations. As of 2012 there were over 300 registered financial institutions operating in Nepal.