Recommended

More Related Content

Similar to Sheet1Date (Month)Adjusted Closing Price for TESLAAdjusted Closing.docx

Similar to Sheet1Date (Month)Adjusted Closing Price for TESLAAdjusted Closing.docx (20)

More from bagotjesusa

More from bagotjesusa (20)

Recently uploaded

Recently uploaded (20)

Sheet1Date (Month)Adjusted Closing Price for TESLAAdjusted Closing.docx

- 1. Sheet1Date (Month)Adjusted Closing Price for TESLAAdjusted Closing Price for GMAdjusted Closing for NASDAQ1/3/1124.132.5930372700.0800782/1/1123.88999929. 9491482782.270023/1/1127.7527.7161392781.0700684/1/1127. 628.6629352873.5400395/2/1130.13999928.4128362835.300049 6/1/1129.12999927.1176912773.520027/1/1128.1724.72390427 56.3798838/1/1124.7421.4637072579.4599619/1/1124.3899991 8.0248682415.39990210/3/1129.37000123.0893382684.4099121 1/1/1132.74000219.0163272620.34008812/1/1128.55999918.10 52572605.1499021/3/1229.0721.4547752813.8400882/1/1233.4 123.2411842966.8898933/1/1237.24000222.9106963091.570068 4/2/1233.13000120.5437053046.3601075/1/1229.519.82914228 27.3400886/1/1231.29000117.6139932935.0500497/2/1227.421 7.6050612939.520028/1/1228.5219.0699183066.9599619/4/122 9.28000120.3204043116.2299810/1/1228.12999922.7767162977 .2299811/1/1233.8223.1161333010.2399912/3/1233.86999925.7 510873019.510011/2/1337.50999825.0901173142.1298832/1/13 34.83000224.2505043160.1899413/1/1337.88999924.848951326 7.520024/1/1353.99000227.5464293328.7900395/1/1397.76000 230.2707023455.9099126/3/13107.36000129.7526453403.257/1 /13134.27999932.0392463626.3701178/1/1316930.4404133589. 8701179/3/13193.36999532.1285713771.4799810/1/13159.9400 0233.003913919.70996111/1/13127.27999934.5938114059.8898 9312/2/13150.42999336.5052684176.5898441/2/14181.4100043 2.2268224103.8798832/3/14244.80999832.3340074308.1201173 /3/14208.44999731.0170564198.9902344/1/14207.88999931.07 11254114.5600595/1/14207.77000431.1612424242.6201176/2/1 4240.05999832.9840134408.1801767/1/14223.30000330.730558 4369.770028/1/14269.70001231.6210354580.270029/2/14242.6 7999329.2762834493.39013710/1/14241.69999728.7813194630. 74023411/3/14244.52000430.6420214791.62988312/1/14222.41 000432.2840394736.0498051/2/15203.60000630.1662944635.24 02342/2/15203.33999634.503514963.5297853/2/15188.7700043 4.963944900.8798834/1/15226.05000332.6889534941.4199225/

- 2. 1/15250.80000333.5374115070.0297856/1/15268.2600131.3977 974986.8701177/1/15266.14999429.6833045128.2797858/3/152 49.05999827.7333074776.5097669/1/15248.39999428.62762146 20.16015610/1/15206.92999333.2908135053.7511/2/15230.259 99534.5209855108.66992212/1/15240.00999532.7741515007.41 0156 Sheet2 Company Stock's Performance Tesla 40546 40575 40603 40634 40665 40695 40725 40756 40787 40819 40848 40878 40911 40940 40969 41001 41030 41061 41092 41122 41156 41183 41214 41246 41276 41306 41334 41365 41395 41428 41456 41487 41520 41548 41579 41610 41641 41673 41701 41730 41760 41792 41821 41852 41884 41913 41946 41974 42006 42037 42065 42095 42125 42156 42186 42219 42248 42278 42310 42339 24.1 23.889999 27.75 27.6 30.139999 29.129999000000002 28.17 24.74 24.389999 29.370000999999998 32.740001999999997 28.559999000000001 29.07 33.409999999999997 37.240001999999997 33.130001 29.5 31.290001 27.42 28.52 29.280000999999999 28.129999000000002 33.82 33.869999 37.509998000000003 34.830002 37.889999000000003 53.990001999999997 97.760002 107.360001 134.279999 169 193.36999499999999 159.94000199999999 127.279999 150.429993 181.41000399999999 244.80999800000001 208.449997 207.88999899999999 207.770004 240.05999800000001 223.300003 269.70001200000002 242.679993 241.699997 244.520004 222.41000399999999

- 3. 203.60000600000001 203.33999600000001 188.770004 226.050003 250.800003 268.26001000000002 266.14999399999999 249.05999800000001 248.39999399999999 206.929993 230.259995 240.009995 General Motors 40546 40575 40603 40634 40665 40695 40725 40756 40787 40819 40848 40878 40911 40940 40969 41001 41030 41061 41092 41122 41156 41183 41214 41246 41276 41306 41334 41365 41395 41428 41456 41487 41520 41548 41579 41610 41641 41673 41701 41730 41760 41792 41821 41852 41884 41913 41946 41974 42006 42037 42065 42095 42125 42156 42186 42219 42248 42278 42310 42339 32.593037000000002 29.949148000000001 27.716138999999998 28.662935000000001 28.412835999999999 27.117691000000001 24.723904000000001 21.463706999999999 18.024868000000001 23.089338000000001 19.016327 18.105257000000002 21.454775000000001 23.241184000000001 22.910696000000002 20.543704999999999 19.829142000000001 17.613993000000001 17.605060999999999 19.069918000000001 20.320404 22.776716 23.116133000000001 25.751086999999998 25.090116999999999 24.250503999999999 24.848951 27.546429 30.270702 29.752645000000001 32.039245999999999 30.440412999999999 32.128571000000001 33.003909999999998 34.593811000000002 36.505268000000001 32.226821999999999 32.334007 31.017056 31.071124999999999 31.161242000000001 32.984012999999997 30.730557999999998 31.621034999999999 29.276282999999999

