Mod 3 Part 6 2-IN-ONE Savings and SPInv Plan as at Oct2014

1. PRESENTATION TITLEPRESENTATION TITLE

GOAL CATEGORIES & THE RMM SOLUTION

1

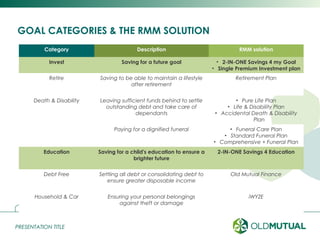

Category Description RMM solution

Invest Saving for a future goal • 2-IN-ONE Savings 4 my Goal

• Single Premium Investment plan

Retire Saving to be able to maintain a lifestyle

after retirement

Retirement Plan

Death & Disability Leaving sufficient funds behind to settle

outstanding debt and take care of

dependants

• Pure Life Plan

• Life & Disability Plan

• Accidental Death & Disability

Plan

Paying for a dignified funeral • Funeral Care Plan

• Standard Funeral Plan

• Comprehensive + Funeral Plan

Education Saving for a child's education to ensure a

brighter future

2-IN-ONE Savings 4 Education

Debt Free Settling all debt or consolidating debt to

ensure greater disposable income

Old Mutual Finance

Household & Car Ensuring your personal belongings

against theft or damage

iWYZE

2. PRESENTATION TITLEPRESENTATION TITLE

2

Why would your customers need to save for a

future goal?

Case study

FINANCIAL GOAL: SAVING FOR A LONG-TERM GOAL

• Saving for a goal, means that you do not have to incur debt to

reach a goal

• Saving over a long term results in better growth for your money

because of compounding

• Saving for a goal, means that you do not have to incur debt to

reach a goal

• Saving over a long term results in better growth for your money

because of compounding

3. PRESENTATION TITLEPRESENTATION TITLE

Who should buy the 2-IN-ONE Savings plans?

The 2-IN-ONE Savings plans are designed for customers who want to commit to a

specific long term goal, but also want access to money during this period if

required.

It is not aimed at customers wanting to save solely for the period shorter than 10

years.

2-IN-ONE SAVINGS PLANS

3

2-IN-ONE Savings plans

Long Term Pocket Short Term Pocket

Build for the future Deal with today

Regulated by the Long Term

Insurance Act

Regulated by the Collective

Investment Schemes Control Act

4. PRESENTATION TITLEPRESENTATION TITLE

What are the age limits?

2-IN-ONE SAVINGS PLANS

4

Product

Minimum entry

age for

policyholder

Maximum entry

age for

policyholder

2-IN-ONE SAVINGS 4 MY GOAL 0 N/A

2-IN-ONE SAVINGS 4 MY GOAL (With Premium

Waiver Option)

16 N/A

2-IN-ONE SAVINGS 4 EDUCATION 0 N/A

2-IN-ONE SAVINGS 4 EDUCATION (With

Premium Waiver Option)

16 N/A

5. PRESENTATION TITLEPRESENTATION TITLE

2-IN-ONE SAVINGS PLANS

5

Product

Minimum entry

age for the child

Maximum entry

age for the child

2-IN-ONE SAVINGS 4 EDUCATION Birth 14

2-IN-ONE SAVINGS 4 EDUCATION (With

Premium Waiver Option)

Birth 14

6. PRESENTATION TITLEPRESENTATION TITLE

2-IN-ONE SAVINGS PLANS

6

What are the minimum and maximum terms?

Product Minimum Terms

When maturity

benefit is

available

2-IN-ONE SAVINGS 4 MY GOAL 10 Any age

2-IN-ONE SAVINGS 4 MY GOAL (With Premium

Waiver Option)

10 Any age

2-IN-ONE SAVINGS 4 EDUCATION 10 Any age

2-IN-ONE SAVINGS 4 EDUCATION (With

Premium Waiver Option)

10 Any age

7. PRESENTATION TITLEPRESENTATION TITLE

HOW CONTRIBUTIONS ARE COLLECTED

7

Total

Contribution

Long Term Pocket Short Term Pocket

R150 R130 R20

R160 R130 R30

R900 R585 R315

R2000 R1300 R700

For contribution from R150 – R200 a month:

R130 goes into long term and the rest goes into

the short terms savings.

