Recommended

Recommended

More Related Content

Similar to Chapter 9 Exercise 31. Liquidity ratios. Edison, Stagg, and Thor.docx

Similar to Chapter 9 Exercise 31. Liquidity ratios. Edison, Stagg, and Thor.docx (20)

More from christinemaritza

More from christinemaritza (20)

Recently uploaded

Recently uploaded (20)

Chapter 9 Exercise 31. Liquidity ratios. Edison, Stagg, and Thor.docx

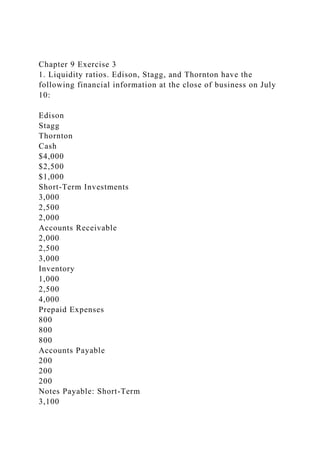

- 1. Chapter 9 Exercise 3 1. Liquidity ratios. Edison, Stagg, and Thornton have the following financial information at the close of business on July 10: Edison Stagg Thornton Cash $4,000 $2,500 $1,000 Short-Term Investments 3,000 2,500 2,000 Accounts Receivable 2,000 2,500 3,000 Inventory 1,000 2,500 4,000 Prepaid Expenses 800 800 800 Accounts Payable 200 200 200 Notes Payable: Short-Term 3,100

- 2. 3,100 3,100 Accrued Payables 300 300 300 Long-Term Liabilities 3,800 3,800 3,800 a. Compute the current and quick ratios for each of the three companies. (Round calculations to two decimal places.) Which firm is the most liquid? Why? b. Suppose Thornton is using FIFO for inventory valuation and Edison is using LIFO. Comment on the comparability of information between these two companies. c. If all short-term notes payable are due on July 11 at 8 a.m., comment on each company's ability to settle its obligation in a timely manner. Chapter 9 Exercise 4 1. Computation and evaluation of activity ratios. The following data relate to Alaska Products Inc.: 20X5 20X4 Net Credit Sales $832,000 $760,000 Cost of Goods Sold 440,000 350,000 Cash, Dec. 31 125,000 110,000 Accounts Receivable, Dec. 31 180,000

- 3. 140,000 Inventory, Dec. 31 70,000 50,000 Accounts Payable, Dec. 31 115,000 108,000 2. The company is planning to borrow $300,000 via a 90-day bank loan to cover short-term operating needs. a. Compute the accounts-receivable and inventory-turnover ratios for 20X5. Alaska rounds all calculations to two decimal places. b. Study the ratios from part (a) and comment on the company's ability to repay a bank loan in 90 days. c. Suppose that Alaska's major line of business involves the processing and distribution of fresh and frozen fish throughout the United States. Do you have any concerns about the company's inventory-turnover ratio? Briefly discuss. Chapter 9 Problem 1 1. Horizontal and vertical analysis. The following financial statements pertain to Waterloo Corporation: WATERLOO CORPORATION Comparative Balance Sheets December 31,20X5 and 20X4 20X5 20X4 Assets Current Assets Cash $ 11,250 $ 12,500 Accounts Receivable (net) 18,500 25,000 Inventories

- 4. 38,500 35,000 Prepaid Expense __3,750 __3,750 Total Current Assets $ 72,000 $ 76,250 Property, Plant, and Equipment Buildings (net) $ 102,750 $ 101,250 Equipment (net) 28,500 30,000 Vehicles (net) 32,000 40,000 Total Property, Plant, and Equipment $ 163,250 $ 171,250 Trademarks (net) __$ 14,750 __$ 2,500 Total assets $ 250,000 $ 250,000 Liabilities and Stockholders' Equity Current Liabilities Accounts Payable $ 49,000 $ 70,000 Notes Payable 13,500 40,000 Federal Taxes Payable

