Downloaded 14 times

![1 www.quandl.com

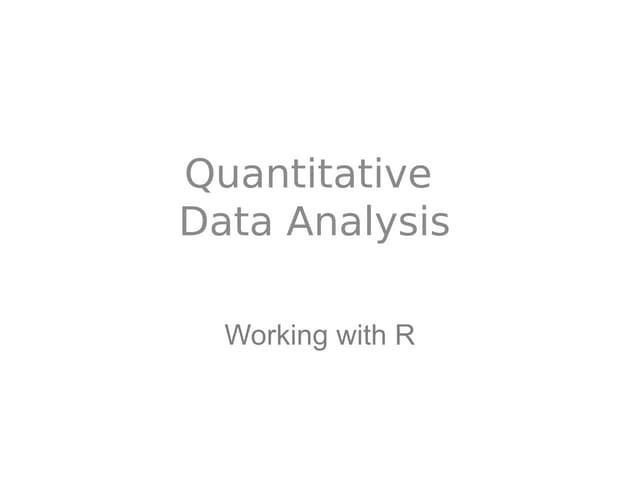

R Cheat Sheet

Vector and Matrix Operations

Construction

c()

cbind()

rbind()

matrix()

Concatenate

Column Concatenate

Row Concatenate

Create matrix

v <- c(1,2,3,4) # 1 2 3 4

cbind(v,v) # 2 Columns

rbind(v,v) # 2 Rows

mat <- matrix(v,nrow=2,ncol=2)

Selection

v[1]

tail(v,1)

mat[2,1]

mat[1,]

mat[,2]

v[c(1,3)]

v[-c(1,3)]

mat[,c(1,2)]

mat[,1:5]

mat[,“col”]

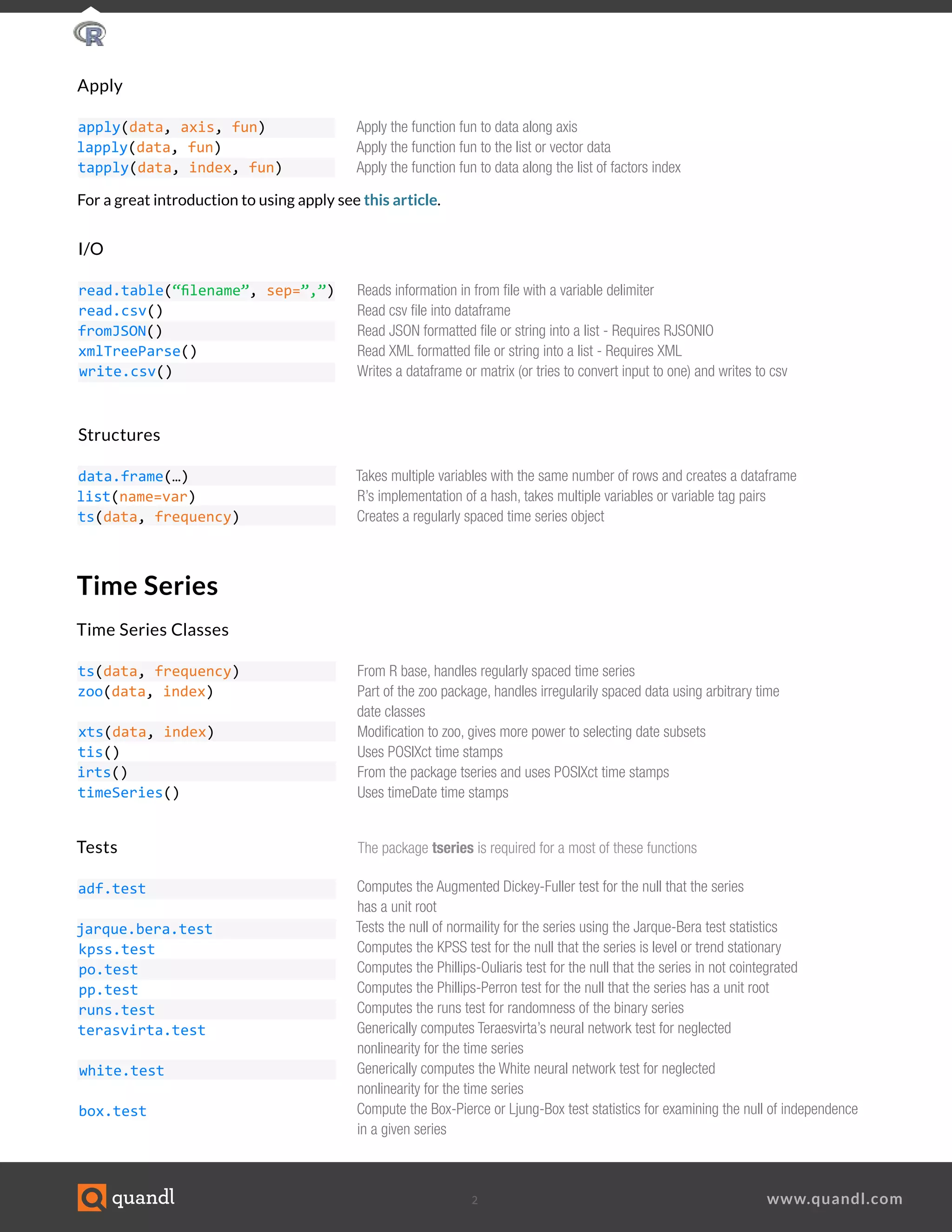

Utility

length()

dim()

sort()

order()

names()