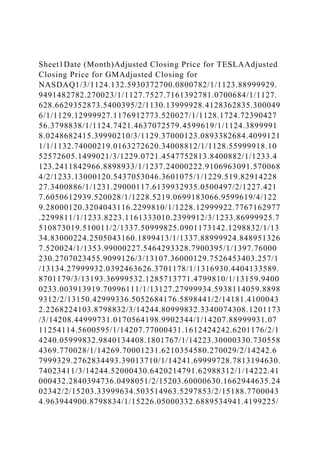

- 4. 28.781319 30.642021 32.284039 30.166294000000001 34.503509999999999 34.963940000000001 32.688952999999998 33.537410999999999 31.397797000000001 29.683304 27.733307 28.627621000000001 33.290813 34.520985000000003 32.774151000000003 Date Adjusted Closign Price According to the line chart above, we can see that Tesla outperformed General Motors in stock performance. Both companies had simlar low adjusted closing prices (below $50), from the beginning of 2011 to the end of 2012. In 2013, we can see that Tesla started to have increasing adjusted closing prices, whereas General Motors still had stock prices below $50. Tesla has shown to have a greater stock performance throughout all the years where the highest closing stock price was apprxomiately $269 in August of 2014. Despite having inconsistent, fluctuating closing stock prices, Tesla has shown significant,comparable performance from 2013 to 2015. Sheet1 (2)Date (Month)Adjusted Closing Price for TESLAAdjusted Closing Price for GMAdjusted Closing for NASDAQDate (Month)TeslaNASDAQ1/3/1124.132.5930372700.0800781/3/11 1001002/1/1123.88999929.9491482782.270022/1/1199.1286265 56103.04398164593/1/1127.7527.7161392781.0700683/1/11116 .157392890699.95687147584/1/1127.628.6629352873.5400394/ 1/1199.4594594595103.32497811055/2/1130.13999928.4128362 835.3000495/2/11109.202894927598.66923761356/1/1129.1299

- 7. 41061 41092 41122 41156 41183 41214 41246 41276 41306 41334 41365 41395 41428 41456 41487 41520 41548 41579 41610 41641 41673 41701 41730 41760 41792 41821 41852 41884 41913 41946 41974 42006 42037 42065 42095 42125 42156 42186 42219 42248 42278 42310 42339 100 99.128626556016584 116.15739289064012 99.459459459459467 109.20289492753624 96.648971355307609 96.704431744058766 87.8239261625843 98.585282942603087 120.41821321927893 111.47429651091943 87.232734439051058 101.78571784963997 114.92948056415548 111.46363962885364 88.963478036333086 89.043160608416528 106.06780000000001 87.631828455358644 104.01167031363967 102.66480014025245 96.072397675123042 120.22751938242158 100.14783855706682 110.74697108789404 92.855248885910356 108.78552059801778 142.49143157802669 181.07056562064955 109.81996604296305 125.07451355183949 125.85642035937161 114.42011538461539 82.711902640324325 79.57984082055971 118.1882418148039 120.59430462115357 134.94845521308739 85.147665006720842 99.73135139934783 99.942279570649291 115.54122028124907 93.018414088298044 120.77922453050751 89.981454283361316 99.596177670896836 101.16673853330664 90.957795011323483 91.542647515082109 99.872293716926521 92.834664951994966 119.74889983050485 110.94890496418175 106.96172519583264 99.213443703368227 93.578810300480413 99.735002005420398 83.305152173232344

- 8. 111.27434532895384 104.2343438772332 NASDAQ 40546 40575 40603 40634 40665 40695 40725 40756 40787 40819 40848 40878 40911 40940 40969 41001 41030 41061 41092 41122 41156 41183 41214 41246 41276 41306 41334 41365 41395 41428 41456 41487 41520 41548 41579 41610 41641 41673 41701 41730 41760 41792 41821 41852 41884 41913 41946 41974 42006 42037 42065 42095 42125 42156 42186 42219 42248 42278 42310 42339 100 103.04398164593991 99.956871475759939 103.3249781105479 98.669237613501025 97.821040879895946 99.382007814026878 93.581439079164824 93.639751673586844 111.13728661565541 97.613262277359667 99.420297156481169 108.01067861161411 105.43917920754279 104.20238632023948 98.537637510857152 92.810435690228132 103.80958631249032 100.15229624454011 104.33539966160869 101.60647741172126 95.53948197366357 101.10874907957228 100.30794953328621 104.06091957284156 100.57477121164568 103.39631734179993 101.87512298700467 103.81880117131655 98.4762359742900 63 106.55608953206495 98.993483874442589 105.05895358553441 103.93028683132503 103.57628328102717 102.87446098479695 98.259106981633494 104.97675955005531 97.466879287572098 97.989274318469413 103.1123633186466 103.90230693378857 99.128661840794962 104.81718715256324 98.103171153215115 103.05671425832837 103.47438294678481 98.840059032998568 97.871441915716943 107.0824711218193 98.737795385265329

- 9. 100.82719919622238 102.60269042158122 98.359779497824007 102.83563968345477 93.140584489385475 96.726697575017567 109.38473622904428 101.08671624041554 98.017883959111657 Date Adjusted Closing The values shown above are indexed to show better comparison between the two data sets. According to the graph above, we can see that Tesla has been performing erratically compared to NASDAQ throughout the years. It has shown the major growths and declines, whereas the NASDAQ remained relatively stagnant, with minor growth and declines in price. Tesla has shown to outperform and show significant growth compared to the stock index in the first quarter of 2013. However, Tesla has shown to underperform and show significant decline in its fourth quarter in 2014 in comparison to the index. BALTIMORE CITY COMMUNITY COLLEGE Principles of Accounting Fall 2016 Written Assignment Instructions Please read articles on any five unrelated Accountingtopics. What do I mean by unrelated topics? For instance, if you selected one article involving accounting education in colleges, then your second article cannot be on the same or similar topic. Your topics do not have to be restricted to accounting topics covered in the course.