- 5. __2,500 __25,000 Total Current Liabilities $ 65,000 $ 135,000 Long-Term Debt __$ 50,000 __$ 25,000 Total Liabilities $ 115,000 $ 160,000 Stockholders' Equity Common Stock, $10 par $ 25,000 $ 25,000 Retained Earnings __110,000 __65,000 Total Stockholders' Equity $ 135,000 $ 90,000 Total Liabilities and Stockholders' Equity $ 250,000 $ 250,000 WATERLOO CORPORATION Comparative Income Statements For the Years Ending December 31, 20X5 and 20X4 20X5 20X4 Net Sales $ 550,000 $500,000 Cost of Goods Sold __330,000

- 6. __250,000 Gross Profit $ 220,000 $250,000 Operating Expense __132,500 __100,000 Income Before Interest and Taxes $ 87,500 $150,000 Interest Expense __12,500 __3,000 Income Before Taxes $ 75,000 $147,000 Income Tax Expense __30,000 __58,800 Net Income $ 45,000 $ 88,200 Instructions a. Prepare a horizontal analysis of the balance sheet, showing dollar and percentage changes. Round all calculations in parts (a) and (b) to two decimal places. b. Prepare a vertical analysis of the income statement by relating each item to net sales. c. Briefly comment on the results of your analysis. Chapter 9 Problem 2 2. Ratio computation. The financial statements of the Lone Pine Company follow. LONE PINE COMPANY Comparative Balance Sheets December 31, 20X2 and 20X1 ($000 Omitted)

- 7. 20X2 20X1 Assets Current Assets Cash and Short-Term Investments $ 400 $ 600 Accounts Receivable (net) 3,000 2,400 Inventories __2,000 __2,200 Total Current Assets $5,400 $5,200 Property, Plant, and Equipment Land $1,700 $ 600 Buildings and Equipment (net) __1,500 __1,000 Total Property, Plant, and Equipment $3,200 $1,600 Total Assets $8,600 $6,800 Liabilities and Stockholders' Equity Current Liabilities Accounts Payable $1,800 $1,700 Notes Payable __1,100

- 8. __1,900 Total Current Liabilities $2,900 $3,600 Long-Term Liabilities Bonds Payable 4,100 2,100 Total Liabilities $7,000 $5,700 Stockholders' Equity Common Stock $ 200 $ 200 Retained Earnings __1,400 __900 Total Stockholders' Equity $1,600 $1,100 Total Liabilities and Stockholders' Equity $8,600 $6,800 LONE PINE COMPANY Statement of Income and Retained Earnings For the Year Ending December 31,20X2 ($000 Omitted) Net Sales* $36,000 Less: Cost of Goods Sold $20,000 Selling Expense 6,000

- 9. Administrative Expense 4,000 Interest Expense 400 Income Tax Expense __2,000 _32,400 Net Income $ 3,600 Retained Earnings, Jan. 1 ___900 $ 4,500 Cash Dividends Declared and Paid __3,100 Retained Earnings, Dec. 31 $ 1,400 *All sales are on account. Instructions Compute the following items for Lone Pine Company for 20X2, rounding all calculations to two decimal places when necessary: a. Quick ratio b. Current ratio c. Inventory-turnover ratio d. Accounts-receivable-turnover ratio e. Return-on-assets ratio f. Net-profit-margin ratio g. Return-on-common-stockholders' equity h. Debt-to-total assets i. Number of times that interest is earned j. Dividend payout rate

- 10. Chapter 9 Problem 3 3. Financial statement construction via ratios. Incomplete financial statements of Lock Box Inc. are presented as follows: LOCK BOX INC. Income Statement For the Year Ending December 31, 20X3 Sales $ ? Cost of Goods Sold ? Gross Profit $ 15,000,000 Operating Expenses and Interest ? Income Before Taxes $ ? Income taxes, 40% ? Net income $ ? LOCK BOX INC. Balance Sheet December 31, 20X3 Assets Cash $ ? Accounts Receivable ?