Length of vector

Dimensions of vector/matrix/dataframe

Sorts vector

Index to sort vector e.g. sort(v) == v[order(v)]

Names of columns

Select first

Select last

Select row 2, column 1

Select row 1

Select column 2

Select the first and third values

Select all but the first and third values

Select columns 1 and 2

Select columns 1 to 5

Select column named “col”

Basic Syntax

#

<- or =

<<-

v[1]

*

%*%

/

%/%

%%

Comments

Assignment

Global Assignment

First element in a vector

Scalar Multiplication

Matrix Multiplication

Division

Integer Division

Remainder

# This is not interpreted

a <- 1; b = 2

a <<- 10 # Not recommended

v[1]

c(1,1)*c(1,1) # 1 1

c(1,1)%*%c(1,1) # 2

1/2 # 0.5

1%/%2 # 0

7%%6 # 1

Example](https://image.slidesharecdn.com/rcheatsheet-160617115932/75/R-Cheat-Sheet-1-2048.jpg)

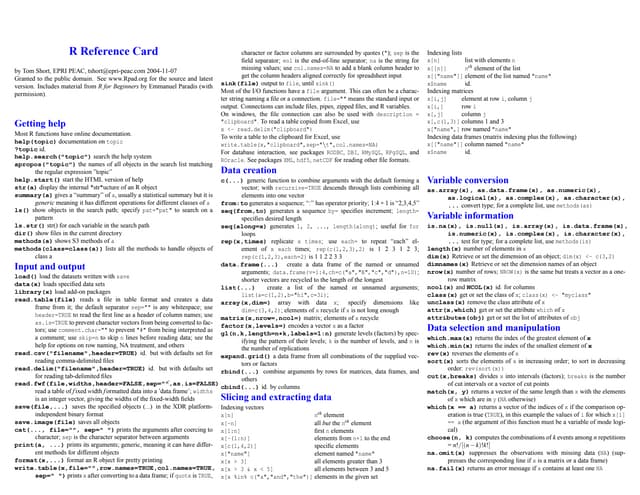

![4 www.quandl.com

Plotting

plot(ts)

title(main, sub, xlab, ylab)

ggplot()

aes()

geom_line()

geom_boxplot()

xlab()

ylab()

ggtitle()

theme()

R base plot function

Adds labels to the currently open plot

Creates a ggplot object

Creates a properly formatted list of variables for use in ggplot

Plots data with a line connecting them

Plots data in the form of box and whiskers plot

Edit the x axis label

Edit the y axis label

Edit the plot title

Modify a large number of options for the plot from grid elements to colors

Aside from the built in plotting function in R, ggplot2 is a very powerful plotting package.

See http://docs.ggplot2.org/current/ for complete documentation.

