1. PRESENTATION TITLEPRESENTATION TITLE

GOAL CATEGORIES & THE RMM SOLUTION

1

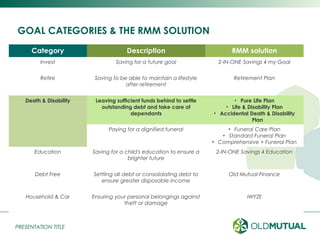

Category Description RMM solution

Invest Saving for a future goal 2-IN-ONE Savings 4 my Goal

Retire Saving to be able to maintain a lifestyle

after retirement

Retirement Plan

Death & Disability Leaving sufficient funds behind to settle

outstanding debt and take care of

dependants

• Pure Life Plan

• Life & Disability Plan

• Accidental Death & Disability

Plan

Paying for a dignified funeral • Funeral Care Plan

• Standard Funeral Plan

• Comprehensive + Funeral Plan

Education Saving for a child's education to ensure a

brighter future

2-IN-ONE Savings 4 Education

Debt Free Settling all debt or consolidating debt to

ensure greater disposable income

Old Mutual Finance

Household & Car Ensuring your personal belongings against

theft or damage

iWYZE

2. PRESENTATION TITLEPRESENTATION TITLE

FINANCIAL GOAL: LEAVING SUFFICIENT FUNDS BEHIND TO

SETTLE OUTSTANDING DEBT AND TAKE CARE OF DEPENDENTS

2

Why would your customers need life & disability cover?

• Settling outstanding debt in the event of death or disability.

• Taking care of dependents financially in the event where the main

breadwinner should die or become disabled.

• Settling outstanding debt in the event of death or disability.

• Taking care of dependents financially in the event where the main

breadwinner should die or become disabled.

3. PRESENTATION TITLEPRESENTATION TITLE

LIFE PLAN RANGE

3

Theory table

Pure Life Plan Life & Disability Plan Accidental Death &

Disability Plan

Eligibility Policyholder only Policyholder only Policyholder only

Minimum entry age 16 16 16

Maximum entry age 60 60 60

Minimum premium Determined by age and cover selected

Maximum premium

Minimum term N/A N/A N/A

Maximum term Whole life Whole life Whole life

Minimum cover/benefit R50 000 R50 000 R50 000

Maximum cover/benefit R500 000 R500 000 R250 000

Maximum cover/benefit

Combined

R750 000

4. PRESENTATION TITLEPRESENTATION TITLE

LIFE PLAN RANGE

4

Pure Life Plan Life & Disability Plan Accidental Death &

Disability Plan

Premium increase To be determined by Old Mutual but expected to also be 5%

Cover/benefit increase 5% 5% 5%

Paid-up benefit

Terminal Illness Benefit

Income Assistance

Benefit

Cessions Allowed

Cash Back Benefit

Premium Holiday

Family Support Services

Yes No Yes No Yes No

Yes No Yes No Yes No

Yes No Yes No Yes No

Yes No Yes No Yes No

Yes No Yes No Yes No

Yes No Yes No Yes No

Yes No Yes No Yes No

5. PRESENTATION TITLEPRESENTATION TITLE

LIFE PLAN RANGE

5

Covered events

Pure Life PlanPure Life Plan Life & Disability PlanLife & Disability Plan

Accidental Death & Disability PlanAccidental Death & Disability Plan

Natural

Causes

Accidental

Causes

Death

Disability

Natural

Causes

Accidental

Causes

Death

Disability

Natural

Causes

Accidental

Causes

Death

Disability

6. PRESENTATION TITLEPRESENTATION TITLE

LIFE PLAN RANGE: EXCLUSIONS

6

•Claims will not be paid if the benefit is not valid or if there is

evidence of fraud

•There will be claims underwriting to investigate fraud and non-

disclosure

•Claims will not be paid if the benefit is not valid or if there is

evidence of fraud

•There will be claims underwriting to investigate fraud and non-

disclosure

Death Exclusions

•Deliberate exposure to exceptional danger, attempted

suicide, self inflicted injury or the insured’s own criminal act.

