Exercise 18-1Financial information for Sinead Inc. is pr.docx

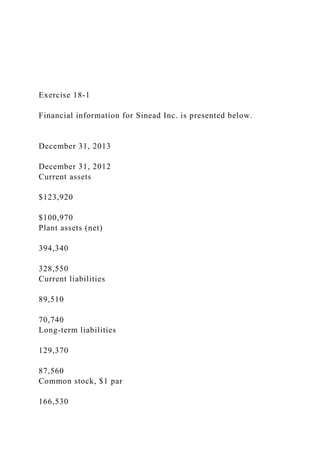

Exercise 18-1 Financial information for Sinead Inc. is presented below. December 31, 2013 December 31, 2012 Current assets $123,920 $100,970 Plant assets (net) 394,340 328,550 Current liabilities 89,510 70,740 Long-term liabilities 129,370 87,560 Common stock, $1 par 166,530 116,400 Retained earnings 132,850 154,820 Prepare a schedule showing a horizontal analysis for 2013 using 2012 as the base year. (If amount and percentage are a decrease show the numbers as negative, e.g. -55,000, -20% or (55,000). (20%). Round percentages to 1 decimal place, e.g. 12.3%.) SINEAD INC. Condensed Balance Sheets December 31 Increase or (Decrease) 2013 2012 Amount Percentage Assets Current Assets $123,920 $100,970 $ % Plant Assets (net) 394,340 328,550 % Total assets $518,260 $429,520 $ % Liabilities Current Liabilities $89,510 $70,740 $ % Long-term Liabilities 129,370 87,560 % Total liabilities 218,880 158,300 % Stockholders' Equity Common Stock, $1 par 166,530 116,400 % Retained Earnings 132,850 154,820 % Total stockholders' equity 299,380 271,220 % Total liabilities and stockholders' equity $518,260 $429,520 $ % Exercise 18-2 Operating data for Krystal Corporation are presented below. 2013 2012 Net sales $747,550 $596,800 Cost of goods sold 466,890 393,490 Selling expenses 123,640 70,370 Administrative expenses 56,450 54,540 Income tax expense 30,120 25,260 Net income 70,450 53,140 Prepare a schedule showing a vertical analysis for 2013 and 2012. (Round all answers to 1 decimal place, e.g. 48.5%.) KRYSTAL CORPORATION Condensed Income Statements For the Years Ended December 31 2013 2012 Amount Percent Amount Percent Net sales $747,550 % $596,800 % Cost of goods sold 466,890 % 393,490 % Gross margin 280,660 % 203,310 % Selling expenses 123,640 % 70,370 % Administrative expenses 56,450 % 54,540 % Total operating expenses 180,090 % 124,910 % Income before income taxes 100,570 % 78,400 % Income taxes expense 30,120 % 25,260 % Net income $70,450 % $53,140 % Comparative statement data for Lionel Company and Barrymore Company, two competitors, appear below. All balance sheet data are as of December 31, 2013, and December 31, 2012. Lionel Company Barrymore Company 2013 2012 2013 2012 Net sales $1,576,018 $339,804 Cost of goods sold 1,008,289 240,939 Operating expenses 300,593 78,336 Interest expense 8,640 2,920 Income tax expense 54,924 6,370 Current assets 320,222 $314,105 83,452 $ 78,542 Plant assets (net) 519,420 498,249 139,245 125,702 Current liabilities 64,200 74,053 34,295 28,136 Long-term liabilities 107,950 90,407 28,915 25,879 Common stock, $10 par 496,000 496,000 120,000 120,000 Retained earnings 171,492 151,894 39,487 30,229 Warning Don't show me this message again for the assi ...