- 11. Inventory ? Property, Plant, and Equipment ___8,000,000 Total assets $ 24,000,000 Liabilities and Stockholders' Equity Accounts Payable $ ? Notes Payable: Short-Term 600,000 Bonds Payable 4,600,000 Common Stock 2,000,000 Retained Earnings ? Total Liabilities and Stockholders' Equity $ 24,000,000 Further information is the following: · Cost of goods sold is 60% of sales. All sales are on account. · The company's beginning inventory is $5 million; inventory- turnover ratio is 4. · The debt-to-total-assets ratio is 70%.

- 12. · The profit margin on sales is 6%. · The firm's accounts-receivable-turnover ratio is 5. Receivables increased by $400,000 during the year. Instructions Using the preceding data, complete the income statement and the balance sheet. Running Head: PROJECT PERFORMANCE 1 PROJECT PERFORMANCE 9 Assignment 3: Project Performance Craig A. Alford BUS 419 – Project Estimating and Budgeting Strayer University Dr. Shah Jamali Spring quarter of 2015 Introduction This project is about the development of an improved version of Microsoft Windows 10 Enterprise Client. The new product is meant to offer better-improved service to clients and to ensure that their computing experience is smooth and secure. The project has been initiated to come up with a better functioning operating system. From the project title, one can identify that the software under development is the second version with different patches being applied to the initial software to improve it. There is need for extensive research to

- 13. be done on the new product under development so that the issues experienced in the first version are not experienced in the current version under development and that users can get a better experience from the new version as compared to the previous. Key Objectives This project is geared towards the development of a better version of the Microsoft Windows with secure implementations among other patches being developed. The need for this is to come up with a more usable operating system with more features incorporated within it. The product undergoing development is required to support integration with other operating systems to allow for a wider access with other systems and software for increased functionality. Users of the system will also receive patches and updates on previous software for increased functionality and better security as compared to peer operating systems. The aim of this is to strive to come up with a better functioning operating system with integration enabled for a smoother experience and increased usability and productivity. Projected Costs Within the project, there are some projected costs during different stages of the project development phase. For successful implementation of the project, there are a number of costs to be experienced through its lifecycle. Costs are such as staffing costs, research, purchase of software and equipment to carry out testing and development among other costs, which are bound to arise within the project. Resource Cost Research $1,500 Staffing $45,000 Certification

- 14. $1,200 Testing $3,000 Acquisition of Software Components $1,500 Purchase of Computers $15,500 Purchase of Software for Testing $950 Licensing Fees $800 Testing Environment $1,000 Totals $70,450 Resources During the project phases, there are a number of resources, which need to be set aside for the success and completion of the project. The different departments and teams 1. Human Resources The human resources required for the implementation of this project vary since there is need for multiple teams to be brought together to ensure that the requirements are met. The first team is the team doing the initial research on the project. Secondly, there is need for the project planning team. There is also need for the human resources team to be involved in the process. In addition, after the human resources team has selected members of the project, there is need for creation of sub-teams within the project for delivery of objectives and accomplishment of tasks. 2. Computers In accomplishment of this project, computers loaded with the appropriate software are necessary for purchase and implementation. The programmers need computers, which provide them with an environment where they can be able to perform adequate testing on the new platform being, developed

- 15. to ensure that it meets customer needs and requirements. 3. Finances In order for the project to reach completion, there are a number of financial implications, which have to be incurred. There is need to set and draft a budget for the project implementation. The budget should be inclusive of costs such as staffing costs, costs of purchasing 4. Time There is need for a time schedule to be outlined for the project. The project timeline needs to be developed by the project manager and then communicated to the team members, project sponsors and stakeholders so that they can know the expected period of wait from start to completion. In addition, this helps in planning for different aspects of a project to allow for successful implementation and development. Responsibility Assignment Matrix The responsibility assessment matrix is a form of a linear responsibility chart developed for purposes of description of participation by various roles as per the tasks they are carrying out or the expected deliverables of the project from them. This is a useful tool to implement for information clarity in a multi- functional department project. The most commonly used responsibilities in this matrix are Responsible (R), Accountable (A), Consulted (C) and Informed (I). The responsible party is one whose work is to achieve the task; the accountable party is the one answerable, the consulted is one whose opinions are sought and the informed is one who is kept up to date with the progress of the project (Doglione, 2016). Name Project Sponsor Project Manager System Coder System Analyst System Tester Human Resources Initiate Project