- 10. ALL ARTICLES MUST BE RESEARCHED USING THE INTERNET. Your Accounting articles have to be from The CPA Journal, Journal of Accountancy or Accountant Today. The articles must be published in 2015 or 2016 and must contain at least 2 pages (equivalent to 8.5”x11”) of text. On each topic, you are required to write 1 page. Thus you will have written a total of 5 pages. Each topic is divided into two sections and has to be clearly identified, as follows: Section 1-Summary of the article in your own words (0.5 pages long) Section 2-Your comments, opinions and any other feedback you wish to provide on the topic (0.5 pages long). Format Use letter size paper (8.5"x11") Spacing of Work: 1.5 times Normal Print: 12 font size Margins: 1" on all sides Your work must be presented as follows: I Cover Sheet Show your name, course name and number, and semester. (3%) II The next page should list the articles presented with the title of the article, name and date of the source publication and links to them. (2%) III Next, you will present all of the 5 write ups. Each write up must start on a separate page. At the top of each write up, just show the name of the article only. 105 points (22 % per write up)

- 11. IV. Next, cite your articles using the APA format.(10 %) This assignment is designed to broaden your understanding of the accounting discipline as well as sharpen your Internet research, communication and critical thinking skills. There will be an automatic deduction of points if your work is not presented as specified. Due: November 13, 11.59pm EST Students who wish to submit the work early by 11.59pm EST, November 9 will be eligible for 10 points bonus. Late work will be penalized at the rate of 10 points for each 24 hour period that your work is late up to a maximum late penalty of 70 points. No credit will be given for late work submitted after 11.59pm EST, November 20 The next page is a sample work of student in a previous semester. Use it only as a general guide. Please consult my instructions above as I sometimes make changes in the assignment from one semester to the next. WRITTEN ASSIGNMENT ACCT 201 Student Name ARTICLES (2010, July). Accounting for Small Businesses: The Role of the IFRS. The CPA Journal Web Link: (2010, March). A Looming Crisis for Pensions. The CPA Journal Web link: (2010, December). When It Comes to Fraud, It's Better to Be Safe than Sorry. The CPA Journal Web Link: (2010, April). Attracting and Retaining Talent: The Importance of First Impressions. The CPA Journal

- 12. Web link: “Attracting and Retaining Talent: The Importance of First Impressions” Summary In this article, the authors discuss one of the most pressing issues facing accounting firms in a time of economic turmoil. They present the necessity of accounting firms to make highly impactful first impressions on candidates for available positions. As the market for skilled workers becomes more competitive, firms have to go above and beyond the normal routine to obtain and retain employees. If they do not take the necessary steps, they may not stay in business. While there are more workers available for positions due to the recent recession, many do not possess the required skills for specialized jobs, making one of the top 10 most difficult positions to fill is that of the accountant (Yamanmura, Birk, & Cossitt, 2010). This fact makes it imperative for an accounting firm to find ways to attract candidates and once they have them, give them a reason to stay. The authors suggest that the first impression a firm makes is the one of the most important factors in a candidate’s decision to begin or continue working for the company. They then outline how these first impressions impact the worker. The more positive the initial impression is, the more likely the employee is to be excited about working for the company and the more likely they are to stay.

- 13. The authors outline a plan for accounting firms to use to manage first impressions. The first step in the plan is to train recruiters who can appeal to the desires of potential recruits. The next step is to set a clear vision and expectation for the new employee, by preparing assignments, scheduling training, and setting goals. Finally, the authors suggest that for a firm to retain an employee, they must offer a fair balance between work and life. It is stated that Generation Y, people with birthdays from the 1970s to 1990s make up the majority of candidates for accounting positions. People in Gen Y want to be challenged, want to grow and learn, and are not afraid of advancement. Employees from this generation want to have direction and purpose. If a firm can provide these things, they are likely to employ workers who feel a sense of ownership in the company. Their workers will not just show up until something better presents itself, they will care about results and work diligently for the company’s success. Reaction The article captured my attention because two years ago, I found myself in search of employment due to changes my previous employer made to streamline operations and cut costs. It opened my eyes to the fact that there is a lot of opportunity for employment in the field of accounting. I have worked in several different industries and in most of those industries, I had to compete with other qualified applicants for the position I was interested in. It would seem that the demand for highly skilled accountants is on the rise and the supply is very limited. Because of this, accounting firms need to compete for employees. The first step to employing talent is making a great first impression.

