1.1Yearcash flowpresent value of cash inflow = cash flow(1+r).pdf

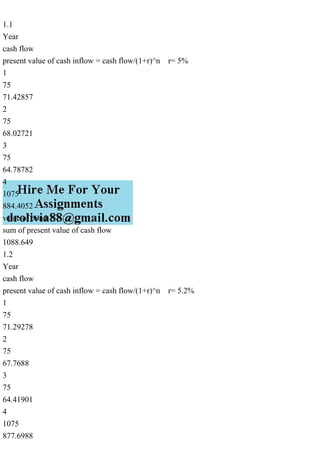

1.1 Year cash flow present value of cash inflow = cash flow/(1+r)^n r= 5% 1 75 71.42857 2 75 68.02721 3 75 64.78782 4 1075 884.4052 value of bond sum of present value of cash flow 1088.649 1.2 Year cash flow present value of cash inflow = cash flow/(1+r)^n r= 5.2% 1 75 71.29278 2 75 67.7688 3 75 64.41901 4 1075 877.6988 value of bond sum of present value of cash flow 1081.179 1.3 % change in bond price if YTM increases by .2% (1081.18-1088.65)/1088.65 -0.69% 1.4 Duration is a measure of a bond\'s sensitivity to interest rate changes. The higher the bond\'s duration, the greater its sensitivity to the change (also know as volatility) and vice versa. 1.4 Year cash flow Year*cash flow present value of Year*cash inflow = cash flow/(1+r)^n r= 5% 1 75 75 71.42857 2 75 150 136.0544 3 75 225 194.3635 4 1075 4300 3537.621 total 3939.467 Macculay duration in years total/face value of bond 3939.467/1000 3.939467 1.4 modified duration macculay duration/(1+YTM) 3.94/1.05 3.752381 1.5 change in price if YTM increases by .2% modified duration*change in YTM 3.75*.2% 0.75% 1.1 Year cash flow present value of cash inflow = cash flow/(1+r)^n r= 5% 1 75 71.42857 2 75 68.02721 3 75 64.78782 4 1075 884.4052 value of bond sum of present value of cash flow 1088.649 1.2 Year cash flow present value of cash inflow = cash flow/(1+r)^n r= 5.2% 1 75 71.29278 2 75 67.7688 3 75 64.41901 4 1075 877.6988 value of bond sum of present value of cash flow 1081.179 1.3 % change in bond price if YTM increases by .2% (1081.18-1088.65)/1088.65 -0.69% 1.4 Duration is a measure of a bond\'s sensitivity to interest rate changes. The higher the bond\'s duration, the greater its sensitivity to the change (also know as volatility) and vice versa. 1.4 Year cash flow Year*cash flow present value of Year*cash inflow = cash flow/(1+r)^n r= 5% 1 75 75 71.42857 2 75 150 136.0544 3 75 225 194.3635 4 1075 4300 3537.621 total 3939.467 Macculay duration in years total/face value of bond 3939.467/1000 3.939467 1.4 modified duration macculay duration/(1+YTM) 3.94/1.05 3.752381 1.5 change in price if YTM increases by .2% modified duration*change in YTM 3.75*.2% 0.75% Solution 1.1 Year cash flow present value of cash inflow = cash flow/(1+r)^n r= 5% 1 75 71.42857 2 75 68.02721 3 75 64.78782 4 1075 884.4052 value of bond sum of present value of cash flow 1088.649 1.2 Year cash flow present value of cash inflow = cash flow/(1+r)^n r= 5.2% 1 75 71.29278 2 75 67.7688 3 75 64.41901 4 1075 877.6988 value of bond sum of present value of cash flow 1081.179 1.3 % change in bond price if YTM increases by .2% (1081.18-1088.65)/1088.65 -0.69% 1.4 Duration is a measure of a bond\'s sensitivity to interest rate changes. The higher the bond\'s duration, the greater its sensitivity to the change (also know as volatility) and vice versa. 1.4 Year cash flow Year*cash flow present value of Year*cash inflow = cash flow/(1+r)^n r= 5% 1 75 75 71.42857 2 75 150 136.0544 3 75 225 194.3635 4 1075 4300 3537.621 total 3939.467 M.

