More Related Content

More from nadinesullivan (20)

Les 26 4

- 2. CLOSING ENTRY FOR ACCOUNTS WITH CREDIT

BALANCES

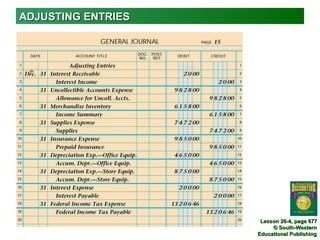

1

2

1. Enter the balance of accounts in the Income

Statement credit column as a debit.

2. Enter the total of debit entries as a credit to to

Income Summary.

Lesson 26-4, page 678

© South-Western

Educational Publishing

- 3. CLOSING ENTRY FOR ACCOUNTS WITH DEBIT

BALANCES

1. Enter Income

Summary.

2. Enter the

1 2 balance of

every account

in the Income

Statement

debit column

as a credit.

3 3. Enter the total

as a debit to

Income

Summary.

Lesson 26-4, page 679

© South-Western

Educational Publishing

- 4. CLOSING ENTRY TO RECORD NET INCOME

1

2

1. Debit Income Summary

2. Credit Retained Earnings

Lesson 26-4, page 680

© South-Western

Educational Publishing

- 5. CLOSING ENTRY FOR DIVIDENDS

1

2

1. Debit Retained Earnings

2. Credit Dividends

Lesson 26-4, page 680

© South-Western

Educational Publishing

- 6. REVERSING ENTRIES

1. Reverse the entry

that created a

balance in

Interest

Receivable.

2. Reverse the entry

that created a

balance in

Interest Payable.

1 3. Reverse the entry

that created a

2 balance in

Federal Income

Tax Payable.

3

Lesson 26-4, page 681

© South-Western

Educational Publishing

- 7. ACCOUNTING CYCLE FOR A MERCHANDISING

BUSINESS ORGANIZED AS A CORPORATION

1. Source documents checked for accuracy,

and transactions are analyzed.

2. Transactions are recorded in a

1 2 journal.

3. Journal entries are posted to

9 ledgers.

4. Schedules of accounts

8 3 payable and accounts

receivable are prepared from

subsidiary ledgers.

4

5. Work sheet is prepared.

5

6. Financial statements are

7 prepared.

7. Adjusting and closing

entries are journalized.

8. A post-closing trial

6 balance is prepared.

9. Reversing entries are

journalized and posted to Lesson 26-4, page 682

the general ledger. © South-Western

Educational Publishing