- 14. I understand how a first impression can affect the attitude of an employee. I experienced this with a previous employer. I cared about my position and worked hard towards my personal success. I love the challenges that my job presented to me and did what was necessary to overcome them. However, the recruiting process was prolonged and disorganized. My first impression of employment with the company was not a good one. As a result, I kept my eyes open for other opportunities. As a “Gen Y” member, I agree with the authors’ suggestion that working with positive people in a friendly environment is important. I want to be challenged and certainly enjoy learning new skills. If I feel that my current path does not provide me the opportunity to grow and advance, I will indeed look for a change. Having experienced firsthand how a first impression can impact an employee’s attitude towards the company he works for, I definitely agree that accounting firms must put a plan into place to make sure that first impressions it makes, are lasting and positive. In doing so, accounting firms can be sure to attract the best talent and have employees who feel empowered and motivated to grow and improve the company. “When It Comes to Fraud, It’s Better to Be Safe than Sorry” Summary In this article, the author presents three scenarios involving fraud that he encountered during his career as an accountant. In each of the three stories, the author demonstrates the necessity for leaders to make ethical decisions when preparing financial statements and reporting performance.

- 15. In the first scenario, a bookkeeper at one of CS Company’s offices altered the office’s monthly statements to improve results. The bookkeeper changed the accounts receivable aging to hide the fact that the office was not efficient at collecting the money it was owed. The monthly reports were analyzed and compared to the statements of other offices. The misstatements were discovered and fixed and an investigation ensued. As a result of the investigation, it was determined that the company didn’t lose any money due to the alterations, collections on accounts payable were made, and the bookkeeper was fired. The second scenario involved a company that had six US and three foreign manufacturing facilities. The product had become obsolete and the sales of the product were declining. The company had positive profits, but mostly because of one of its foreign subsidiaries. The subsidiary was audited by a local auditing team as well as the corporation’s auditors. It was discovered that there were many errors in the subsidiaries financial statements, which drastically inflated the profits. The CEO and the controller of the subsidiary were aware of the misstatements and did not report them, so they were both fired. It turns out, the director of the subsidiary was inflating its sales and its accounts receivable. The company’s poor performance and its lack of managerial ethics and attention ultimately caused it to go out of business. The final scenario involves an automobile parts manufacturer. When the company’s CFO discovered some inconsistencies in its subsidiaries numbers, he had a corporate controller investigate the irregularities by herself. The investigation progressed slowly. When the controller made her reports to the CFO, he simply told her to continue her investigation and did not report any of the findings to the SEC. Ultimately, the CFO

- 16. was replaced due to poor performance. The new CFO reported the findings to the auditing board and full investigation was performed. These scenarios show that discovering errors and deviations to financial reports is only the one step. Once these things are discovered, they must be reported immediately to auditors, so that any problems resulting from the errors can be swiftly resolved. Many errors can be prevented with adequate attention from corporate management and effective controls. The situation in the second scenario could have been prevented if managers had set clear expectations, communicated properly and implemented controls to keep the manager at the subsidiary from making adjustments to the financial statements. Reaction I found this article interesting and chose it because the company I work for has controls in place to detect non-compliance with government and company guidelines. All of our locations are visited at least twice a year by a control review team. The team will come prepared with information regarding accounts opened, transactions that we have processed, and procedures we have followed. The auditors spend a day reviewing our procedures to ensure our compliance with laws. At the end of the review we get a score based on their findings. This can be very stressful but if we are operationally sound and acting with integrity, there really is nothing to worry about. As stated in the article, integrity should be the primary focus.

- 17. You have to question peoples’ motives for making unethical decisions, such as altering performance reporting. What was the benefit to the bookkeeper to overstate accounts receivable collection? I think the bookkeeper made these changes to cover up the lack of effort to actually collect on the accounts. Could the errors in the second scenario have been prevented? If the directors of corporate management had communicated properly with its subsidiary, and not neglected it, I think that this situation could have been easily avoided. With clear direction from corporate management, the director of the subsidiary would not have made inaccurate alterations to the financial statements and the situation would have been avoided. I can understand the pressure that some of these subsidiaries must receive from corporate officers. I work in a partially commission based, goal oriented sales environment. Our “numbers” are under constant scrutiny. We have to report frequently to middle management on what we are doing to achieve our goals. The temptation frequently arises to overstate our performance. There is rarely any benefit to doing so. Overstating my performance would only tarnish my reputation and lead to more problems in the future. “Accounting for Small Businesses: The Role of the IFRS” Summary United States based CPAs have had two methods or sets of standards for reporting financial information; the US Generally Accepted Account Principals, and Other Comprehensive Basis of Accounting. This has presented a problem for accountants, as many of the reporting requirements of GAAP are very demanding, and don’t necessarily apply to all small businesses. Because of this, accountants have generally agreed that there

- 18. needs to be a set of accounting standards developed specifically for small businesses. The International Accounting Standards Board released the International Financial Reporting Standards for Small to Medium Sized Entities (IFRS for SMEs) in May of 2009. In this article, the authors discuss the results of several surveys conducted of CPAs regarding their willingness or likelihood to adopt them. The authors received 243 survey responses from CPAs. The survey posed questions to CPAs about their knowledge of IFRS and IFRS for SMEs, as well as their willingness to adopt IFRS. More than half of the respondents believed that there should be different reporting requirements for private and public companies. However, most of the CPAs who responded to the survey had little detailed knowledge about IFRS and IFRS for SMEs. As a result, it was determined that most CPAs would continue to use their current accounting basis even if the US adopted IFRS. They also reported that their clients’ knowledge of IFRS would be a very significant barrier in their adoption of IFRS. The survey also asked the CPAs what type of accounting they use. The results show that only small business used cash and tax basis account and only large business used IFRS. Next, the author discusses two conclusions from the survey. One conclusion is that different types of businesses have different needs regarding accounting standards. The other conclusion is that CPAs and their clients need more detail before adopting IFRS and IFRS for SMEs. Reaction