•War, terrorist activities, riots, civil commotion, rebellion or

insurrection.

•Injury or sickness in respect of which the insured received

treatment of any kind during the three year period

immediately prior to the date he/she became covered for

disability benefits

•Deliberate exposure to exceptional danger, attempted

suicide, self inflicted injury or the insured’s own criminal act.

•War, terrorist activities, riots, civil commotion, rebellion or

insurrection.

•Injury or sickness in respect of which the insured received

treatment of any kind during the three year period

immediately prior to the date he/she became covered for

disability benefits

Disability

Exclusions

7. PRESENTATION TITLEPRESENTATION TITLE

LIFE PLAN RANGE: FEATURES EXPLAINED

What is the Terminal Illness Benefit? (N/A for ADDP)

50% of the benefit will be available after the policy has been in force for at least 5

years if:

Old Mutual’s Chief Medical officer confirms that a covered life is expected to die

within 12 months.

The benefit is in a active status.

No previous terminal illness payments was made from the policy.

The claim of this benefit is prior to the death of the life assured.

Please take note: The remaining 50% of the cover will remain active for as long as

the customer continues to pay premiums and it will pay out on the death of the

covered life.

7

8. PRESENTATION TITLEPRESENTATION TITLE

LIFE PLAN RANGE: FEATURES EXPLAINED

What is a staggered waiting period? (N/A for ADDP)

Earlier in this module you learned what a waiting period is and why it is necessary.

Let’s take a look at how waiting periods work when dealing with the Pure Life Plan

and the Life & Disability Plan.

On death/disability due to natural causes:

8

Money Back

Guarantee

50% of Cover

100% of Cover

6 months

12 months

9. PRESENTATION TITLEPRESENTATION TITLE

On death due to suicide

LIFE PLAN RANGE: FEATURES EXPLAINED

9

24 months

Money Back Guarantee

100% of Cover

On disability due to attempted suicide

Money Back Guarantee

11. PRESENTATION TITLEPRESENTATION TITLE

LIFE PLAN RANGE: FEATURES EXPLAINED

The Income Assistance Benefit? (N/A for ADDP)

11

Waiting period Death due to natural causes Death due to an accident

Income

assistance

portion

Remainder of the

benefit

Income

assistance

portion

Remainder of the

benefit

Less than 6

months No Income

Assistance Benefit

Money Back

Guarantee

10% of Cover up to

a maximum of R50

000

90% of cover

More than 6

months but less

than 12 months

10% of Cover up to

a maximum of R50

000

40% of cover

10% of Cover up to

a maximum of R50

000

90% of cover

Equal to or more

than 12 months

10% of Cover up to

a maximum of R50

000

90% of cover

10% of Cover up to

a maximum of R50

000

90% of cover

12. PRESENTATION TITLEPRESENTATION TITLE

LIFE PLAN RANGE: FEATURES EXPLAINED

12

Income Assistance activity.

Waiting period Death due to natural causes Death due to an accident

Income

assistance

portion

Remainder of

the benefit

Income

assistance

portion

Remainder of

the benefit

Less than 6

months No Income

Assistance Benefit

Money Back

Guarantee

R10 000 R90 000

More than 6

months but less

than 12 months

R10 000 R40 000 R10 000 R90 000

Equal to or

more than 12

months

R10 000 R90 000 R10 000 R90 000

13. PRESENTATION TITLEPRESENTATION TITLE

LIFE PLAN RANGE: FEATURES EXPLAINED

What is a cession? (N/A for ADDP)

In an earlier module you learned that when a customer cedes a policy to a

financial institution as security he/she becomes the cedent and the financial

institution becomes the cessionary.

Below is an illustration of how a cession works.

13

Customer

Financial institution

Life and/or disability coverR500 000

Life and/or disability cover

Bond or loan

R500 000

When a Pure Life Plan or a Life & Disability Plan is ceded to a financial institution,

the waiting period will be waived if:

•The financial institution is willing to accept it as security.