Recommended

Recommended

More Related Content

Similar to Exercise 18-1Financial information for Sinead Inc. is pr.docx

Similar to Exercise 18-1Financial information for Sinead Inc. is pr.docx (11)

More from gitagrimston

More from gitagrimston (20)

Recently uploaded

Recently uploaded (20)

Exercise 18-1Financial information for Sinead Inc. is pr.docx

- 1. Exercise 18-1 Financial information for Sinead Inc. is presented below. December 31, 2013 December 31, 2012 Current assets $123,920 $100,970 Plant assets (net) 394,340 328,550 Current liabilities 89,510 70,740 Long-term liabilities 129,370 87,560 Common stock, $1 par 166,530

- 2. 116,400 Retained earnings 132,850 154,820 Prepare a schedule showing a horizontal analysis for 2013 using 2012 as the base year. (If amount and percentage are a decrease show the numbers as negative, e.g. -55,000, -20% or (55,000). (20%). Round percentages to 1 decimal place, e.g. 12.3%.) SINEAD INC. Condensed Balance Sheets December 31 Increase or (Decrease) 2013 2012 Amount Percentage Assets

- 3. Current Assets $123,920 $100,970 $ % Plant Assets (net) 394,340 328,550 % Total assets $518,260 $429,520

- 5. % Total liabilities 218,880 158,300 % Stockholders' Equity Common Stock, $1 par 166,530 116,400 %

- 6. Retained Earnings 132,850 154,820 % Total stockholders' equity 299,380 271,220 % Total liabilities and stockholders' equity $518,260 $429,520 $ %

- 7. Exercise 18-2 Operating data for Krystal Corporation are presented below. 2013 2012 Net sales $747,550 $596,800 Cost of goods sold 466,890 393,490 Selling expenses 123,640 70,370 Administrative expenses 56,450 54,540 Income tax expense 30,120 25,260 Net income

- 8. 70,450 53,140 Prepare a schedule showing a vertical analysis for 2013 and 2012. (Round all answers to 1 decimal place, e.g. 48.5%.) KRYSTAL CORPORATION Condensed Income Statements For the Years Ended December 31 2013 2012 Amount Percent Amount Percent Net sales $747,550 % $596,800 % Cost of goods sold 466,890 % 393,490

- 9. % Gross margin 280,660 % 203,310 % Selling expenses 123,640 % 70,370 % Administrative expenses 56,450 % 54,540 % Total operating expenses 180,090 % 124,910 % Income before income taxes 100,570

- 10. % 78,400 % Income taxes expense 30,120 % 25,260 % Net income $70,450 % $53,140 % Comparative statement data for Lionel Company and Barrymore Company, two competitors, appear below. All balance sheet data are as of December 31, 2013, and December 31, 2012. Lionel Company Barrymore Company 2013 2012

- 11. 2013 2012 Net sales $1,576,018 $339,804 Cost of goods sold 1,008,289 240,939 Operating expenses 300,593 78,336 Interest expense 8,640

- 12. 2,920 Income tax expense 54,924 6,370 Current assets 320,222 $314,105 83,452 $ 78,542 Plant assets (net) 519,420 498,249 139,245 125,702 Current liabilities 64,200 74,053

- 13. 34,295 28,136 Long-term liabilities 107,950 90,407 28,915 25,879 Common stock, $10 par 496,000 496,000 120,000 120,000 Retained earnings 171,492 151,894 39,487 30,229 Warning Don't show me this message again for the assignment Ok Cancel

- 14. (a) Prepare a vertical analysis of the 2013 income statement data for Lionel Company and Barrymore Company in columnar form. (Round percentages to 1 decimal place, e.g. 12.1%.) Condensed Income Statement For the Year Ended December 31, 2013 Lionel Company Barrymore Company Dollars Percent Dollars Percent $ %

- 16. % % % % % % $ %

- 17. $ % Problem 18-2A The comparative statements of Larker Tool Company are presented below. LARKER TOOL COMPANY Income Statement For the Years Ended December 31 2013 2012 Net sales $1,818,550 $1,747,770 Cost of goods sold 1,007,430 973,740 Gross profit 811,120 774,030

- 18. Selling and administrative expense 513,100 474,200 Income from operations 298,020 299,830 Other expenses and losses Interest expense 18,080 14,010 Income before income taxes 279,940 285,820 Income tax expense 80,510 76,850 Net income $ 199,430 $ 208,970

