Recommended

Recommended

More Related Content

Similar to The following information is for Henenlotter Inc. for the year end.docx

Similar to The following information is for Henenlotter Inc. for the year end.docx (20)

More from cherry686017

More from cherry686017 (20)

Recently uploaded

Recently uploaded (20)

The following information is for Henenlotter Inc. for the year end.docx

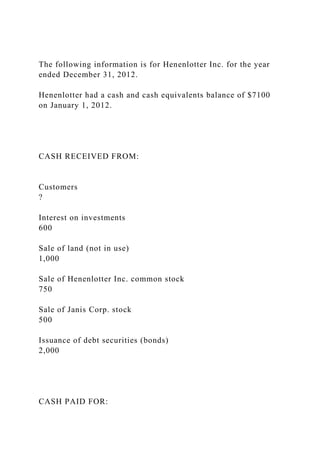

- 1. The following information is for Henenlotter Inc. for the year ended December 31, 2012. Henenlotter had a cash and cash equivalents balance of $7100 on January 1, 2012. CASH RECEIVED FROM: Customers ? Interest on investments 600 Sale of land (not in use) 1,000 Sale of Henenlotter Inc. common stock 750 Sale of Janis Corp. stock 500 Issuance of debt securities (bonds) 2,000 CASH PAID FOR:

- 2. Interest on debt 300 Income tax 80 Debt principal reduction 1,500 Purchase of equipment 4,100 Purchase of inventory 1,000 Dividends paid on Henenlotter common stock 200 Operating expenses 400 OTHER DATA Revenue 600 Accounts Receivable (Jan. 1, 2012) 1,200 Accounts Receivable (Dec. 31, 2012)

- 3. 900 Accounts written off during the year 200 Prepare a Statement of Cash Flows for the year. Use the direct method for the operating activities section. 1. Four different competent accountants independently agree on the amount and method of reporting an economic event. The concept demonstrated is: A. Reliability. B. Comparability. C. Completeness. D. Verifiability. E. All of the above 2. Which of the following best demonstrates the full disclosure principle? A. The multi-step income statement. B. The auditors' report. C. The company's tax return. D. Notes to financial statements. E. None of the above.

- 4. 3. Disclosure notes to a company's financial statements: A. Are relatively unimportant facts that don't belong in the basic financial statements. B. Document the source of financial statement facts, like literary footnotes. C. Are an integral part of a company's financial statements. D. Are irrelevant facts that are immaterial in amount. E. None of the above. 4. An important argument in support of historical cost information is: A. Relevance. B. Predictive quality for future cash flows. C. Materiality. D. Verifiability. E. All of the above 5. Primecoat Corporation could disseminate its annual financial statements two days earlier if it shifted substantial human resources from other operations to the annual report project. Management decided the value of the earlier report was not worth the added commitment of resources. The concept best demonstrated is: A. Timeliness. B. Materiality. C. Relevance. D. Cost effectiveness. E. All of the above. 6. Mega Loan Company has very stringent credit requirements and, accordingly, has negligible losses from uncollectible accounts. The company's independent accountants did not protest when, contrary to GAAP, the company recorded bad debt expense only when specific accounts were determined to be uncollectible, rather than use an allowance for uncollectible

- 5. accounts. The concept demonstrated is: A. Comparability. B. Faithful representation. C. Cost effectiveness. D. Materiality. E. Two of the above are correct. 7. Recognizing expected losses immediately, but deferring expected gains, is an example of: A. Materiality. B. Conservatism. C. Cost effectiveness. D. Timeliness. E. All of the above 8. According to the conceptual framework, verifiability implies: A. Legal evidence. B. Logic. C. Consensus. D. Legal verdict. E. None of the above. 9. Land was acquired in 2012 for a future building site at a cost of $40,000. The assessed valuation for tax purposes is $27,000, a qualified appraiser placed its value at $48,000, and a recent firm offer for the land was for a cash payment of $46,000. The land should be reported in the financial statements at: A. $40,000. B. $27,000. C. $46,000. D. $48,000. E. None of the above. 10. Of the following, the most important objective for financial reporting is to provide information useful for:

- 6. A. Making decisions. B. Determining taxable income. C. Providing accountability. D. Increasing future profits. E. Two of the above. 11. The balance in retained earnings at the end of the year is determined by retained earnings at the beginning of the year: A. Plus revenues minus liabilities. B. Plus accruals minus deferrals. C. Plus net income minus dividends. D. Plus assets minus liabilities. E. None of the above. 12. Fink Insurance collected premiums of $18,000,000 from its customers during the current year. The adjusted balance in the unearned premiums account increased from $6 million to $8 million dollars during the year. What was Fink's revenue from earned insurance premiums for the current year? A. $10,000,000. B. $16,000,000. C. $18,000,000. D. $20,000,000. E. None of the above. 13. On November 1, 2012, Tim's Toys borrows $30,000,000 at 9% to finance the holiday sales season. The note is for a six- month term and both principal and interest are payable at maturity. What should be the balance of interest payable for the loan as of December 31, 2012? A. $112,500. B. $225,000. C. $450,000. D. $1,350,000. E. None of the above.

- 7. 14. Eve's Apples opened business on January 1, 2011, and paid for two insurance policies effective that date. The liability policy was $36,000 for eighteen months, and the crop damage policy was $12,000 for a two-year term. What was the balance in Eve's prepaid insurance as of December 31, 2011? A. $9,000. B. $18,000. C. $30,000. D. $48,000. E. None of the above. 15. In its first year of operations Acme Corp. had income before tax of $400,000. Acme made income tax payments totaling $150,000 during the year and has an income tax rate of 40%. What would be the balance in income tax payable at the end of the year? A. $160,000 credit. B. $150,000 credit. C. $10,000 credit. D. $10,000 debit. E. None of the above. 16. Carolina Mills purchased $270,000 in supplies this year. The supplies account increased by $10,000 during the year to an ending balance of $66,000. What was supplies expense for Carolina Mills during the year? A. $300,000. B. $280,000. C. $260,000. D. $240,000. E. None of the above. 17. The adjusting entry required to record accrued expenses includes: A. A debit to an expense.

- 8. B. A debit to an asset. C. A credit to an asset. D. A credit to liability. E. Two of the above. 18. The adjusting entry required when amounts previously recorded as unearned revenues are earned includes: A. A debit to a liability. B. A debit to an asset. C. A credit to a liability. D. A credit to an asset. E. A debit to an expense. 19. On December 31, 2012, Coolwear, Inc. had balances in its accounts receivable and allowance for uncollectible accounts of $48,400 and $0, respectively. No receivables were written off during the year. At the end of 2012, Coolwear estimated that $2,100 in receivables would not be collected. Bad debt expense for 2012 would be: A. $0. B. $46,300. C. $1,050. D. $2,100. E. None of the above. 20. A sale on account would be recorded by: A. Debiting revenue. B. Crediting assets. C. Crediting liabilities. D. Debiting assets. E. None of the above. 21-23. Carter Appliances is preparing its annual report for the current fiscal year. The company's controller has asked for your help in determining how best to disclose information about the following items:

- 9. 21. A subsequent event. 22. Inventory costing method. 23. Allowance for uncollectible accounts. Required: Indicate whether the above items should be disclosed (A) in the summary of significant accounting policies note, (B) in a separate disclosure note, or (C) on the face of the balance sheet or (D) not included in the annual report. 24. The balance sheet reports: A. Net income at a point in time. B. Cash flows for a period of time. C. Assets and equities at a point in time. D. Assets and equities for a period of time. E. Assets and liabilities for a period of time. 25. Notes payable: A. Is a current liability account. B. Usually has a debit balance. C. Is a non-current liability account. D. Is an investment. E. Cannot determine its classification without additional information. 26. Assets do not include: A. Funds for special purposes. B. Investments. C. Paid-in capital. D. Unexpired insurance. E. Two of the above are not assets. 27. Cash equivalents would not include: A. Cash not available for current operations. B. Money market funds. C. United States treasury bills. D. Bank drafts. E. All of the above.