•It is taken out with a new home loan.

•The cession is done within 6 months of taking the new home loan.

14. PRESENTATION TITLEPRESENTATION TITLE

LIFE PLAN RANGE: FEATURES EXPLAINED

When will the benefit cease?

The Pure Life Plan, Life & Disability Plan and Accidental Death & Disability Plan will

cease under the following conditions:

Death of the policyholder

Disability of policyholder, if policyholder claims or stop paying premiums because

of the disability.

If premiums cease, the Premium Holiday Benefit is exhausted and the grace

period used.

If stop order has not started operating 6 months after application

If debit order has not started operating 2 months after signing.

14

15. PRESENTATION TITLEPRESENTATION TITLE

LIFE PLAN RANGE: FEATURES EXPLAINED

15

How does the annual premium and cover increases work?

Cover increases annually on 1 July by 5% provided the policy has been in force for more

than 6 months.

The premium increase can vary annually but it is expected to be the same as the cover

increase. A customer has the option to not pay the increased premium. This would lead to

a situation where Old Mutual must amend the cover .

Following below is an example of how the cover will be amended if a customer chooses

not to pay the increased premium.

A customer purchases a Life &Disability Plan for a R100 000. At July the cover will increase

by 5% and the premium by 3%. The customer does not want to pay the increased

premium.

The cover will be amended as follows:

New cover = R100 000 × (1+5%) ÷ (1+3%)

=R100 000 × 1.05 ÷ 1.03

=R101 942

16. PRESENTATION TITLEPRESENTATION TITLE

LIFE PLAN RANGE: FEATURES EXPLAINED

Who can be the premium payer for the Life Plan Range?

Premiums are payable by stop order from the customer’s pay slip or by debit order

from the bank account of:

The customer

The customer’s spouse

The employer of the customer

What is the Cash Back Benefit? (N/A for Pure Life Plan and Life & Disability Plan)

After every 60 premiums received by Old Mutual, a customer will get a cash back

amount equal to 5 current premiums.

16

17. PRESENTATION TITLEPRESENTATION TITLE

LIFE PLAN RANGE: UNDERWRITING PROCESS

17

Call Centre

The Call centre will call the customer and

ask the relevant medical questions. The

Call Centre could reject application for

the following reasons:

1. Customer could not ne reached after 9

attempts.

2. Customer’s contact details is incorrect.

3. A loading is applied to a stop order

application

Underwriting Department

The Underwriting Department can do one

of three things with the application:

1. Accept

2. Decline

3. Load

Call Centre

The Call Centre will contact the customer

again and give him/her 2 loading

options:

1. Lower cover for the same premium

2. The same cover for a higher premium

(Premium loading)

The Adviser

You have to contact the customer again

to arrange a follow up meeting during

which a new premium must be calculated

should the customer choose to keep the

same cover amount.

18. PRESENTATION TITLEPRESENTATION TITLE

LIFE PLAN RANGE: UNDERWRITING PROCESS

Why do we make use of a call centre in underwriting process?

Benefits for you

Time constraints at point of sale is reduced.

Removes the responsibility from you to ask sensitive medical questions.

Underwriting questions are recorded, this can be used as proof at claim stage.

Benefits for the customer

It is easier for customers to answer sensitive questions coming from someone that they do

not know and probably will never meet.

Customers can choose when they want to be called and this creates a convenient time for

them.

18

19. PRESENTATION TITLEPRESENTATION TITLE

LIFE PLAN RANGE: UNDERWRITING PROCESS FOR HIV+ LIVES

Background

The industry has traditionally shied away from covering the HIV positive customers

on an emotional level.

South Africa’s focus on making anti-retroviral medication available to all and the

fact that the industry now has sufficient statistics to price realistically led to a

scenario where we can offer benefits to HIV + customers.

It is regarded to be a controllable chronic disease like diabetes and rated

accordingly.

At a previous ASISA conference a suggestion was made that smokers may be a

worse risk than certain HIV + risk profiles.