- 19. LARKER TOOL COMPANY Balance Sheets December 31 Assets 2013 2012 Current assets Cash $60,940 $64,870 Short-term investments 69,730 49,980 Accounts receivable (net) 117,930 102,100 Inventory 123,140 114,700 Total current assets 371,740

- 20. 331,650 Plant assets (net) 597,060 518,860 Total assets $968,800 $850,510 Liabilities and Stockholders’ Equity Current liabilities Accounts payable $160,110 $145,780 Income taxes payable 42,620 41,460 Total current liabilities 202,730

- 21. 187,240 Bonds payable 204,100 204,100 Total liabilities 406,830 391,340 Stockholders’ equity Common stock ($5 par) 276,000 300,000 Retained earnings 285,970 159,170 Total stockholders’ equity 561,970 459,170 Total liabilities and stockholders’ equity $968,800 $850,510

- 22. All sales were on account. Compute the following ratios for 2013. (Weighted-average common shares in 2013 were 55,700.) (Round Earnings per share to 2 decimal places, e.g.1.65, and all others to 1 decimal place, e.g. 6.8 or 6.8% .) (a) Earnings per share $ (b) Return on common stockholders’ equity % (c) Return on assets % (d) Current ratio :1 (e) Acid-test ratio

- 23. :1 (f) Receivables turnover times (g) Inventory turnover times (h) Times interest earned times (i) Asset turnover times (j) Debt to total assets % Brief Exercise 19-1

- 24. Complete the following comparison table between managerial and financial accounting. Financial Accounting Managerial Accounting Primary users Types of reports Frequency of reports

- 25. Purpose of reports Content of reports Verification Brief Exercise 19-2 (Essay) The Sarbanes-Oxley Act of 2002 (SOX) has important implications for the financial community. Explain two implications of SOX.

- 26. Brief Exercise 19-3 Identify which of the following statements best describes the functions of the management of an organization. (a) requires management to look ahead and to establish objectives. A key objective of management is to add value to the business (b) involves coordinating the diverse activities and human resources of a company to produce a smooth-running operation. This function relates to the implementation of planned objectives. (c)

- 27. is the process of keeping the activities on track. Management must determine whether goals are being met and what changes are necessary when there are deviations. Determine whether each of the following costs should be classified as direct materials (DM), direct labor (DL), or manufacturing overhead (MO). (a) Frames and tires used in manufacturing bicycles. (b) Wages paid to production workers. (c) Insurance on factory equipment and machinery.

- 28. (d) Depreciation on factory equipment. Problem 19-1A Fabila Company specializes in manufacturing a unique model of bicycle helmet. The model is well accepted by consumers, and the company has enough orders to keep the factory production at 11,350 helmets per month (80% of its full capacity). Fabila’s monthly manufacturing cost and other expense data are as follows. Rent on factory equipment $7,380 Insurance on factory building 1,720 Raw materials (plastics, polystyrene, etc.) 79,630 Utility costs for factory 500 Supplies for general office 100 Wages for assembly line workers 40,700 Depreciation on office equipment 860

- 29. Miscellaneous materials (glue, thread, etc.) 2,120 Factory manager’s salary 5,690 Property taxes on factory building 550 Advertising for helmets 14,610 Sales commissions 7,050 Depreciation on factory building 1,400 (a) Prepare an answer sheet. Enter each cost item on your answer sheet, placing the dollar amount under the appropriate headings. Total the dollar amounts in each of the columns. Product Costs Cost Item Direct Materials Direct Labor Manufacturing Overhead

- 30. Period Costs Rent on factory equipment $ $ $ $ Insurance on factory building Raw materials Utility costs for factory

- 31. Supplies for general office Wages for assembly line workers Depreciation on office equipment Miscellaneous materials

- 32. Factory manager’s salary Property taxes on factory building Advertising for helmets Sales commissions

- 33. Depreciation on factory building $ $ $ $ (b) Compute the cost to produce one helmet. (Round answer to 2 decimal places, e.g. 1.25.) The cost to produce one helmet $ Brief Exercise 21-1 Mendez Manufacturing (a) purchases $45,200 of raw materials on account, and (b) it incurs $51,060 of factory labor costs. Journalize the two transactions on March 31 assuming the labor costs are not paid until April. (Credit account titles are automatically indented when amount is entered. Do not indent manually.)

