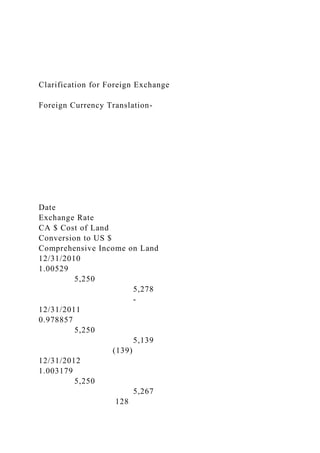

Clarification for Foreign Exchange

Foreign Currency Translation-

Date

Exchange Rate

CA $ Cost of Land

Conversion to US $

Comprehensive Income on Land

12/31/2010

1.00529

5,250

5,278

-

12/31/2011

0.978857

5,250

5,139

(139)

12/31/2012

1.003179

5,250

5,267

128

12/31/2013

0.940531

5,250

4,938

(329)

ABC Company acquired a Canadian Subsidiary whose only asset was land.

ABC Company purchased the subsidiary on 12/31/10 for CA $5,250 and retaines 100% interest in the subsidiary.

Go to www.x-rates.com and use the historic lookup feature to determine the exact exchange rates on 12/31/10, 12/31/11, 12/31/12 and 12/31/13.

Clarification for Comprehensive Income

For the Year Ended December 31, 2013

Net Earnings

5,385.00

Other Comprehensive (Loss) Income:

Foreign Currency Translation Adjustments

(329.00)

Cash Flow Hedges, net of tax

(12.00)

Other Comprehensive Income

(10.00)

Total Other Comprehensive (Loss) Income

(351.00)

COMPREHENSIVE INCOME

5,034.00

Clarification for statement of OE

ABC Company

Statement of Owners Equity

For the Year Ended December 31, 2013

Capital Stock:

Preferred Stock

-

Common Stock

88.00

88.00

Additional Paid in Capital

8,402.00

Retained Earnings

23,048.00

31,538.00

Accumulated Other

Comprehensive Income

46.00

Treasury Stock

(19,194.00)

Total Shareholder's Equity

12,390.00

Clarification for Statement of Earnings

ABC Company

Statement of Retained Earnings

For the Year Ended December 31, 2013

January 1, as Reported

20,038.00

Correction of depreciation error

(903.00)

Cumulative increase in income

from inventory method change

771.00

January 1, as adjusted

19,906.00

Net Income

5,385.00

25,291.00

Dividends

(2,243.00)

Balance, December 31

23,048.00

Title

ABC/123 Version X

1

ABC Company History

ACC/545 Version 6

1

University of Phoenix Material

ABC Company History

The ABC Company is a mid-sized company that manufact.

Clarification for Foreign ExchangeForeign Currency Transla.docx

1. Clarification for Foreign Exchange

Foreign Currency Translation-

Date

Exchange Rate

CA $ Cost of Land

Conversion to US $

Comprehensive Income on Land

12/31/2010

1.00529

5,250

5,278

-

12/31/2011

0.978857

5,250

5,139

(139)

12/31/2012

1.003179

5,250

5,267

128

2. 12/31/2013

0.940531

5,250

4,938

(329)

ABC Company acquired a Canadian Subsidiary whose only

asset was land.

ABC Company purchased the subsidiary on 12/31/10 for CA

$5,250 and retaines 100% interest in the subsidiary.

Go to www.x-rates.com and use the historic lookup feature to

determine the exact exchange rates on 12/31/10, 12/31/11,

12/31/12 and 12/31/13.

Clarification for Comprehensive Income

For the Year Ended December 31, 2013

Net Earnings

5,385.00

Other Comprehensive (Loss) Income:

Foreign Currency Translation Adjustments

(329.00)

Cash Flow Hedges, net of tax

(12.00)

Other Comprehensive Income

3. (10.00)

Total Other Comprehensive (Loss) Income

(351.00)

COMPREHENSIVE INCOME

5,034.00

Clarification for statement of OE

ABC Company

Statement of Owners Equity

For the Year Ended December 31, 2013

Capital Stock:

Preferred Stock

-

Common Stock

88.00

88.00

Additional Paid in Capital

8,402.00

Retained Earnings

5. January 1, as Reported

20,038.00

Correction of depreciation error

(903.00)

Cumulative increase in income

from inventory method change

771.00

January 1, as adjusted

19,906.00

Net Income

5,385.00

25,291.00

Dividends

(2,243.00)

Balance, December 31

23,048.00

Title

ABC/123 Version X

1

ABC Company History

ACC/545 Version 6

1

6. University of Phoenix Material

ABC Company History

The ABC Company is a mid-sized company that manufactures

goods in the United States and has begun to expand the

operation overseas. The company maintains a healthy balance

sheet and has reported positive net income since inception.