For contributions over R200 a month:

65% goes to long term and 35% to short term.

8. PRESENTATION TITLEPRESENTATION TITLE

PREMIUM SPLIT: WITHOUT PREMIUM WAIVER OPTION

8

How is the premium split?

Total Contribution Long term premium Short term contribution

R150 R130 R20

R200 R130 R70

R250 R162.50 R87.50

R300 R195 R105

R400 R260 R140

R500 R325 R175

R1000 R650 R350

9. PRESENTATION TITLEPRESENTATION TITLE

PREMIUM SPLIT: WITH PREMIUM WAIVER OPTION

9

How is the premium split?

Total contribution Long term

premium

Premium for

Premium Waiver

Short term

contribution

R165 R130 R13 R22

R200 R130 R13 R57

R250 R152.58 R15.26 R82.16

R300 R183.10 R18.31 R98.59

R400 R244.13 R24.41 R131.45

R500 R305.17 R30.52 R164.32

R1000 R610.33 R61.03 R328.64

10. PRESENTATION TITLEPRESENTATION TITLE

FEES

10

It is of crucial importance that you disclose these fees to your customers.

This links closely to TCF legislation in that you have to be transparent

regarding anything that could impact a customer’s savings.

11. PRESENTATION TITLEPRESENTATION TITLE

PRODUCT FEATURES

Short -term contribution increases and decreases

A customer can increase or decrease their short term contribution by at least R20

once every year. No changes are allowed for the first 12 months.

Savings top-up

A Top-up can be made anytime, provided that a previous top-up contribution has

been finalised. The top up limits are as follows:

Minimum top-up amount – R250

Maximum top-up amount – R5000

Top-ups can only be made via a once off debit order arranged at a client services

branch. Any amount for the savings top-up will first be used to pay the long-term

premiums that might be in arrears.

11

12. PRESENTATION TITLEPRESENTATION TITLE

When: Savings Boosters is an amount equal to:

After 24 premiums Sum of the last 2 long term premiums

After 60 premiums Sum of the last 3 long term premiums

After 110 premiums Sum of the last 8 long term premiums

PRODUCT FEATURES

Savings boosters

To motivate our customers to be disciplined in their long term savings. Old Mutual

will pay into the long-term pocket, the following:

12

Activity

Amount = R275.60

24

R137.80

23

R137.80

22

R137.80

21

R137.80

20

R137.80

Premiums

13. PRESENTATION TITLEPRESENTATION TITLE

DISABILITY, DEATH & MATURITY

13

Long-term pocket Disability of

policyholder

Death of

policyholder

Maturity

2-IN-ONE Savings 4

my Goal

(Without Premium

Waiver Option)

The customer has 3

options:

1.Continue paying

premiums

2.Request that the

policy be made

paid-up if the

minimum paid-up

value is met.

3.Claim the fund

value with a valid

disability claim

The fund value

available at the time

of death will pay

out, if claimed by

the nominated

beneficiary.

The fund value is

transferred to the

short -term pocket.

2-IN-ONE Savings 4

Education

(Without Premium

Waiver Option)

14. PRESENTATION TITLEPRESENTATION TITLE

DISABILITY, DEATH & MATURITY

14

Short-term pocket Disability of

policyholder

Death of

policyholder

Maturity

2-IN-ONE Savings 4

my Goal

(With and without

Premium Waiver

Option)

If the long-term

pocket is made

paid-up, the short-

term pocket will also

be paid-up.

The fund value

available at the time

of death will pay

into the customer’s

estate.