- 34. No. Account Titles and Explanation Debit Credit a. b. List Of Accounts Close Brief Exercise 21-1 Accounts Payable Accounts Receivable Cash Cost of Goods Sold Factory Labor Factory Wages Payable Finished Goods Inventory Manufacturing Overhead Raw Materials Inventory Salaries and Wages Payable Sales Work in Process - Assembly Work in Process - Blending

- 35. Work in Process - Canning Work in Process - Cooking Work in Process - Cutting Work in Process - Finishing Work in Process - Machining Work in Process - Mixing Work in Process - Packaging Brief Exercise 21-2 Mendez Manufacturing (a) purchases $38,050 of raw materials on account, (b) and it incurs $54,970 of factory labor costs. Supporting records show that the Assembly Department used $27,030 of raw materials and $26,450 of the factory labor, and the Finishing Department used the remainder. Journalize the assignment of the costs to the processing departments on March 31. (Credit account titles are automatically indented when amount is entered. Do not indent manually.) No. Account Titles and Explanation Debit Credit (a) (b)

- 36. List Of Accounts Close Brief Exercise 21-2 Accounts Payable Accounts Receivable Cash Cost of Goods Sold Factory Labor Factory Wages Payable Finished Goods Inventory Manufacturing Overhead Raw Materials Inventory Salaries and Wages Payable Sales Work in Process - Assembly Work in Process - Blending Work in Process - Canning Work in Process - Cooking Work in Process - Cutting Work in Process - Finishing Work in Process - Machining Work in Process - Mixing Work in Process - Packaging Brief Exercise 21-3

- 37. Mendez Manufacturing (a) purchases $45,580 of raw materials on account, (b) and it incurs $51,930 of factory labor costs. Supporting records show that the Assembly Department used $25,230 of raw materials and $25,880 of the factory labor, and the Finishing Department used the remainder. Manufacturing overhead is assigned to departments on the basis of 190% of labor costs. Journalize the assignment of overhead to the Assembly and Finishing Departments. (Credit account titles are automatically indented when amount is entered. Do not indent manually.) Account Titles and Explanation Debit Credit List Of Accounts Close Brief Exercise 21-3 Accounts Payable Accounts Receivable Cash Cost of Goods Sold Factory Labor Factory Wages Payable Finished Goods Inventory Manufacturing Overhead Raw Materials Inventory Salaries and Wages Payable

- 38. Sales Work in Process - Assembly Work in Process - Blending Work in Process - Canning Work in Process - Cooking Work in Process - Cutting Work in Process - Finishing Work in Process - Machining Work in Process - Mixing Work in Process - Packaging Brief Exercise 22-4 Moines Company accumulates the following data concerning a mixed cost, using miles as the activity level. Miles Driven Total Cost Miles Driven Total Cost January 8,940 $14,180 March 9,440 $16,018

- 39. February 7,710 13,250 April 9,140 14,460 Compute the variable and fixed cost elements using the high- low method. (Round Variable cost to 2 decimal places, e.g. $1.37) Variable cost per mile $ Fixed cost $ Brief Exercise 22-5 Determine the missing amounts. (Round Contribution Margin Ratio to 0 decimal places, e.g. 32%) Unit Selling Price Unit Variable Costs Contribution Margin per Unit Contribution Margin Ratio

- 40. 1. $300 $198 $ % 2. $300 $ $117 % 3. $ $ $270 27 % Brief Exercise 22-9 Sylvia Manufacturing Inc. had sales of $2,425,260 for the first quarter of 2012. In making the sales, the company incurred the

- 41. following costs and expenses. Variable Fixed Cost of goods sold $763,520 $538,840 Selling expenses 90,570 56,950 Administrative expenses 83,020 63,050 Prepare a CVP income statement for the quarter ended March 31, 2012. SYLVIA MANUFACTURING INC. Income Statement For the Quarter Ended March 31, 2012 $ $

- 42. $ Exercise 22-5 In the month of June, Bonita Beauty Salon gave 3,330 haircuts, shampoos, and permanents at an average price of $30. During the month, fixed costs were $18,600 and variable costs