- 19. After reading this article, I agree that different types of business need different accounting standards. I work with a lot of small business owners, with less than 10 employees. I can see the importance of a simple set of accounting standards a small business that does less than $10 million in revenue per year, or has a very limited number of transaction types. On several occasions, business owners have come to me to establish a line of credit. One requirement is that the customer must be able to provide two years of financial statements. I feel that if there are specific accounting standards for SMEs, than it may be easier for these customers to provide the necessary documents, obtain their lines of credit and use that to enhance and grow their business. I do find it interesting that CPAs are reluctant to change the basis of accounting they use for their clients. I think that a simpler set of standards for financial reporting would make their job easier. It may take them some time to learn all of the details and requirements of IFRS. However, I think it will ultimately help their clients, especially if they intend to grown beyond US borders. “A Looming Crisis for Pensions” Summary We learn that underfunding of pension plans could have drastic negative repercussions. Financial accountants have a very daunting task in managing pension plans. They have to determine how much money needs to be contributed to a pension plan by a company, what the value of the pension plan currently is and what it may be worth in the future. The authors present several questions that accountants face

- 20. when determining pension plan funding. They are: How many more years will an employee work? How will an employee’s compensation over time affect amounts promised in retirement? For how many years after retirement will an employee live and collect compensation or other post-retirement benefits? What investment returns will be earned on funds designated to meet future retirement obligations? (Easterday & Eaton, 2010). The two types of pension plans are defined contribution (DC), which includes 401k and 403b retirement plans, and defined benefit plan (DB), which is a type of deferred compensation. In a DC type plan, employees make a contribution to the plan, the employer may match it, and the employee is responsible for the performance of the plan. Generally in DB plans, an employee is promised a certain percentage of their income to be paid after retirement. In the DB plan, employers set money aside and are responsible for investing these funds. The longer an employee stays with a company that offers a DB plan, the great the obligation is for the employer. If the assets in the plan are less than the total obligation, the plan is considered underfunded. There are three major reasons a pension plan has funding problems. If the plans assets are invested and those investments perform poorly, the plans funding can be negatively affected. Delays in paying cash contributions to the plan by the employer will also result in under funding. Accountants and decision makers may have overestimated interest rates. This may also cause underfunding in pension plans. The author provides us with an example of a drastic underfunding problem in Cincinnati, Ohio. The city of Cincinnati has only made partial contributions to its pension

- 21. plans to free up cash for other needs. As of December of 2008, the city reported that its pension plans were underfunded by nearly $913 million dollars. This could have very negative tax implications for city residents, as they may need to bear the burden of this deficit. The Pension Benefit Guaranty Corporation currently protects corporations and employees if the company fails and the pension plan is underfunded. Unfortunately, the PBGC has protected more companies than it can handle. It reported a $33.5 billion deficit in the first half 2009. While many companies have moved away from DB plans, those that do have a responsibility to its employees to manage and fun them. If not, they’re putting the financial security of its people in jeopardy. Reaction I do not understand why an employer would put itself into a position where it did not provide adequate funding to its pension plan. I know that idle cash does not benefit the company, but by not contributing the necessary funds to the pension plan, the company would be putting the economic security of its employees at risk. I chose this article because my family’s financial security has been on my mind a lot recently. Having just been married, retirement discussions are a frequent occurrence in my home. Who is going to retire first? What do we need to retire? My wife and I both have DC plans with our employers. Bank of America, my employer also offers a 4% per year Defined Benefit plan. With recent developments in the banking industry, it worries me that BOA may not make adequate contributions to my pension, in order to utilize those funds for other purposes. While I am

- 22. confident that Bank of America will not go out of business before I retire, the prospect of being asked to accept a reduced benefit if my pension plan is inadequately funded, does not appeal to me. I can see that financial accountants have to carefully calculate how much money and when a firm needs to contribute to its DB plan. This must be done in order to ensure the company doesn’t have to play catch up. By making adequate contributions, the company shows that it has the employees’ best interest in mind. The last paragraph of the article states that thoughtful reform is required. I located a plan that I find very interesting. Maryland’s unfunded liability for pension plans as of January, 21, 2011 was $19 billion dollars. By adjusting retirement age of state workers, changing benefit calculation from highest three years of salary to highest five years, and requiring a ten year vesting period as opposed to five, the Governor of Maryland hopes to reduce this unfunded pension liability by $7 million dollars (O'Malley, 2011). Let’s hope it works. Works Cited Christie, N., Brozovsky, J., & Hicks, S. (2010, July). Accounting for Small Businesses: The Role of the IFRS. The CPA Journal, pp. 40-43. Easterday, K., & Eaton, T. V. (2010, March). A Looming Crisis for Pensions. The CPA Journal, pp. 56-58. O'Malley, M. (2011, January 21). Reforming Maryland's Pension System: A Path to Sustainability. Retrieved March 6, 2011, from Maryland.gov: http://www.governor.maryland.gov/documents/RetirementRefor m.pdf