Plotting example with ggplot2

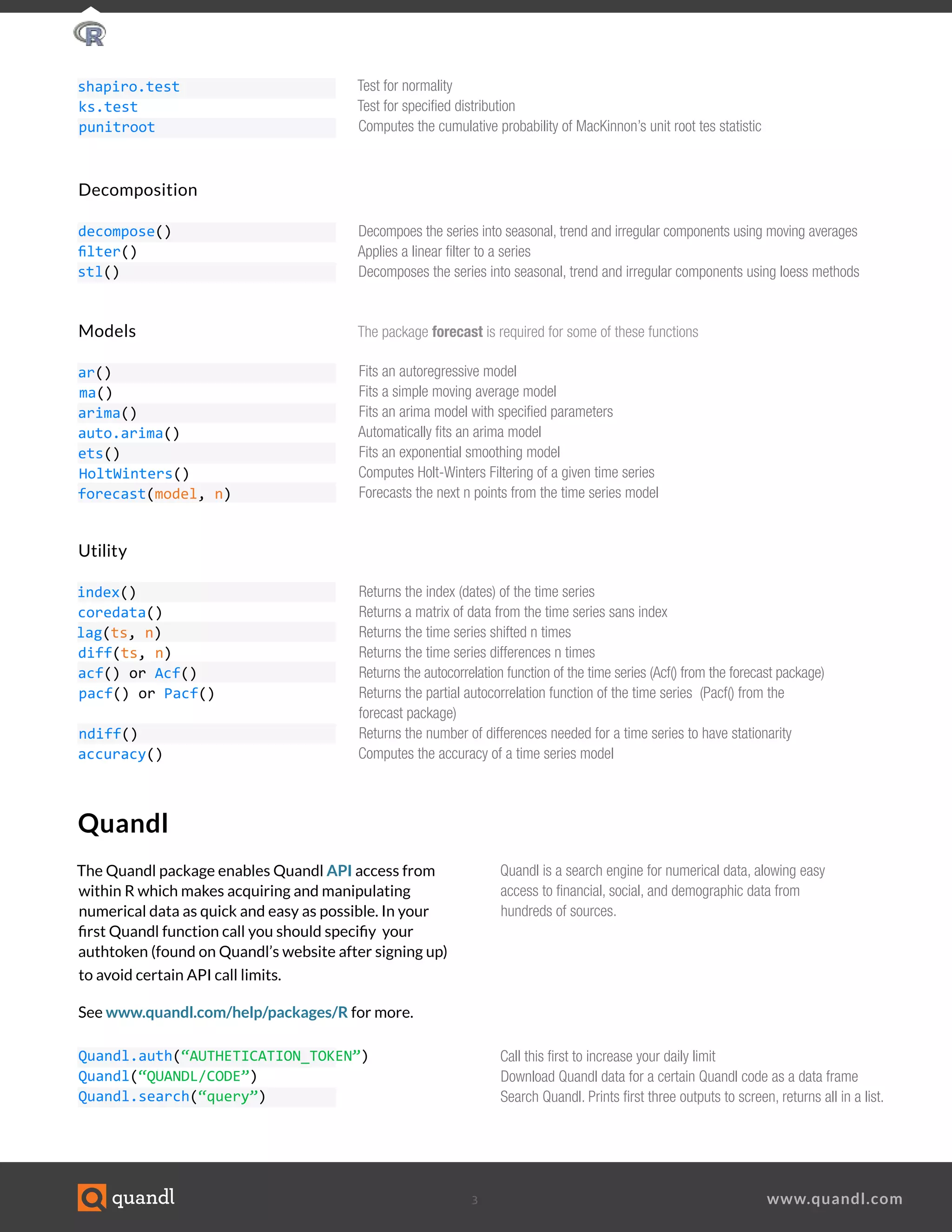

library(Quandl)

library(ggplot2)

data_series <- Quandl(“GOOG/NASDAQ_AAPL”, start_date=”2005-01-01”)[,c(1,5)]

my.plot <- ggplot(data=data_series, aes(x=Date, y=Close)) +

geom_line(color=”#FAB521”) + # Adding a colored line

theme(panel.background = element_rect(fill=’#393939’), panel.grid.major.x = element_blank(),

panel.grid.major.y = element_line(colour=’white’, size=0.1),

panel.grid.minor = element_line(colour=’white’, size=0.1)) + # modifying background color

# and grid options

xlab(“Date”) + ylab(“Closing Price”) + ggtitle(“AAPL”) # Adding titles

my.plot # Generates the plot](https://image.slidesharecdn.com/rcheatsheet-160617115932/75/R-Cheat-Sheet-4-2048.jpg)

This document provides a cheat sheet on vector and matrix operations, time series analysis functions, modeling functions, and plotting functions in R. It includes the basic syntax for constructing and selecting vectors and matrices, as well as functions for time series decomposition, modeling, testing, and plotting time series data. Examples are given for accessing Quandl data and plotting it using ggplot2.

![Introduction to Pandas and Time Series Analysis [PyCon DE]](https://cdn.slidesharecdn.com/ss_thumbnails/introductiontopandasandtimeseriesanalysispyconde-170617163724-thumbnail.jpg?width=640&height=640&fit=bounds)

![[1062BPY12001] Data analysis with R / week 2](https://cdn.slidesharecdn.com/ss_thumbnails/dataanalyzer01-180307063046-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Nikola Rajovic - Hardware Technologies Under the Hood: RISC-V...](https://cdn.slidesharecdn.com/ss_thumbnails/o2gptrmtoyqndgoshwgq-dsc2025-tenstorrent-rajovic-251205090438-814685f5-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Boris Perkovic - Lost in performance.pptx](https://cdn.slidesharecdn.com/ss_thumbnails/uq5hrp7vsuahqkxzifux-1-251204082258-fd2ee09d-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Vid Stimac - Policy Parsimony: Between Oversimplifying and Ov...](https://cdn.slidesharecdn.com/ss_thumbnails/eqlepagzqp2rhg3gbluh-dsc-stimac-251120-251205090438-059e7f54-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Dragana Ilic - AI for Big Data in Astronomy.pptx](https://cdn.slidesharecdn.com/ss_thumbnails/8palya86qaatvjhva1ms-2-dragana-ilic-ai-ilic-251208151906-652b819c-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Goran Obradovic - The Rise of Sovereign AI: Building the Regi...](https://cdn.slidesharecdn.com/ss_thumbnails/7nw2xxixrxqdxvrb5wca-6-251205085714-ab09a2ac-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Dragan Vucic - Building the Learning Organization - How AI Tr...](https://cdn.slidesharecdn.com/ss_thumbnails/8brigo2sbu6qur6gxrra-7-251205085715-6ae07d24-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Bogdan Daniel Maruneac - AI - It starts with you.pptx](https://cdn.slidesharecdn.com/ss_thumbnails/odov3snhrcqs9hx5ny2n-4-251205085715-f1daacfe-thumbnail.jpg?width=640&height=640&fit=bounds)