- 16. I R R I I R Research I R C C C R Staffing C R I I I R System Development I I R R R I System Testing I I R R R I System Packaging and Deployment I

- 17. I R R R I Critical Path Analysis Definition of Software Requirements There is need for definition of the minimum operational and usage requirements for the project. The need for this is that it acts as a quality control measure where a system needs to meet certain criteria before installation or usage. The specification of requirements is an important aspect so that the team responsible can be aware of what developments are to be made to the system and software. Requirement Project Plan The requirements for the project to be completed successfully need to be defined and outlined properly so that the project manager and the respective teams can be able to plan for the project appropriately. Software Integration The software in development needs to be integrated within other software for increased productivity. Integration testing needs to be carried out Software Testing and Quality Assurance The software needs to undergo testing to ensure requirements are met and that the new operating system developed is bug free and usable. There is need for different forms of testing to be applied on the new software to ensure that all components are functional. The first test will involve the installation procedures to be analyzed whether they are working as they should and whether after installation, all required components are successfully installed and are functional. In addition, there is need for a functionality test to see whether the new operating system will be operational fully and whether all components work smoothly without interruptions.

- 18. There is need for a security test to be run on the new operating system to ensure that is it robust and secure form attacks. A good operating system should be secure from virus and Trojan attacks, network attacks, backdoors and brute force among other types on computer operating systems. The system needs to have a smart screen integrated within it to ensure that new software is tested and checked for validity before installation. The user needs to receive a prompt to give them details of the software, confirm whether they want to continue with installation as well as warn them about the potential harm, which could be caused by use of the software. The system should also have secure authorization and authentication options to have increased security. The system should prompt for a password to be set during installation since most users tend to forget to set up passwords on further computer use until they experience an attack on their system. In addition, there is need for the software to be bundled with an in built firewall as a measure for protection from intrusion and other attacks. The system also needs to undergo a compatibility test to ensure that the system can be able to function with other additional software from different vendors to allow different users to be able to have their needs met. Different software and utility packages offer different users’ different needs met therefor the need for compatibility testing. Software Accreditation This is the process of validation that a software has met all requirements and can be released for use. The software can only be validated if all the checks for quality assurance are passed and that the software meets the minimum user requirements and needs. Patches and Updates There is need for periodic patches and updates to be released and configured to be downloaded automatically to allow the system to be up to date and also protected from different types of attacks which might develop over time. Also,

- 19. patches to software help in fixing possible bugs and other errors in system software, which may not manifest or be detected in the initial testing phases. Documentation It is important for a software to be tested and documented so that there can be ease f troubleshooting. This is the role of the developers of the system. A troubleshooting manual is easy to develop form the system documentation since there is outlining of all possible issues encountered and those projected to encounter during development and implementation as well as steps of development, which can be used to guide the user on what steps to take to manage issues and repair problems with functionality of an operating system. Failure to document can lead to major issues in troubleshooting since this would require the system to be analyzed anew, which would be tasking and time consuming. In addition, documentation of a project is good practice, which needs to be followed especially in an information technology project. Total Float in the Project The free float in project management refers to the total amount of time by which an activity can be delayed without the early start of the successor activity being delayed. This is achievable through the early finish date of each activity within the project being subtracted from the early start date of the next activity in the project. The total float is the total amount of time that an activity can be delayed from when it is started and the end date of the project is not delayed. The total slack refers to the total amount of time within a schedule where a task can be delayed before the completion of the entire project is delayed. There is need to identify the free slack and float times within a project for purposes of planning so that the project manager and members can be able to cater for any events that might lead to a project being delayed (Rouse, 2017). Measures for Critical Path Management and Float Reduction The critical path is a method in project management where there is identification of activities that are critical to the