Life expectancy of HIV+ people are now estimated to be around 80-85% that of

an HIV- person.

19

20. PRESENTATION TITLEPRESENTATION TITLE

LIFE PLAN RANGE: UNDERWRITING PROCESS FOR HIV+ LIVES

The following HIV+ customers will be accepted:

Well controlled customers with acceptable CD4 counts and who have been on

anti-retroviral treatment for 12 months or more.

Healthy customers not yet on anti-retroviral treatment but with good CD4 counts.

There is a further requirement for those not on anti-retroviral treatment however:

They need to commence with treatment when recommended and they must

continue with treatment for at least 12 months.

20

21. PRESENTATION TITLEPRESENTATION TITLE

LIFE PLAN RANGE: CALCULATIONS

21

How do you calculate cover?

Premium

- R15

× R1000

÷ Rate

= Cover

How do you calculate premium?

Cover

× Rate

÷ R1000

+ R15

= Premium

Important note: The R15 is known as the base rate and must always be subtracted from the

premium when a customer tells you what premium he/she wants to pay . The R15 base rate

must always be added to the premium when a customer tells you how much cover he/she

wants.

22. PRESENTATION TITLEPRESENTATION TITLE

LIFE PLAN RANGE: CALCULATIONS

22

How do you calculate cover?

Premium R255

- R15 R240

× R1000 R240 000

÷ Rate 1.20

= Cover R200 000

Practical example for cover calculations

Premium: R 255

Rate: 1.20

23. PRESENTATION TITLEPRESENTATION TITLE

LIFE PLAN RANGE: CALCULATIONS

23

How do you calculate premium?

Cover R300 000

× Rate 1.50

÷ R1000 R450 000

+ R15 R450

= Premium R465

Practical example for premium calculations

Cover: R300 000

Rate: 1.50

25. PRESENTATION TITLEPRESENTATION TITLE

IMPORTANT STEPS TO FOLLOW WHEN CALCULATING COVER

AND PREMIUM FOR THE LIFE PLAN RANGE

25

STEP 1

Make sure that you are using the correct plan’s rates. (It is a very common error to use the Life and disability

plan’s rates when a client is actually interested in Pure life plan or visa versa.)

STEP 2

Make sure that you are using the correct age band. (Another common error is to use the age band above

or below the one that you are supposed to use.)

STEP 3

Remember to include the base rate in your calculation when dealing with Pure Life and Life and Disability

Plan.

STEP 4

Do all your calculations more than once. (Your calculator can not make a mistake but you can still input

the incorrect information.)

26. PRESENTATION TITLEPRESENTATION TITLE

Income Assistance Portion Remainder of the benefit

R22 500 (10% of R225 000) R90 000 (40% of R225 000)

QUESTION 1

26

Cover & premium calculations.

Samuel is 38 years old

Rate = 1.70

R225 000 × 1.70 ÷ 1000 + R15 = R397.50

Income Assistance Portion Remainder of the benefit

R22 500 (10% of R225 000) R202 500 (90% of R225 000)

Income Assistance Portion Remainder of the benefit

R0 Money Back Guarantee

27. PRESENTATION TITLEPRESENTATION TITLE

QUESTION 2

27

Maria is 30 years old

Rate = 1.70

(R300-R15) × 1000 ÷ 1.70 = R167 647.06

Income Assistance Portion Remainder of the benefit

R0 Money Back Guarantee

Income Assistance Portion Remainder of the benefit

R16 764.71 (10% of R167 647.06) R150 882.35 (90% of R167 647.06)

Income Assistance Portion Remainder of the benefit

R0 R167 647.06

28. PRESENTATION TITLEPRESENTATION TITLE

QUESTION 3

28

Petso is 43 years old

Rate = 0.90

R100 000 × 0.90 ÷ R1000 = R90

Income Assistance Portion Remainder of the benefit

R0 Money Back Guarantee

Income Assistance Portion Remainder of the benefit

R0 R100 000

Income Assistance Portion Remainder of the benefit

R0 R100 000