Recommended

Recommended

More Related Content

More from aquacareser

More from aquacareser (20)

Recently uploaded

Recently uploaded (20)

1.1Yearcash flowpresent value of cash inflow = cash flow(1+r).pdf

- 1. 1.1 Year cash flow present value of cash inflow = cash flow/(1+r)^n r= 5% 1 75 71.42857 2 75 68.02721 3 75 64.78782 4 1075 884.4052 value of bond sum of present value of cash flow 1088.649 1.2 Year cash flow present value of cash inflow = cash flow/(1+r)^n r= 5.2% 1 75 71.29278 2 75 67.7688 3 75 64.41901 4 1075 877.6988

- 2. value of bond sum of present value of cash flow 1081.179 1.3 % change in bond price if YTM increases by .2% (1081.18-1088.65)/1088.65 -0.69% 1.4 Duration is a measure of a bond's sensitivity to interest rate changes. The higher the bond's duration, the greater its sensitivity to the change (also know as volatility) and vice versa. 1.4 Year cash flow Year*cash flow present value of Year*cash inflow = cash flow/(1+r)^n r= 5% 1 75 75 71.42857 2 75 150 136.0544 3 75 225 194.3635 4 1075 4300 3537.621 total 3939.467 Macculay duration in years total/face value of bond 3939.467/1000

- 3. 3.939467 1.4 modified duration macculay duration/(1+YTM) 3.94/1.05 3.752381 1.5 change in price if YTM increases by .2% modified duration*change in YTM 3.75*.2% 0.75% 1.1 Year cash flow present value of cash inflow = cash flow/(1+r)^n r= 5% 1 75 71.42857 2 75 68.02721 3 75 64.78782 4 1075 884.4052 value of bond sum of present value of cash flow 1088.649 1.2 Year cash flow present value of cash inflow = cash flow/(1+r)^n r= 5.2% 1 75

- 4. 71.29278 2 75 67.7688 3 75 64.41901 4 1075 877.6988 value of bond sum of present value of cash flow 1081.179 1.3 % change in bond price if YTM increases by .2% (1081.18-1088.65)/1088.65 -0.69% 1.4 Duration is a measure of a bond's sensitivity to interest rate changes. The higher the bond's duration, the greater its sensitivity to the change (also know as volatility) and vice versa. 1.4 Year cash flow Year*cash flow present value of Year*cash inflow = cash flow/(1+r)^n r= 5% 1 75 75 71.42857 2 75 150 136.0544 3 75 225

- 5. 194.3635 4 1075 4300 3537.621 total 3939.467 Macculay duration in years total/face value of bond 3939.467/1000 3.939467 1.4 modified duration macculay duration/(1+YTM) 3.94/1.05 3.752381 1.5 change in price if YTM increases by .2% modified duration*change in YTM 3.75*.2% 0.75% Solution 1.1 Year cash flow present value of cash inflow = cash flow/(1+r)^n r= 5% 1 75 71.42857 2 75 68.02721 3 75

- 6. 64.78782 4 1075 884.4052 value of bond sum of present value of cash flow 1088.649 1.2 Year cash flow present value of cash inflow = cash flow/(1+r)^n r= 5.2% 1 75 71.29278 2 75 67.7688 3 75 64.41901 4 1075 877.6988 value of bond sum of present value of cash flow 1081.179 1.3 % change in bond price if YTM increases by .2% (1081.18-1088.65)/1088.65 -0.69% 1.4 Duration is a measure of a bond's sensitivity to interest rate changes. The higher the bond's duration, the greater its sensitivity to the change (also know as volatility) and vice versa. 1.4 Year cash flow

- 7. Year*cash flow present value of Year*cash inflow = cash flow/(1+r)^n r= 5% 1 75 75 71.42857 2 75 150 136.0544 3 75 225 194.3635 4 1075 4300 3537.621 total 3939.467 Macculay duration in years total/face value of bond 3939.467/1000 3.939467 1.4 modified duration macculay duration/(1+YTM) 3.94/1.05 3.752381 1.5 change in price if YTM increases by .2% modified duration*change in YTM 3.75*.2% 0.75% 1.1 Year

- 8. cash flow present value of cash inflow = cash flow/(1+r)^n r= 5% 1 75 71.42857 2 75 68.02721 3 75 64.78782 4 1075 884.4052 value of bond sum of present value of cash flow 1088.649 1.2 Year cash flow present value of cash inflow = cash flow/(1+r)^n r= 5.2% 1 75 71.29278 2 75 67.7688 3 75 64.41901 4 1075 877.6988 value of bond sum of present value of cash flow 1081.179

- 9. 1.3 % change in bond price if YTM increases by .2% (1081.18-1088.65)/1088.65 -0.69% 1.4 Duration is a measure of a bond's sensitivity to interest rate changes. The higher the bond's duration, the greater its sensitivity to the change (also know as volatility) and vice versa. 1.4 Year cash flow Year*cash flow present value of Year*cash inflow = cash flow/(1+r)^n r= 5% 1 75 75 71.42857 2 75 150 136.0544 3 75 225 194.3635 4 1075 4300 3537.621 total 3939.467 Macculay duration in years total/face value of bond 3939.467/1000 3.939467 1.4 modified duration

- 10. macculay duration/(1+YTM) 3.94/1.05 3.752381 1.5 change in price if YTM increases by .2% modified duration*change in YTM 3.75*.2% 0.75%