Acctba1 group business case 1st term, ay 2013-2014 (1)

1. ACCTBA1 GROUP BUSINESS CASE

1st

Term, Academic Year 2013-2014

Williams, J., Haka, S., Bettner, M., & Carcello, J. (2012)

Financial Accounting, 15th

edition, McGraw-Hill Irwin (with modifications)

BILLBOARD SCREEN is a service-type enterprise in the advertising field, and its owner-

manager, Billy Beard, has only a limited knowledge of accounting. Billy prepared the

following statement of financial position, which, although arranged satisfactorily,

contains certain errors with respect to such concepts as the business entity and asset

valuation.

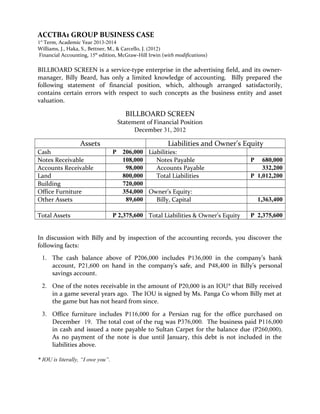

BILLBOARD SCREEN

Statement of Financial Position

December 31, 2012

Assets Liabilities and Owner’s Equity

Cash P 206,000 Liabilities:

Notes Receivable 108,000 Notes Payable P 680,000

Accounts Receivable 98,000 Accounts Payable 332,200

Land 800,000 Total Liabilities P 1,012,200

Building 720,000

Office Furniture 354,000 Owner’s Equity:

Other Assets 89,600 Billy, Capital 1,363,400

Total Assets P 2,375,600 Total Liabilities & Owner’s Equity P 2,375,600

In discussion with Billy and by inspection of the accounting records, you discover the

following facts:

1. The cash balance above of P206,000 includes P136,000 in the company’s bank

account, P21,600 on hand in the company’s safe, and P48,400 in Billy’s personal

savings account.

2. One of the notes receivable in the amount of P20,000 is an IOU* that Billy received

in a game several years ago. The IOU is signed by Ms. Panga Co whom Billy met at

the game but has not heard from since.

3. Office furniture includes P116,000 for a Persian rug for the office purchased on

December 19. The total cost of the rug was P376,000. The business paid P116,000

in cash and issued a note payable to Sultan Carpet for the balance due (P260,000).

As no payment of the note is due until January, this debt is not included in the

liabilities above.

* IOU is literally, “I owe you”.

2. - 2 -

4. Also included in the amount for office furniture is a computer that cost P101,000 but

is not on hand because Billy donated it to a local charity.

5. The “Other Assets” of P89, 600 represent the total amount of income taxes Billy has

paid the government over a period of years. Billy believes the income tax law to be

unconstitutional, and a friend who attends law school has promised to help Billy

recover the taxes paid as soon as he passes the bar exam.

6. The asset “Land” was acquired at a cost of P560,000 but was increased to a valuation

of P800,000 when one of Billy’s friends offered to pay that much for it if Billy would

move the building off the lot.

7. The accounts payable includes debts of P308,000 and the P24,200 balance owed on

Billy’s personal credit card.

8. A customer’s open account for P7,500 was erroneously recorded by the firm’s

bookkeeper as P5,700.

9. On December 31, 2012, the firm bought office supplies for P150,000, payable in 45

days. This was debited to Office Equipment and credited to Accounts Payable.

10. The firm granted on December 30, 2012 cash advance to two of its employees at

P8,500 each. This was recorded in the journal but not posted to the ledger when the

Statement of Financial Position was prepared.

INSTRUCTIONS:

a. For items 1 to 7 above, use a separate numbered paragraph to explain whether the

treatment followed by Billy is in accordance with generally accepted accounting

principles (one letter size bond paper).

b. Prepare a corrected Statement of Financial Position at December 31, 2012

(another letter size bond paper).

- 3 -

3. Format:

• Letter size bond paper (8-1/2” x 11”)

• 1.5 line spacing

• One inch margin in all sides

• Minimum of 3 pages (not including the cover page)

• Font: Arial 12

• Cover page:

Deadline: August 28, 2013 (Wednesday)

GROUP BUSINESS CASE

Presented to the

Accountancy Department

De La Salle University

In partial fulfillment

Of the course requirements

In ACTBAS1 (sec)

Surname, First Name, M.I.

Surname, First Name, M.I.

Surname, First Name, M.I.