- 20. project. It makes use of an approach to scheduling where the project is broken down into a number of work tasks and they are displayed in a flow chart then there is calculation of the duration Best practices for minimization are to calculate the shortest paths of processes. In addition, it is important for calculation of early starts and end dates so that slack and float can be accounted for and this can allow for better panning of activities within a project. A project needs to have free float and slack so that there is an allowance for flexibility in the event one or more tasks are slightly delayed and others are finished early. It is better for a project to be delivered before time as opposed to it being delivered after the deadline since there is an increase in costs and the budget might get overstretched. References Doglione, Cara (July 25, 2016). Understanding Responsibility Assignment Matrix (RACI Matrix). Retrieved from: https://project- management.com/understanding-responsibility- assignment-matrix-raci-matrix/ Rouse, Margaret (2017). Float (Project Float, Slack).

- 21. Retrieved from: http://whatis.techtarget.com/definition/float-project-float- slack 1. Assignment 4: Earned Value Management (EVM) Due Week 8 and worth 130 points Use the Internet or the Strayer Library to research articles on EVM. Project managers often use Earned Value Management (EVM) if they want to compare the status of their projects to their project plans. Using the same project from Assignment 3, develop a project scenario to explain the amount of work that you have completed with the funds allotted. This assignment consists of two (2) sections: · MS Project Exercise · EVM paper You must submit both sections as separate files for the completion of this assignment. Label each file name according to the section of the assignment for which it is written. Additionally, you may create and / or assume all necessary assumptions needed for the completion of this assignment. Section 1: MS Project Exercise Assume that your project is using more resources (e.g., time, money, and / or other non-labor resources, etc.) than anticipated through 50% of the project duration. 1. Update the project schedule to reflect related resource changes. 2. Produce a series of EVM reports from MS project that illustrates your project’s performance. Note: Your reports should focus on the cost and schedule performance of the project. Section 2: EVM Paper Write a two to three (2-3) page paper in which you: 3. Summarize the resource changes of your project, and discuss the performance results of your project.

- 22. 4. Determine one (1) performance measurement baseline for your MS Project. Justify your response. 5. Apply earned value analysis (EVA) in order to forecast future cost issues. Justify your response. Your assignment must follow these formatting requirements: · Typed, double spaced, using Times New Roman font (size 12), with one-inch margins on all sides; citations and references must follow APA or school-specific format. Check with your professor for any additional instructions. · Include a cover page containing the title of the assignment, the student’s name, the professor’s name, the course title, and the date. The cover page and the reference page are not included in the required assignment page length. The specific course learning outcomes associated with this assignment are: · Appraise the process of determining the cost and relevant budget required for a project component. · Analyze quality assurance processes in project management. · Use technology and information resources to research issues in project estimating and budgeting. · Write clearly and concisely about project estimating and budgeting using proper writing mechanics. Grading for this assignment will be based on answer quality, logic / organization of the paper, and language and writing skills, using the following rubric found here. Student Guidance ReportAshford University ACC205Guidance ReportWeek FiveLISTEN TO AUDIO/VIDEO EXPLAINING THE GUIDANCE REPORTYELLOW INDICATES ACCOUNT AMOUNTS CHANGEDChange Account to:Based Upon Course Start DateAccount to be changedOriginal AmountJan - FebMar-AprMay-JunJul-AugSept-OctNov-DecCh 9 Ex 3Edison Cash $4,0005,0006,0007,0008,0009,00010,000Stagg Cash