Currently, the organization utilizes the average cost inventory

method and is exploring a change in accounting principle to

maximize net income and attract new stockholders. Also, the

company utilizes the straight-line method of depreciating fixed

assets, which are primarily machinery/equipment and several

large production facilities.

The organization is a publically–traded company that sells its

stock on the open market. Demand for the stock has caused an

increase in the price per share, and if the trend continues, the

organization is considering splitting the stock to encourage

investment. The company is having success selling preferred

stock on the open market as well.

ABC Company offers its employees a generous pension plan,

but it is currently investigating pension plan changes that will

benefit both the employees and the stockholders. Also, the

company offers a 401k and an employee stock purchase plan to

encourage employees to be owners of their company.

Finally, the company finances some of the major investments it

has made, including warehouses and land. To accomplish

company goals, it has issued bonds in which the company is

now considering restructuring.

2013

2012

8. Additional paid-in capital

(9,100)

(7,500)

Retained earnings

(25,200)

(64,600)

Sales

(558,300)

(778,700)

Cost of goods sold

250,000

380,000

Selling expenses

141,500

172,000

General and administrative expenses

137,000

151,300

Interest expense

4,300

2,600

Income tax expense

20,400

61,200

Additional information:

1. Los Lobos purchased $5,000 in equipment during 2007.

2. Los Lobos allocated one-third of its depreciation expense to

selling expenses and the remainder to general and

administrative expenses.

3. Bad debt expense for 2007 was $5,000, and write-offs of

uncollectible accounts totaled $4,800.

4. $12,000 of the debt is current portion.

9. Cash Sales

$72,600

Collections on Receivables

477,900

Purchases

(219,500)

Purchase of Equipment

(5,000)

Wages

(150,700)

Payments to Suppliers

(126,300)

Tax Payments

(27,800)

Borrowing

30,000

Repayment of Debt

(5,000)

Interest Payments

(3,800)

Sale of Stock

11,600

Dividends

(51,000)

On January 1, 2006, Jamona Corp. purchased 12% bonds,

having a maturity value of $300,000, for $322,744.44. The

bonds provide the bondholders with a 10% yield. They are dated

January 1, 2006, and mature January 1, 2011, with interest

receivable December 31 of each year. The company uses the

effective-interest method to allocate unamortized discount or

premium. The bonds are classified as available-for-sale. The

fair value of the bonds at December 31 of each year is as

follows:

10. · 2006 – $320,500

· 2007 – $309,000

· 2008 – $308,000

· 2009 – $310,000

· 2010 – $300,000

The following information is available from Jamona’s inventory

records:

Units

Unit Cost

January 1, 2007 (beginning inventory)

600

$ 8.00

Purchases:

January 5, 2007

1,200

9.00

January 25, 2007

1,300

10.00

February 16, 2007

800

11.00

March 26, 2007

600

12.00

A physical inventory on March 31, 2007, shows 1,600 units on

hand. Select any one of the inventory methods (LIFO, FIFO,

11. Average Cost, or others).

On July 6, Jamona Corp. acquired the plant assets of Berry

Company, which had discontinued operations. The appraised

value of the property is:

Land

$ 400,000

Building

1,200,000

Machinery and equipment

800,000

Total

$2,400,000

Jamona Corp. gave 12,500 shares of its $100 per value common

stock in exchange. The stock had a market value of $168 per

share on the date of the purchase of the property.

Jamona Corp. expended the following amounts in cash between

July 6 and December 15, the date when it first occupied the

building.

Repairs to building

$105,000

Construction of bases for machinery to be installed later

135,000

Driveways and parking lots

122,000

Remodeling of office space in building

161,000

Special assessment by city on land

18,000

12. On December 20, the company paid cash for machinery,

$260,000, subject to a 2% cash discount, and freight on

machinery of $10,500.

On January 1, 2007, Jamona Corp. signed a 5-year,

noncancelable lease for a machine. The terms of the lease called

for Jamona to make annual payments of $8,668 at the beginning

of each year, starting January 1, 2007. The machine has an

estimated useful life of 6 years and a $5,000 unguaranteed

residual value. The machine reverts to the lessor at the end of

the lease term. Jamona uses the straight-line method of

depreciation for all of its plant assets. Jamona’s incremental

borrowing rate is 10%, and the lessor’s implicit rate is

unknown.

Restructuring Debt Data

Your company is in financial trouble and is in the process of

reorganizing. Your manager wants to know how you will report

on restructuring the debt. Use the following information to help

with this assignment.