- 43. were 60% of sales. Warning Don't show me this message again for the assignment Ok Cancel (a) Determine the contribution margin in dollars, per unit, and as a ratio. (Round the contribution ratio to 0 decimal places, e.g. 27%) Contribution Margin in Dollars $ Contribution Margin Per Unit $ Contribution Margin Ratio %

- 44. Exercise 23-3 Ernst and Anderson, CPAs, are preparing their service revenue (sales) budget for the coming year (2012). The practice is divided into three departments: auditing, tax, and consulting. Billable hours for each department, by quarter, are provided below. Department Quarter 1 Quarter 2 Quarter 3 Quarter 4 Auditing 2,030 1,580 2,060 2,290 Tax 2,950 2,370 2,190

- 45. 2,380 Consulting 1,610 1,610 1,610 1,610 Average hourly billing rates are: auditing $84, tax $88, and consulting $101. Prepare the service revenue (sales) budget for 2012 by listing the departments and showing for each quarter and the year in total, billable hours, billable rate, and total revenue. ERNST AND ANDERSON, CPAs Sales Revenue Budget For the Year Ending December 31, 2012 Quarter 1 Quarter 2 Dept. Billable Hours Billable Rate Total Rev. Billable Hours Billable Rate Total Rev. Auditing

- 47. ERNST AND ANDERSON, CPAs Sales Revenue Budget For the Year Ending December 31, 2012 Dept. Quarter 3 Quarter 4 Billable Hours Billable Rate Total Rev. Billable Hours Billable Rate Total Rev. Auditing $ $ $ $ Tax Consulting

- 48. Totals $ $ ERNST AND ANDERSON, CPAs Sales Revenue Budget For the Year Ending December 31, 2012 Year Dept. Billable Hours Billable Rate Total Rev. Auditing $ $ Tax Consulting Totals $

- 49. Exercise 23-5 Paseo Industries has adopted the following production budget for the first 4 months of 2013. Month Units Month Units January 10,160 March 5,490 February 8,280 April 3,680 Each unit requires 5 pounds of raw materials costing $2 per pound. On December 31, 2012, the ending raw materials inventory was 9,310 pounds. Management wants to have a raw materials inventory at the end of the month equal to 30% of next month’s production requirements. Prepare a direct materials purchases budget by month for the first quarter. PASEO INDUSTRIES

- 50. Direct Materials Purchases Budget For the Quarter Ending March 31, 2013 January February March :

- 51. : $ $

- 52. $ $ $ $ Exercise 23-8 Tye Company is preparing its manufacturing overhead budget for 2012. Relevant data consist of the following. Units to be produced (by quarters): 11,200, 11,900, 16,900, 16,100. Direct labor: Time is 1.4 hours per unit. Variable overhead costs per direct labor hour: Indirect materials $0.6; indirect labor $1.2; and maintenance $0.4. Fixed overhead costs per quarter: Supervisory salaries $35,600; depreciation $17,000; and maintenance $11,300. Prepare the manufacturing overhead budget for the year, showing quarterly data. (Round overhead rate to 2 decimal places, e.g. $2.58) TYE COMPANY Manufacturing Overhead Budget For the Year Ending December 31, 2012 Quarter

- 55. Exercise 23-13 Blue Lagoon Corporation is projecting a cash balance of $31,155 in its December 31, 2011, balance sheet. Blue Lagoon’s schedule of expected collections from customers for the first quarter of 2012 shows total collections of $179,582. The schedule of expected payments for direct materials for the first quarter of 2012 shows total payments of $40,707. Other information gathered for the first quarter of 2012 is: sale of equipment $3,867, direct labor $69,922, manufacturing overhead $35,411, selling and administrative expenses $45,196 and purchase of securities $12,292. Blue Lagoon wants to maintain a balance of at least $24,984 cash at the end of each quarter. Prepare a cash budget for the first quarter. BLUE LAGOON CORPORATION

- 56. Cash Budget For the Quarter Ended March 31, 2012 $ Add: Less:

- 57. $