- 10. 28. Accrued expenses: A. Can be repaid in services rather than cash. B. Result from payment before services are received. C. Result from services received before payment. D. Are deferred charges to expense. E. Two of the above are correct. 29. The principal concern with accounting for related party transactions is: A. The size of the transactions. B. Differences between economic substance and legal form. C. The absence of legally binding contracts. D. The lack of accurate data to record transactions. E. All of the above. 30. A subsequent event for an entity with a December 31, 2012, year-end would not include: A. A change in the estimated useful lives of equipment in January 2013. B. An issuance of bonds in January 2013. C. An acquisition of another company in January 2013. D. A major uncertainty at December 31, resolved in January 2013. E. All of the above. 31. Popson Inc. incurred a material loss which was not unusual in character, but was clearly an infrequent occurrence. This loss should be reported as: A. An extraordinary loss. B. A separate line item between income from continuing operations and income from discontinued operations. C. A separate line item within income from continuing operations. D. A separate line item within income from noncontinuing operations.

- 11. E. A separate line item in the retained earnings statement. 32. Freda's Florist reported the following before-tax income statement items for the year ended December 31, 2012: Operating income 250,000 Extraordinary gain 70,000 All income statement items are subject to a 40% income tax rate. In its 2012 income statement, Freda's separately stated income tax expense would be __________________and total income tax expense would be____________________. 33. The principal benefit of separately reporting discontinued operations and extraordinary items is to enhance: A. Predictive ability. B. Consistency in reporting. C. Intraperiod continuity. D. Comprehensive reporting. E. All of the above. 34. On August 1, 2012, Rocket Retailers adopted a plan to discontinue its catalog sales division, which qualifies as a separate component of the business according to GAAP regarding discontinued operations. The disposal of the division was expected to be concluded by June 30, 2013. On January 31, 2013, Rocket's fiscal year-end, the following information relative to the discontinued division was accumulated: Operating loss Feb. 1, 2012 – Jan. 31, 2013 115,000 Estimated operating losses Feb. 1 to June 30, 2013 80,000 Impairment of division assets at Jan. 31, 2012

- 12. 10,000 In its income statement for the year ended January 31, 2012, Rocket would report a before-tax loss on discontinued operations of ___________________. 35. On October 28, 2012, Mercedes Company committed to a plan to sell a division that qualified as a component of the entity according to GAAP regarding discontinued operations and was properly classified as held for sale on December 31, 2012, the end of the company's fiscal year. The division's loss from operations for 2012 was $2,000,000.The division's book value and fair value less cost to sell on December 31 were $3,000,000 and $2,500,000, respectively. What before-tax amount should Mercedes report on discontinued operations in its 2012 income statement? (State the amount followed by gain OR loss OR impairment loss) 36. Major Co. reported 2012 income of $300,000 from continuing operations before income taxes and a before-tax extraordinary loss of $80,000. All income is subject to a 30% tax rate. In the 2012 income statement, Major Co. would show the following line-item amounts for income tax expense _________________________and net income__________________________. 37 and 38. Misty Company reported the following before-tax items during the current year: Sales 600 Operating expenses 250 Restructuring charges 20

- 13. Extraordinary loss 50 Misty's effective tax rate is 40%. 37. What would be Misty's income before extraordinary item(s)? 38. What would be Misty's net income for the current year? 39. The Maytag Corporation's income statement includes income from continuing operations, a loss from discontinued operations, and extraordinary items. Earnings per share information would be provided for: A. Net income only. B. Income from continuing operations and net income only. C. Income from continuing operations, loss from discontinued operations and net income only. D. Income from continuing operations, loss from discontinued operations, extraordinary items and net income. 40. The statement of cash flows reports cash flows from the activities of: A. Operating, purchasing, and investing. B. Borrowing, paying, and investing. C. Financing, investing, and operating. D. Using, investing, and financing. Test 1 will remain open until 7 PM on Saturday, October 5. There will be no time extensions. Part A is objective questions; you will need to download them. Answers are to be entered on the separate answer sheet. Only 1

- 14. submission will be allowed. Several of these are fill in the blank. Use the following instructions: Do not use dollar signs, do not use the decimal point (if rounding is necessary, round to the nearest dollar) , do use the comma separator (for amounts higher than 999). Part B will be sent as an attachment. If you are not using Excel, it must be formatted in a WORD table or it will not be accepted. Only 1 submission will be allowed.