- 23. $2,5003,5004,5005,5006,5007,5008,500Thornton Cash $1,0002,0003,0004,0005,0006,0007,000QuestionsYOUR ANSWERS BASED UPON COURSE START DATECompute the current and quick ratios for each of the three companies. (Round calculations to two decimal places.) Which firm is the most liquid? Why?Edison Current ratioQuick ratioStagg Current ratioQuick ratioThorntonCurrent ratioQuick ratioSuppose Thornton is using FIFO for inventory valuation and Edison is using LIFO. Comment on the comparability of information between these two companies.If all short-term notes payable are due on July 11 at 8 a.m., comment on each company's ability to settle its obligation in a timely manner.Account to be changedOriginal AmountJan - FebMar-AprMay-JunJul-AugSept-OctNov-DecCh 9 Ex 420X5 20X420X5 20X420X5 20X420X5 20X420X5 20X420X5 20X420X5 20X4 Net Credit Sales $832,000760000.00842,000760,000852,000760,000862,000760, 000872,000760,000882,000760,000892,000760,000 Net Credit Sales $832,000$760,000 Cost of Goods Sold 440,000350000.00450,000350,000460,000350,000470,000350,0 00480,000350,000490,000350,000500,000350,000 Cost of Goods Sold 440,000350,000QuestionsYOUR ANSWERS BASED UPON COURSE START DATE The company is planning to borrow $300,000 via a 90-day bank loan to cover short-term operating needs.a. Compute the accounts-receivable and inventory-turnover ratios for 20X5Accounts Receivable TurnoverInventory TurnoverStudy the ratios from part (a) and comment on the company's ability to repay a bank loan in 90 days.Suppose that Alaska's major line of business involves the processing and distribution of fresh and frozen fish throughout the United States. Do you have any concerns about the company's inventory-turnover ratio? Briefly discuss.Account to be changedOriginal AmountJan - FebMar-AprMay-JunJul-AugSept-OctNov-DecCh 9 Pb 120X5 20X420X5 20X420X5 20X420X5 20X420X5 20X420X5 20X420X5 20X4AssetsCurrent AssetsPLACE YOUR

- 24. ANSWERS BELOW STARTING ON ROW 99Cash 1125012500.00$12,250$13,400$13,250$14,30021,50027,700$15 ,250$16,100$16,250$17,000$17,250$17,900 Accounts Receivable (net) 1850025000.0019,50025,90020,50026,80041,50037,70022,5002 8,60023,50029,50024,50030,400 Inventories 3850035000.0039,50035,90040,50036,8006,7506,45042,50038,6 0043,50039,50044,50040,400 Prepaid Expense 37503750.004,7504,6505,7505,550$75,000$78,9507,7507,3508, 7508,2509,7509,150 Total Current Assets 7200076250.00$73,000$77,150$74,000$78,050$105,750$103,95 0$76,000$79,850$77,000$80,750$78,000$81,650 Buildings (net) 102750101250.00$103,750$102,150$104,750$103,05031,50032, 700$106,750$104,850$107,750$105,750$108,750$106,650 Equipment (net) 2850030000.0029,50030,90030,50031,80035,00042,70032,5003 3,60033,50034,50034,50035,400 Vehicles (net) 3200040000.0033,00040,90034,00041,800$166,250$173,95036, 00043,60037,00044,50038,00045,400 Total Property, Plant, and Equipment 163250171250.00$164,250$172,150$165,250$173,050$17,750$ 5,200$167,250$174,850$168,250$175,750$169,250$176,650 Trademarks (net) 147502500.00$15,750$3,400$16,750$4,300$253,000$252,700$1 8,750$6,100$19,750$7,000$20,750$7,900 Total assets 250000250000.00$251,000$250,900$252,000$251,800$52,000$ 72,700$254,000$253,600$255,000$254,500$256,000$255,400 Accounts Payable 4900070000.00$50,000$70,900$51,000$71,80016,50042,700$53 ,000$73,600$54,000$74,500$55,000$75,400 Notes Payable 1350040000.0014,50040,90015,50041,8005,50027,70017,50043, 60018,50044,50019,50045,400 Federal Taxes Payable 250025000.003,50025,9004,50026,800$68,000$137,7006,50028, 6007,50029,5008,50030,400 Total Current Liabilities 65000135000.00$66,000$135,900$67,000$136,800$53,000$27,7

