Marginal costing is a type of flexible standard costing that separates fixed costs from variable costs. It is a comprehensive method for planning and monitoring costs based on resource drivers. Marginal costing ensures cost fluctuations from changes in operating levels are accurately predicted and incorporated into variance analysis. It has become widely accepted in business over the last 50 years. Marginal cost is the change in total cost from producing one more unit. It includes any additional costs to produce the next unit and varies depending on production levels and time periods considered. The relationship between marginal cost and economies of scale depends on whether average or marginal costs are falling or rising with production. Externalities can cause private and social costs to diverge.

![Marginal Costing is a type of flexible standard costing that

separates fixed costs from proportional costs in relation to the

output quantity of the objects. In particular, Marginal Costing is a

comprehensive and sophisticated method of planning and

monitoring costs based on resource drivers. Selecting the resource

drivers and separating the costs into fixed and proportional

components ensures that cost fluctuations caused by changes in

operating levels, as defined by marginal analysis, are accurately

predicted as changes in authorized costs and incorporated into

variance analysis.

This form of internal management accounting has become widely

accepted in business practice over the last 50 years. During this

time, however, the demands placed on costing systems by cost

management requirements have changed radically.

MARGINAL COST

In economics and finance, marginal cost is the change in total cost

that arises when the quantity produced changes by one unit. It is

the cost of producing one more unit of a good.[1] Mathematically, the

marginal cost (MC) function is expressed as the first derivative of

the total cost (TC) function with respect to quantity (Q). Note that

the marginal cost may change with volume, and so at each level of

production, the marginal cost is the cost of the next unit produced.

A typical Marginal Cost Curve](https://image.slidesharecdn.com/17009209-marginal-costing-120225234555-phpapp02/85/Marginal-costing-2-320.jpg)

![[edit] Negative externalities of production

Negative Externalities of Production

Much of the time, private and social costs do not diverge from one

another, but at times social costs may be either greater or less than

private costs. When marginal social costs of production are greater

than that of the private cost function, we see the occurrence of a

negative externality of production. Productive processes that result

in pollution are a textbook example of production that creates

negative externalities.

Such externalities are a result of firms externalizing their costs onto

a third party in order to reduce their own total cost. As a result of

externalizing such costs we see that members of society will be

negatively affected by such behavior of the firm. In this case, we

see that an increased cost of production on society creates a social

cost curve that depicts a greater cost than the private cost curve.

In an equilibrium state we see that markets creating negative

externalities of production will overproduce that good. As a result,

the socially optimal production level would be lower than that

observed.

Positive externalities of production

Positive Externalities of Production

When marginal social costs of production are less than that of the

private cost function, we see the occurrence of a positive externality

of production. Production of public goods are a textbook example of

production that create positive externalities. An example of such a](https://image.slidesharecdn.com/17009209-marginal-costing-120225234555-phpapp02/85/Marginal-costing-5-320.jpg)

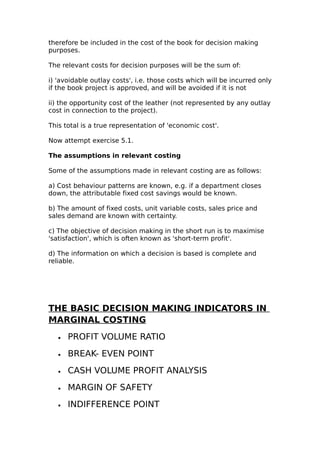

![The algebraic equation for break-even analysis consists of four

factors. If you know any three of the four, you can solve for

the fourth factor. You calculate the break-even amount with

the following equation:

Sales Price per Unit * Quantity Sold = Fixed Costs + [Variable

Costs per Unit * Quantity Sold]

For example, assume you have total fixed monthly costs of

$1200 and total variable costs of $6 per unit. If you could sell

the units for $10 each, the equation indicates that you need to

sell 300 units to break even. If you knew you could sell 400

units, the equation would indicate that the sales price would

need to be $9 per unit to break even.

• When managing inventory, you should aim for the Economic

Order Quantity (EOQ). This is the level of inventory that

balances two kinds of inventory costs: holding (or carrying)

costs, which increase with the amount of inventory ordered,

and order costs, which decrease with the amount ordered.

• The largest components of holding costs for most companies

are the cost of space to store the inventory and the cost of

tying up capital in inventory. Other components include the

labour costs associated with inventory maintenance and

insurance costs. Also include deterioration, spoilage, and

obsolescence costs. The costs of more frequent orders include

lost discounts for larger quantity purchases and labour and

supply costs of writing the orders. Additional costs include

paying the bills and processing the paperwork, associated

telephone and mail costs, and the labour costs of processing

and inspecting incoming inventory.](https://image.slidesharecdn.com/17009209-marginal-costing-120225234555-phpapp02/85/Marginal-costing-19-320.jpg)

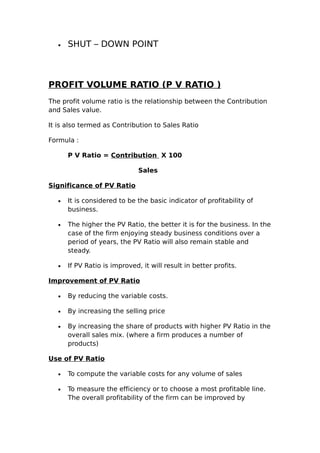

![• EOQ is the size of order that minimizes the total of holding

and ordering costs. The algebraic expression of EOQ is as

follows:

EOQ = square root of [2*U*O divided by H] where U is the

number of units used annually, O is the order cost per order,

and H is the holding cost per unit.

For example, assume you use 40,000 units annually, it costs

$50 to place an order, and it costs $20 to hold the raw

materials for one unit. The equation yields an amount of 447,

which is the number of units you need to order at one time to

minimize total costs.

The reorder point, or Economic Order Point (EOP), tells you

when to place an order. Calculating the reorder point requires

you to know the lead time from placing to receiving an order.

You compute it as follows:

EOP = Lead time * Average usage per unit of time

For example, assume you need 6400 units evenly throughout the

year, there is a lead time of one week, and there are 50 working

weeks in the year. You calculate the reorder point to be 128 units as

follows.

1 week * [6400 units / 50 weeks] = 128 units

You might also consider “Just In Time” inventory management, if

available and appropriate. “Just In Time” allows you to keep minimal

inventory in stock. You only order when you make a sale. Carefully

analyze the time lag. You must be able to satisfy the customer as

well as keep your inventory investment minimized.

Use of BEP Analysis In capital budgeting

Break even analysis is a special application of sensitivity analysis. It

aims at finding the value of individual variables which the project’s

NPV is zero. In common with sensitivity analysis, variables selected

for the break even analysis can be tested only one at a time.

The break even analysis results can be used to decide abandon of

the project if forecasts show that below break even values are likely

to occur.

In using break even analysis, it is important to remember the

problem associated with sensitivity analysis as well as some

extension specific to the method:

• Variables are often interdependent, which makes examining

them each individually unrealistic.](https://image.slidesharecdn.com/17009209-marginal-costing-120225234555-phpapp02/85/Marginal-costing-20-320.jpg)