Part A

ASSETS

CURRENT ASSETS

Cash and cash equivalents

$ 108,340

Trade accounts receivable, net of allowances

2,866,260

Other receivables

62,150

Operating supplies, at lower of average

13. cost or market

58,630

Prepaid expenses

446,050

Total Current Assets

3,541,430

PROPERTY, PLANT, AND EQUIPMENT (at cost)

Land

1,950,000

Buildings and improvements

2,327,410

Equipment

5,015,660

Other equipment and leasehold improvements

1,645,580

total

14. 10,938,650

Accumulated depreciation and amortization

(7,644,430)

Net Property, Plant, and Equipment

3,294,220

OTHER ASSETS

Deposits and other assets

1,000,080

TOTAL ASSETS

$ 7,835,730

LIABILITIES AND SHAREHOLDERS’ EQUITY (DEFICIT)

15. CURRENT LIABILITIES

Accounts payable

$ 972,160

Accrued liabilities

2,071,270

Accrued claims costs

793,620

Federal and other income taxes

19,710

Deferred income taxes

500

Current maturities of long-term debt and

capital lease obligations

50,610

Short-term borrowings

249,250

Total Current Liabilities

4,157,120

LONG-TERM LIABILITIES

16. Capital lease obligation

54,580

Note outstanding

3,000,000

Mortgage outstanding

608,030

Other liabilities

95,860

Total long-term liabilities

3,758,470

Total Liabilities

7,915,590

SHAREHOLDERS’ EQUITY (DEFICIT)

Common stock, $.01 par value; authorized

500,000 shares; issued 231,000 shares

2,310

Additional paid-in capital

17. 731,090

Accumulated other comprehensive loss

(113,500)

Retained earnings (deficit)

(639,180)

Treasury stock

(60,580)

Total Shareholders’ Equity (Deficit)

(79,860)

TOTAL LIABILITIES AND SHAREHOLDERS’ EQUITY

$ 7,835,730

Part B

As stipulated, your company is having financial difficulty and

has asked the bank to restructure its $3 million note

outstanding. The present note has 3 years remaining and pays a

current interest rate of 10%. The present market rate for a loan

of this nature is 12%. The note was issued at its face value. The

bank agrees to accept land in exchange for relinquishing its

claim on this note. The land has a book value of $1,950,000 and

a fair value of $2,400,000.

The company provides the following information related to its

postemployment benefits for the year 2007:

· Accumulated postretirement benefit obligation at January 1,

18. 2007: $810,000

· Actual and expected return on plan assets: $34,000

· Unrecognized prior service cost amortization: $21,000

· Discount rate: 10%

· Service cost: $88,000

Lee Corporation Equity Scenario

Lee Corporation is an American company that began operations

on January 1, 2004. It has just completed its fourth full year of

operations on December 31, 2007. Ending Year Balances for

the prior year that ended on December 2006 were as follows:

Retained Earnings: $225,000

Common Stock at par: $500,000

Additional Paid-in Capital: $1,000,000

Treasury Stock: $200,000

Income before taxes for 2007 totaled $240,000.

Effective Tax Rate was 40% for all years of operation including

2007.

The following information relates to 2007:

1. An error was discovered during 2007. Specifically,

depreciation expense was understated in 2005, resulting in the

need for a Prior Period Adjustment of $25,000 before taxes.

2. Lee Corporation changed its method of valuing inventory

during 2007. The cumulative decrease in income from the

change in inventory methods was $35,000 before taxes.

3. Lee Corporation declared cash dividends of $100,000 in late

2007 to be paid out in 2008.

4. Lee acquired a Canadian subsidiary whose sole asset is a

piece of land. Lee acquired the subsidiary on 12/31/04 for the

exact value of the land, CA $100,000. Lee owns 100% of the

20. $42,0004273,031-(B) Inventory Calculation-A physical

inventory on December 31, 2013, shows 810 units on

hand.Calculate Cost of Goods Sold (COGS) using average

cost.PurchasesUnitsCostTotalBeginning

Inventory80014.3911,512January 5,

201395013.4612,787PurchaseMarch 25,

201395012.8112,170PurchaseJune 8,

201374513.6510,169PurchaseSeptember 15,

201362513.258,281PurchaseDecember 15,

201350514.977,560Purchase4,57550,967Total Purchases(C )

Error Corrections-(1) An error was discovered during 2013

relating to the understatement of depreciation expense in

2011resulting in a Prior Period Adjustment of $1,505 before

taxes.(2) ABC Company changed its method of valuing

inventory during 2013. The cumulative increase in incomefrom

the change in inventory methods was $1,285 before taxes.