- 23. Weinstein, E. A. (2010, December). When It Comes to Fraud, It's Better to Be Safe than Sorry. The CPA Journal, pp. 6, 8-9. Yamanmura, J., Birk, C. A., & Cossitt, B. J. (2010, April). Attracting and Retaining Talent: The Importance of First Impressions. The CPA Journal, pp. 58-60. Part 1Date (Month)Adjusted Closing Price for TESLAAdjusted Closing Price for GMAdjusted Closing for NASDAQ12/1/15240.00999532.7741515007.41015611/2/15230. 25999534.5209855108.66992210/1/15206.92999333.290813505 3.759/1/15248.39999428.6276214620.1601568/3/15249.059998 27.7333074776.5097667/1/15266.14999429.6833045128.279785 6/1/15268.2600131.3977974986.8701175/1/15250.80000333.53 74115070.0297854/1/15226.05000332.6889534941.4199223/2/1 5188.77000434.963944900.8798832/2/15203.33999634.5035149 63.5297851/2/15203.60000630.1662944635.24023412/1/14222. 41000432.2840394736.04980511/3/14244.52000430.642021479 1.62988310/1/14241.69999728.7813194630.7402349/2/14242.6 7999329.2762834493.3901378/1/14269.70001231.6210354580.2 70027/1/14223.30000330.7305584369.770026/2/14240.0599983 2.9840134408.1801765/1/14207.77000431.1612424242.6201174 /1/14207.88999931.0711254114.5600593/3/14208.44999731.01 70564198.9902342/3/14244.80999832.3340074308.1201171/2/1 4181.41000432.2268224103.87988312/2/13150.42999336.50526 84176.58984411/1/13127.27999934.5938114059.88989310/1/13 159.94000233.003913919.7099619/3/13193.36999532.12857137 71.479988/1/1316930.4404133589.8701177/1/13134.27999932. 0392463626.3701176/3/13107.36000129.7526453403.255/1/139 7.76000230.2707023455.9099124/1/1353.99000227.5464293328 .7900393/1/1337.88999924.8489513267.520022/1/1334.830002 24.2505043160.1899411/2/1337.50999825.0901173142.1298831 2/3/1233.86999925.7510873019.5100111/1/1233.8223.1161333 010.2399910/1/1228.12999922.7767162977.229989/4/1229.280 00120.3204043116.229988/1/1228.5219.0699183066.9599617/2

- 24. /1227.4217.6050612939.520026/1/1231.29000117.6139932935. 0500495/1/1229.519.8291422827.3400884/2/1233.13000120.54 37053046.3601073/1/1237.24000222.9106963091.5700682/1/12 33.4123.2411842966.8898931/3/1229.0721.4547752813.840088 12/1/1128.55999918.1052572605.14990211/1/1132.74000219.0 163272620.34008810/3/1129.37000123.0893382684.4099129/1/ 1124.38999918.0248682415.3999028/1/1124.7421.4637072579. 4599617/1/1128.1724.7239042756.3798836/1/1129.12999927.1 176912773.520025/2/1130.13999928.4128362835.3000494/1/11 27.628.6629352873.5400393/1/1127.7527.7161392781.0700682 /1/1123.88999929.9491482782.270021/3/1124.132.5930372700. 080078 Part 21).2). TESLA vs. GM stock values comparison Adjusted Closing Price for TESLA 42339 42310 42278 42248 42219 42186 42156 42125 42095 42065 42037 42006 41974 41946 41913 41884 41852 41821 41792 41760 41730 41701 41673 41641 41610 41579 41548 41520 41487 41456 41428 41395 41365 41334 41306 41276 41246 41214 41183 41156 41122 41092 41061 41030 41001 40969 40940 40911 40878 40848 40819 40787 40756 40725 240.009995 230.259995 206.929993 248.39999399999999 249.05999800000001 266.14999399999999 268.26001000000002 250.800003 226.050003 188.770004 203.33999600000001 203.60000600000001 222.41000399999999 244.520004 241.699997 242.679993 269.70001200000002 223.300003 240.05999800000001 207.770004 207.88999899999999 208.449997 244.80999800000001 181.41000399999999 150.429993 127.279999 159.94000199999999

- 25. 193.36999499999999 169 134.279999 107.360001 97.760002 53.990001999999997 37.889999000000003 34.830002 37.509998000000003 33.869999 33.82 28.129999000000002 29.280000999999999 28.52 27.42 31.290001 29.5 33.130001 37.240001999999997 33.409999999999997 29.07 28.559999000000001 32.740001999999997 29.370000999999998 24.389999 24.74 28.17 29.129999000000002 30.139999 27.6 27.75 23.889999 24.1 Adjusted Closing Price for GM 42339 42310 42278 42248 42219 42186 42156 42125 42095 42065 42037 42006 41974 41946 41913 41884 41852 41821 41792 41760 41730 41701 41673 41641 41610 41579 41548 41520 41487 41456 41428 41395 41365 41334 41306 41276 41246 41214 41183 41156 41122 41092 41061 41030 41001 40969 40940 40911 40878 40848 40819 40787 40756 40725 32.774151000000003 34.520985000000003 33.290813 28.627621000000001 27.733307 29.683304 31.397797000000001 33.537410999999999 32.688952999999998 34.963940000000001 34.503509999999999 30.166294000000001 32.284039 30.642021 28.781319 29.276282999999999 31.621034999999999 30.730557999999998 32.984012999999997 31.161242000000001 31.071124999999999 31.017056 32.334007 32.226821999999999 36.505268000000001 34.593811000000002 33.003909999999998 32.128571000000001 30.440412999999999 32.039245999999999 29.752645000000001 30.270702 27.546429 24.848951 24.250503999999999 25.090116999999999

- 26. 25.751086999999998 23.116133000000001 22.776716 20.320404 19.0699 18000000001 17.605060999999999 17.613993000000001 19.829142000000001 20.543704999999999 22.910696000000002 23.241184000000001 21.454775000000001 18.105257000000002 19.016327 23.089338000000001 18.024868000000001 21.463706999999999 24.723904000000001 27.117691000000001 28.412835999999999 28.662935000000001 27.716138999999998 29.949148000000001 32.593037000000002 date price Tesla vs. NASDAQ stock values comparison Adjusted Closing for NASDAQ 42339 42310 42278 42248 42219 42186 42156 42125 42095 42065 42037 42006 41974 41946 41913 41884 41852 41821 41792 41760 41730 41701 41673 41641 41610 41579 41548 41520 41487 41456 41428 41395 41365 41334 41306 41276 41246 41214 41183 41156 41122 41092 41061 41030 41001 40969 40940 40911 40878 40848 40819 40787 40756 40725 40695 40665 40634 40603 40575 40546 5007.4101559999999 5108.669922 5053.75 4620.1601559999999 4776.5097660000001 5128.2797849999997 4986.8701170000004 5070.0297849999997