- 25. 00$69,000$138,600$70,000$139,500$71,000$140,400Long- Term Debt 5000025000.00$51,000$25,900$52,000$26,800$118,000$162,70 0$54,000$28,600$55,000$29,500$56,000$30,400 Total Liabilities 115000160000.00$116,000$160,900$117,000$161,800$28,000$ 27,700$119,000$163,600$120,000$164,500$121,000$165,400 Common Stock, $10 par 2500025000.00$26,000$25,900$27,000$26,800113,00067,700$2 9,000$28,600$30,000$29,500$31,000$30,400 Retained Earnings 11000065000.00111,00065,900112,00066,800$138,000$92,7001 14,00068,600115,00069,500116,00070,400 Total Stockholders' Equity 13500090000.00$136,000$90,900$137,000$91,800$253,000$25 2,700$139,000$93,600$140,000$94,500$141,000$95,400 Total Liabilities and Stockholders' Equity 250000250000.00$251,000$250,900$252,000$251,800258,0002 58,000$254,000$253,600$255,000$254,500$256,000$255,400W ATERLOO CORPORATIONComparative Income StatementsFor the Years Ending December 31, 20X5 and 20X420X5 20X420X520X420X5 20X420X520X420X5 20X420X520X420X5 20X4Net Sales 550000500000.00575,000510,000580,000520,000585,000521,00 0590,000523,000595,000525,000600,000535,000 Prepare a horizontal analysis of the balance sheet showing percentage changes from 20X4 to 20X5. Round all calculations in parts (a) and (b) to two decimal places.QuestionsYOUR ANSWERS BASED UPON COURSE START DATEWATERLOO CORPORATIONComparative Balance SheetsDecember 31,20X5 and 20X4AssetsCurrent Assets% ChangeCash Accounts Receivable (net) Inventories Prepaid Expense Total Current Assets Buildings (net) Equipment (net) Vehicles (net) Total Property, Plant, and Equipment Trademarks (net) Total assets Accounts Payable Notes Payable Federal Taxes Payable Total Current Liabilities Long-Term Debt Total

- 26. Liabilities Common Stock, $10 par Retained Earnings Total Stockholders' Equity Total Liabilities and Stockholders' Equity WATERLOO CORPORATIONComparative Income Statements Prepare a vertical analysis of the 20X5 income statement by relating each item to net sales.20X5 Net Sales Cost of Goods Sold Gross Profit Operating Expense Income Before Interest and Taxes Interest Expense Income Before Taxes Income Tax Expense Net Income Account to be changedOriginal AmountJan - FebMar-AprMay-JunJul-AugSept-OctNov-DecCh 9 Pb 2LONE PINE COMPANYComparative Balance SheetsDecember 31, 20X2 and 20X1 ($000 Omitted)20X2 20X120X2 20X120X2 20X120X2 20X120X2 20X120X2 20X120X2 20X1AssetsCurrent AssetsPLACE YOUR ANSWERS BELOW STARTING ON ROW 176 Cash and Short- Term Investments 400600.001,4001,4002,4002,2003,4003,0004,4003,8005,4004,6 006,4005,400 Accounts Receivable (net) 30002400.004,0003,2005,0004,0006,0004,8007,0005,6008,0006 ,4009,0007,200 Inventories 20002200.004,0003,0004,0003,8005,0004,6006,0005,4007,0006 ,2008,0007,000 Total Current Assets 54005200.009,4007,60011,40010,00014,40012,40017,40014,800 20,40017,20023,40019,600 Land 1700600.002,7001,4003,7002,2004,7003,0005,7003,8006,7004, 6007,7005,400 Buildings and Equipment (net) 15001000.002,5001,8003,5002,6004,5003,4005,5004,2006,5005 ,0007,5005,800 Total Property, Plant, and Equipment 32001600.005,2003,2007,2004,8009,2006,40011,2008,00013,20 09,60015,20011,200Total Assets 86006800.0014,60010,80018,60014,80023,60018,80028,60022,8 0033,60026,80038,60030,800 Accounts Payable 18001700.002,8002,5003,8003,3004,8004,1005,8004,9006,8005 ,7007,8006,500 Notes Payable 11001900.002,1002,7003,1003,5004,1004,3005,1005,1006,1005