After the long -term

pocket fund value is

transferred to short

term -pocket, the

short-term Pocket

remains paid-up until

the customer claims

the maturity

proceeds

2-IN-ONE Savings 4

Education

(With and without

Premium Waiver

Option)

15. PRESENTATION TITLEPRESENTATION TITLE

THE PREMIUM WAIVER OPTION

What is the premium waiver option?

It can only be selected on application of the policy.

It protects the customer’s savings only for the first 10 years, irrespective of the

term selected by the customer.

It costs a customer an additional 10% of the long term premium, for10 years only,

thereafter this additional amount is paid to the Long Term Pocket.

There is a 6 months waiting period on death or (certain) disability as a result of

natural causes.

15

16. PRESENTATION TITLEPRESENTATION TITLE

THE PREMIUM WAIVER OPTION

How does the premium waiver work?

The premium waiver comes into effect when the policyholder dies or becomes

disabled. Old Mutual will inject a lump sum, equal to the remainder of the

premiums required up to a term of 10 years. After the lump sum was injected, the

following applies:

2-IN-ONE Savings 4 my Goal – The policy will pay out.

2-IN-ONE Savings 4 Education – The policy will become paid-up.

16

17. PRESENTATION TITLEPRESENTATION TITLE

Activity

THE PREMIUM WAIVER OPTION

1. A customer has a 2-IN-ONE Savings 4 my Goal and dies due to natural causes

after 4 months from applying for the policy.

The fund value available at the time of death will pay out to the beneficiary.

2. A customer has a 2-IN-ONE Savings 4 my Goal and dies due to natural causes

after 2 years from applying for the policy.

Old Mutual will inject a lump sum, equal to the remainder of the premiums

required up to a term of 10 years and the policy will pay out.

3. A customer has a 2-IN-ONE Savings 4 Education and becomes disabled due to

an accident after 1 month from applying for the policy.

Old Mutual will inject a lump sum, equal to the remainder of the premiums

required up to a term of 10 years and the policy will become paid-up.

17

18. PRESENTATION TITLEPRESENTATION TITLE

THE PREMIUM WAIVER OPTION

18

2-IN-ONE Savings 4 my Goal and Education

(With Premium Waiver Option)

Death of Policyholder

Natural Causes Accident

Less than 6

months from

application

date

The fund value available at the time of

death will pay out, if claimed by the

nominated beneficiary.

Waiver benefit applies

More than 6

months from

application

date

Waiver benefit applies Waiver benefit applies

After 10 years The fund value available at the time of death will pay out, if claimed by the

nominated beneficiary.

19. PRESENTATION TITLEPRESENTATION TITLE

THE PREMIUM WAIVER OPTION

19

Disability of Policyholder

Natural Causes Accident

Less than 6

months from

application

date

The customer has 3 options:

1.Continue paying premiums

2.Request that the policy be made

paid-up if the minimum paid-up value is

met.

3.Claim the fund value with a valid

disability claim

Waiver benefit applies

More than 6

months from

application

date

Waiver benefit applies Waiver benefit applies

After 10 years The customer has 3 options:

1.Continue paying premiums

2.Request that the policy be made paid-up if the minimum paid-up value is met.

3.Claim the fund value with a valid disability claim

20. PRESENTATION TITLEPRESENTATION TITLE

CAUSAL EVENTS

20

Long-term pocket Short-term pocket

1 part-withdrawal after every 5 years Money can be withdrawn at any time up to a

balance of R0.

Long-term pocket Short-term pocket

Surrender value is available at any time Will automatically surrender when long-term pocket

is surrendered

Long-term pocket Short-term pocket

Will automatically become paid-up when customer

stops paying premiums and the premium holiday

benefit and the grace period is used if the value is

greater than R1000.

Customer can also request for it to be made paid-up

if the minimum paid-up value is met.

Will also be paid-up if the long-term pocket is paid-

up.

Part-withdrawals

Surrender

Paid-up

21. PRESENTATION TITLEPRESENTATION TITLE

FEES & CHARGES APPLICABLE FOR CAUSAL EVENTS

21

Event Fees & Charges

Part withdrawal

R300* + reducing fee.