- 27. 4941.419922 4900.8798829999996 4963.5297849999997 4635.2402339999999 4736.0498049999997 4791.6298829999996 4630.7402339999999 4493.3901370000003 4580.2700199999999 4369.7700199999999 4408.1801759999998 4242.6201170000004 4114.5600590000004 4198.9902339999999 4308.1201170000004 4103.8798 829999996 4176.5898440000001 4059.889893 3919.709961 3771.4799800000001 3589.8701169999999 3626.3701169999999 3403.25 3455.9099120000001 3328.790039 3267.5200199999999 3160.1899410000001 3142.1298830000001 3019.51001 3010.23999 2977.2299800000001 3116.2299800000001 3066.959961 2939.5200199999999 2935.0500489999999 2827.3400879999999 3046.360107 3091.570068 2966.889893 2813.8400879999999 2605.1499020000001 2620.3400879999999 2684.4099120000001 2415.3999020000001 2579.459961 2756.3798830000001 2773.5200199999999 2835.3000489999999 2873.540039 2781.070068 2782.2700199999999 2700.080078 Adjusted Closing Price for TESLA 42339 42310 42278 42248 42219 42186 42156 42125 42095 42065 42037 42006 41974 41946 41913 41884 41852 41821 41792 41760 41730 41701 41673 41641 41610 41579 41548 41520 41487 41456 41428 41395 41365 41334 41306 41276 41246 41214 41183 41156 41122 41092 41061 41030 41001 40969 40940 40911 40878 40848 40819 40787 40756 40725 40695 40665 40634 40603 40575 40546 240.009995 230.259995 206.929993 248.39999399999999 249.05999800000001

- 28. 266.14999399999999 268.26001000000002 250.800003 226.050003 188.770004 203.33999600000001 203.60000600000001 222.41000399999999 244.520004 241.699997 242.679993 269.70001200000002 223.300003 240.05999800000001 207.770004 207.88999899999999 208.449997 244.80999800000001 181.41000399999999 150.429993 127 .279999 159.94000199999999 193.36999499999999 169 134.279999 107.360001 97.760002 53.990001999999997 37.889999000000003 34.830002 37.509998000000003 33.869999 33.82 28.129999000000002 29.280000999999999 28.52 27.42 31.290001 29.5 33.130001 37.240001999999997 33.409999999999997 29.07 28.559999000000001 32.740001999999997 29.370000999999998 24.389999 24.74 28.17 29.129999000000002 30.139999 27.6 27.75 23.889999 24.1 date price When looking at a visual comparison between Tesla Motors and General Motors regarding their stock values, the very first thing that one would notice is that Tesla's stocks are very inconsistent compared to GM's stock values. The graph also shows that although Tesla has higher adjusted closing prices overall, the company does better over time, and although it has moments where the stock value price goes down, Tesla does better than GM.

- 29. By looking at the chart above, it is clear that NASDAQ is doing dramatically better than Tesla, and although they show more inconsistency (with the price going up and down throughout the time intervals), the value of their stocks have started out and stayed consistently higher than Tesla's. It is not a very reasonable comparison, since NASDAQ is the second largest exchange in the world, while Tesla is a relatively new start-up company. INSY 2299 – Information Systems – Fall 2016 Information Systems Deliverable Due Date: Tuesday, November 22, 11:00 PM ET The policy on late assignments is stated in the syllabus. This is a GROUP project that you should prepare and submit jointly with your CC group. Submission Requirements (one person uploads both components to Blackboard for your group): · Part One: The Excel Workbook · Part Two: The Word Document Note: If you divide the various tasks among team members— there are some natural ways to do so—make sure that the final Document and Workbook you submit are complete, consistent, and coherent. Everyone on your team should review both components of the submission. The grading criteria are found at the conclusion of this document.

- 30. PART ONE: DATA ANALYSIS AND CHARTING Submit a Microsoft Excel Workbook containing the following 4 sheets: · "Documentation": Contains the names of all group members, your section (e.g., LWA), and your CC company. · "Stock Prices": produced in Step 1 below · "Stock Plots": produced in Step 2 below · "Scatter Plots”: produced in Step 3 below Be sure to name your sheets as stated above. While working on your analysis you may create more worksheets than these. Delete all the unnecessary worksheets and leave only the final results listed here. For instance, to complete Step 1, you will be downloading at least three worksheets along the way. Do NOT include all the worksheets. Include only one final worksheet that integrates the information required. Hint: In Part One you will be creating charts and interpreting them. It is easy to misinterpret charts. For each chart, you should discuss your analysis and conclusions as a group. Step 1: ETL (Extracting/Transforming/Loading) Data Step 1 involves two simple examples of ETL which is the necessary first step for Business Analytics. You will extract data from third-party sources, transform the data in a desired form, and then load the data into your software application. Specifically, you will extract data about your CC company from Yahoo! Finance (http://finance.yahoo.com) manipulate the data, and then load them into Microsoft Excel. First, enter your CC Company's stock symbol at Yahoo! Finance