- 27. ,9007,1006,700 Total Current Liabilities 29003600.003,9004,4004,9005,2005,9006,0006,9006,8007,9007 ,6008,9008,400 Bonds Payable 41002100.005,1002,9006,1003,7007,1004,5008,1005,3009,1006 ,10010,1006,900 Total Liabilities 70005700.009,0007,30011,0008,90013,00010,50015,00012,1001 7,00013,70019,00015,300 Common Stock Par value $1 (Par value not in original problem, but needed to calculate ratio - dividend payout rate)200200.001,2001,0002,2001,8003,2002,6004,2003,4005,20 04,2006,2005,000Number of Shares200200.001,2001,0002,2001,8003,2002,6004,2003,4005,2 004,2006,2005,000 Retained Earnings 1400900.004,4002,5005,4004,1007,4005,7009,4007,30011,4008 ,90013,40010,500 Total Stockholders' Equity 16001100.005,6003,5007,6005,90010,6008,30013,60010,70016, 60013,10019,60015,500 Total Liabilities and Stockholders' Equity 86006800.0014,60010,80018,60014,80023,60018,80028,60022,8 0033,60026,80038,60030,800LONE PINE COMPANYStatement of Income and Retained EarningsFor the Year Ending December 31,20X2 ($000 Omitted)Net Sales* 3600039,00041,00045,00046,00049,00055,000QuestionsYOUR ANSWERS BASED UPON COURSE START DATECompute the following items for Lone Pine Company for 20X2, rounding all calculations to two decimal places and do nt insert a percent symbol. Quick ratio Current ratio Inventory-turnover ratio Accounts-receivable-turnover ratio Return-on-assets ratio Net-profit-margin ratio Return-on-common-stockholders' equity Debt-to-total assets Number of times that interest is earned Dividend payout rateAccount to be changedOriginal AmountJan - FebMar-AprMay-JunJul-AugSept-OctNov-DecCh 9 Pb 3Cost of goods sold % of sales60.0%60.1%60.2%60.3%60.4%60.5%60.6%QuestionsYOU R ANSWERS BASED UPON COURSE START DATELOCK

- 28. BOX INC.Income StatementFor the Year Ending December 31, 20X3Sales Cost of Goods Sold Gross Profit Operating Expenses and Interest Income Before Taxes Income taxes, 40% Net income LOCK BOX INC.Balance SheetDecember 31, 20X3AssetsCash Accounts Receivable Inventory Property, Plant, and Equipment Total assets Liabilities and Stockholders' Equity Accounts Payable Notes Payable: Short-Term Bonds Payable Common Stock Retained Earnings Total Liabilities and Stockholders' Equity http://www.screencast.com/t/7C6URyZc5afile:///C:/Users/cpabi _000/Documents/ACC205%20Chapters/Produced%20videos/We ek%20Five/Ch%209%20Ex%203.mp4file:///C:/Users/cpabi_000/ Documents/ACC205%20Chapters/Produced%20videos/Week%2 0Five/Ch%209%20Pb%202.mp4file:///C:/Users/cpabi_000/Docu ments/ACC205%20Chapters/Produced%20videos/Week%20Five /Ch%209%20Pb%203.mp4file:///C:/Users/cpabi_000/Documents /ACC205%20Chapters/Produced%20videos/Week%20Five/Ch% 209%20Ex%204.mp4file:///C:/Users/cpabi_000/Documents/AC C205%20Chapters/Produced%20videos/Week%20Five/Ch%209 %20Pb%201.mp4