Sum must not be more than 30% of fund value

Paid-up

Surrender (from active status)

Surrender (from paid-up status) R155*, which must not be more than 30% of fund

value

Under certain extreme circumstances (for instance, investment market crash), we

may reduce the Part Withdrawal and the Surrender Values by a percentage as a

protective measure. Once the market normalises, the reduction percentage may

be removed.

24. PRESENTATION TITLEPRESENTATION TITLE

THE REDUCING FEE: SAVINGS PLAN WITH A TERM OF 30 YEARS

24

15%

0%

Application 10 years

Charge term

10 years/2 = 15 years

Maximum penalty term is 10

years.

25. PRESENTATION TITLEPRESENTATION TITLE

HOW SAVINGS ARE INVESTED

Long Term Pocket

1. Savings in the Long Term Pocket are all invested in the Old Mutual Smoothed

Bonus Fund.

2. The fund then invests in a mix of investments, such as:

a) High growth investments: Shares

b) Medium growth investments: Property

c) Low growth investments: Bonds

d) Foreign investments: All of the above

25

26. PRESENTATION TITLEPRESENTATION TITLE

HOW SAVINGS ARE INVESTED

3. This is a medium risk fund: Under bad market conditions, customers may get less

than what was invested.

4. Customers’ savings grow by bonuses declared each year for the previous year.

5. Guaranteed to receive not less than sum of the accumulated net premiums at:

a) Maturity

b) or death.

6. Guarantee falls away on taking part-withdrawals or surrender of policy.

26

The yearly bonuses we declare are not guaranteed. This means that the

bonus may be reversed in extreme market conditions.

27. PRESENTATION TITLEPRESENTATION TITLE

HOW SAVINGS ARE INVESTED

Short Term Pocket

1. Savings in the Short Term Pocket are all invested in the Old Mutual Money

Market Fund.

2. The fund then invests in cash and other banking investments.

3. This is a low risk fund: Very small chance that customers would get less than

what was invested.

4. Customers’ savings grow by interest, which is added at the end of each month.

5. For customers exiting, the interest earned up that day is added.

27

28. PRESENTATION TITLEPRESENTATION TITLE

2-IN-ONE SAVINGS 4 EDUCATION: EXCLUSIVE FEATURES

What limits apply to children?

A customer can take out the 2-IN-ONE Savings 4 Education for any child, it does

not have to be a dependent, own or legally adopted child.

A customer can change the name of the child on the plan for any reason and

at any time.

The investment term for the child will be determined by the age of the child.

The normal age at which a child finishes with school is at 18. It would make sense

for a customer to select a term that would reach maturity when the child reaches

18 or 19 years.

28

29. PRESENTATION TITLEPRESENTATION TITLE

2-IN-ONE SAVINGS 4 EDUCATION: EXCLUSIVE FEATURES

What happens on death or disability of the child?

On death or disability of the child the customer has the following options:

Replace the child on the plan with another child and continue paying premiums.

Request the fund value to be paid out with a valid disability or death claim.

Request for the policy to be made paid-up if minimum paid-up value is met.

29

31. PRESENTATION TITLEPRESENTATION TITLE

THE SINGLE PREMIUM INVESTMENT PLAN

31

Single Premium Investment Plan

Minimum entry age for policyholder None

Maximum entry age for Policyholder None

Minimum premium R2000

Maximum premium R200 000

Minimum term 5 years

Maximum term None

Who can be the premium payer? Anyone can pay

32. PRESENTATION TITLEPRESENTATION TITLE

THE SINGLE PREMIUM INVESTMENT PLAN

32

Single Premium Investment Plan

Premium Holiday

Surrender value available?

Part-withdrawals allowed?

Paid-up option available?

API applicable?

Family Support Services

Excluding Funeral Support

Yes No

Yes No

Yes No

Yes No

Yes No

Yes No