- 31. in the empty box at the top left. Next, retrieve historical prices by clicking the “Historical Prices” link on the left navigation bar. You want to retrieve data from January 1, 2011 to December 31, 2015 in monthly intervals. This means you will have 60 stock prices for your company. For this analysis, you only need the “Adjusted Closing Price," but you can download more if that is easiest. Find a way to extract these data and load them into Excel. (Hint: For most companies, you can either find a link to download the data to a spreadsheet or you can copy and paste.) Next, identify one of your company’s major competitors. You can use a competitor you have already identified as part of your work on the Consulting Challenge in other courses or you can click on “Competitors” on the left navigation bar in Yahoo! Finance. Download historical prices for this competitor by repeating the steps above. (Note: Some of your competitors may not have gone public from 2011. Be sure to choose only those that were public companies since 2011.) Choose to compare your company’s performance with either the Dow Jones Industrial Average or the NASDAQ Composite Index. Choose whichever index would be a more appropriate comparison for your company. For the index you choose, extract and load into your spreadsheet the "adjusted close" for the same 60 months for that index. This should not be difficult but you may need to think a little bit or hunt around the site to find it. Note: We are using the adjusted close because some of your CC companies may have had stock splits during or after the time period we are focusing on. Now copy and paste the data you have downloaded into a single spreadsheet with 61 rows (60 monthly data points plus a title row) and the following 4 columns:

- 32. Date (Month) Adjusted Closing Price for your company Adjust Adjusted Closing Price for your competitor Adjusted Closing for the DJIA or NASDAQ. Be sure to match correctly the dates across the three companies and the two indexes. Step 2: Charting and Analyzing the Stock Price Data (1) Generate a Line Chart in Excel comparing your company with your competitor in terms of their stock values (that is, their adjusted closing stock prices). Format and label the chart appropriately for readability (but do not over-format). In particular, you may find that the default formatting for 60 data points is not ideal and that you need to change the intervals. Place a large text box beneath the chart discussing the comparison of your company’s stock performance with that of its competitor. Your text should contain no more than 200 words. It may include more than one paragraph. (2) Generate a Line Chart comparing your CC company's stock with the index you chose (DJIA or NASDAQ). Note: Think about why this might be tricky and devise a way to overcome the problem. You may want to explore some features of Excel Charting to do this. Place a large text box beneath the chart discussing the comparison of your company’s stock performance with the index you chose (DJIA or NASDAQ). Your text should contain no more than 200 words. It may include more than one paragraph.

- 33. Step 3: Checking for Correlations Using Scatter Plots Use the 60 months of data from Step 1 to create a Scatter Chart (one with markers but NO LINES is likely to be the most effective type) to examine the relationship between your company’s stock price and its competitor’s stock price. Create an empty Scatter Plot and then in the "Select Data" dialog box, on the left side, you will need to add the appropriate data. For each Scatter Chart, your competitor’s stock price will be the "Series Y Values" (on the vertical axis) and your company’s stock price will be the "Series X Values" (on the horizontal axis). You can leave the "Series Name" box blank. Be sure that the chart has a meaningful title and that the horizontal and vertical axes are well labeled. If you do this well, you will not need a legend on this chart. A scatter chart shows the relationship between two variables. In this case, those variables are (a) your competitor’s stock price and (b) your company’s stock price. A steep upward slope means that a higher value of the variable on the X axis corresponds to a higher value of the variable on the Y axis during the period you analyzed. A steep downward slope means that a higher value of the variable on the X axis is associated with a lower value of the variable on the Y axis. A relatively flat line, or widely scattered points without a pattern, would suggest that there is not much of a relationship between the two variables. Place a large text box beneath the Scatter Plot discussing what your plot tells you about the relationship between the two variables. Your text should contain no more than 200 words. It may include more than one paragraph. PART TWO: MONITORING AND CONTROLLING YOUR

- 34. CONSULTING CHALLENGE RECOMMENDED RESPONSE Submit a Word Document answering the following questions. A critical component of your Recommended Response to the Consulting Challenge is defining how you will monitor and control the success of your proposal as the company follows the recommended course of action over the next several years. (1) What will be the key performance measures that will indicate if your Recommended Response is on course? What are the target values for those measures? (2) What role will Information Systems/Business Analytics play in monitoring performance and enabling adjustments to the company’s behavior as needed? More specifically, a) What data will the company need to draw upon to analyze the performance measures? What will be the source(s) of these data? Be sure to indicate whether these sources are internal to the company or external. (Hint: Many business issues draw on, and integrate, multiple sources of data.) b) Which of the Business Analytics tools and techniques that we discussed in class or that are covered in Chapter 15 of Gallaugher will you use for studying the proposal’s success and the performance measures? Explain why the tools and techniques you plan to use are appropriate. Here is a quick overview of the tools and techniques to consider: · Simulation Modeling · OLAP and Pivot Tables—that is, manipulating multidimensional data cubes. · Performance Dashboards · Data Mining—including mining of numeric data, text (for

- 35. instance, blogs and postings on social network sites), and logs of web traffic (web mining). · Predictive Analytics—using statistical techniques to make forecasts about future behavior. (3) Now, choose one of the Business Analytics tools or techniques you have identified and consider what applications software you will use for the analysis by doing the following (which will require both some research and applying concepts from the course): a) Identify a software package (other than Microsoft Excel) that you can acquire that will provide the functionality you need. b) Why did you choose this package? That is, evaluate this package briefly with respect to its advantages and disadvantages. GRADING CRITERIA: Part Description Points Assigned ONE Correct Data for Stock Prices 10 Stock Charts Correct and Labeled Well 10 Analyses of Stocks Chart (including choice of index) 10 Scatter Plot Correct and Labeled Well

- 36. 10 Analysis of Scatter Plot 10 TWO Discussion of Key Performance Measures and Targets 10 Discussion of Data Needs and Data Sources 15 Discussion of Business Analytics Tools and Techniques 20 Discussion of Software Package Selected 5 TOTAL 100 4