Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Similar to Inter-American Centre for Tax Administration (CIAT)

Similar to Inter-American Centre for Tax Administration (CIAT) (20)

More from WE-SECO

More from WE-SECO (12)

Recently uploaded

Recently uploaded (20)

Inter-American Centre for Tax Administration (CIAT)

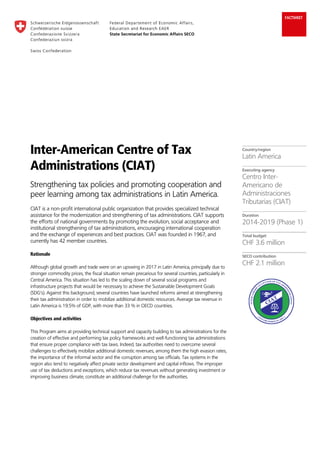

- 1. FACTSHEET Inter-American Centre of Tax Administrations (CIAT) Strengthening tax policies and promoting cooperation and peer learning among tax administrations in Latin America. CIAT is a non-profit international public organization that provides specialized technical assistance for the modernization and strengthening of tax administrations. CIAT supports the efforts of national governments by promoting the evolution, social acceptance and institutional strengthening of tax administrations, encouraging international cooperation and the exchange of experiences and best practices. CIAT was founded in 1967, and currently has 42 member countries. Rationale Although global growth and trade were on an upswing in 2017 in Latin America, principally due to stronger commodity prices, the fiscal situation remain precarious for several countries, particularly in Central America. This situation has led to the scaling down of several social programs and infrastructure projects that would be necessary to achieve the Sustainable Development Goals (SDG’s). Against this background, several countries have launched reforms aimed at strengthening their tax administration in order to mobilize additional domestic resources. Average tax revenue in Latin America is 19.5% of GDP, with more than 33 % in OECD countries. Objectives and activities This Program aims at providing technical support and capacity building to tax administrations for the creation of effective and performing tax policy frameworks and well-functioning tax administrations that ensure proper compliance with tax laws. Indeed, tax authorities need to overcome several challenges to effectively mobilize additional domestic revenues, among them the high evasion rates, the importance of the informal sector and the corruption among tax officials. Tax systems in the region also tend to negatively affect private sector development and capital inflows. The improper use of tax deductions and exceptions, which reduce tax revenues without generating investment or improving business climate, constitute an additional challenge for the authorities. Country/region Latin America Executing agency Centro Inter- Americano de Administraciones Tributarias (CIAT) Duration 2014-2019 (Phase 1) Total budget CHF 3.6 million SECO contribution CHF 2.1 million

- 2. Governance Structure The program is managed and implemented by the CIAT Executive Secretariat, which reports and provides updates on progress to the Executive Council and to the General Assembly, as well as to SECO. Within the Executive Secretariat, the project is managed and coordinated by the International Taxation and Cooperation Directorate, whose Director acts as Program Manager. Depending on the topic, the activities are implemented by the various Directorates of the CIAT Executive Secretariat under the supervision of the Program Manager Results so far In Nicaragua, the Program helped to implement a taxpayer management system that improves customer services and fosters voluntary compliance. In El Salvador, the Program provided support to introduce risk-based tax auditing to combat domestic tax evasion in VAT. It also provided recommendations for the creation of an exchange of information unit within the tax administration. In Guatemala, the Program accompanied the authorities in the introduction of the Electronic Invoice, which included the preparation of the invoice templates. In Honduras, the Program focused on intelligence gathering as well as on securitization of taxpayers’ confidential information. In Bolivia, the Program helped the authorities to implemented extensive controls using sales and stocks registers as well as individual analysis selected randomly. In Guyana, the program provided support for the implementation of transfer pricing regulations based on the model developed by the OECD. How to get involved The selection of the beneficiaries is based on specific requests. CIAT assesses the level of priority of these requests based on the strategy and action plans of recipient tax administrations and after consultation with the Commissioner General. Recipient tax administrations usually provide a financial or in-kind contribution of about 20% of the budget. Further information and contact details Centro Interamericano de Administraciones Tributarias Website: www.ciat.org Email: garias@ciat.org CIAT Coordinator at SECO: Tel.: +41 58 464 07 94 Email: wemu.sekretariat@seco.admin.ch