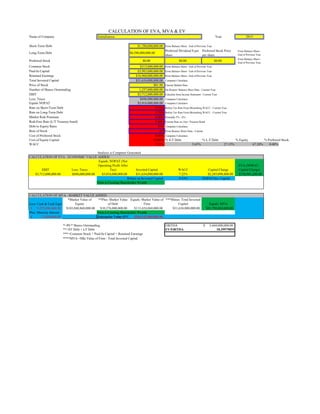

1. CALCULATION OF EVA, MVA & EV

Name of Company AstraZeneca Year 2013

Short-Term Debt $1,788,000,000.00 From Balance Sheet - End of Previous Year

Long-Term Debt $8,588,000,000.00

Preferred Dividend $ per

share

Preferred Stock Price

per share

From Balance Sheet -

End of Previous Year

Preferred Stock $0.00 $0.00 $0.00

From Balance Sheet -

End of Previous Year

Common Stock $315,000,000.00 From Balance Sheet - End of Previous Year

Paid-In Capital $3,983,000,000.00 From Balance Sheet - End of Previous Year

Retained Earnings $16,960,000,000.00 From Balance Sheet - End of Previous Year

Total Invested Capital $31,634,000,000.00 Computer Calculates

Price of Stock $81.98 Current Market Data

Number of Shares Outstanding 1,257,000,000.00 On Reuters' Balance Sheet Data - Current Year

EBIT $3,712,000,000.00 Calculate from Income Statement - Current Year

Less: Taxes $696,000,000.00 Computer Calculates

Equals NOPAT $3,016,000,000.00 Computer Calculates

Rate on Short-Term Debt 5.31% Before Tax Rate From Bloomberg WACC - Current Year

Rate on Long-Term Debt 5.70% Before Tax Rate From Bloomberg WACC - Current Year

Market Risk Premium 6.00% Normally 5% - 6%

Risk-Free Rate (L/T Treasury bond) 5.00% Current Rate on 10yr. Treasury Bond

Debt to Equity Ratio 0.49 Computer Calculates

Beta of Stock 0.5 From Reuters' Ratio Data - Current

Cost of Preferred Stock 0.00% Computer Calculates

Cost of Equity Capital 8.000% % S-T Debt % L-T Debt % Equity % Preferred Stock

WACC 7.22% 5.65% 27.15% 67.20% 0.00%

Analysis is Computer Generated

CALCULATION OF EVA - ECONOMIC VALUE ADDED

EBIT Less: Taxes

Equals: NOPAT (Net

Operating Profit After

Tax) Invested Capital WACC Capital Charge

EVA (NOPAT -

Capital Charge)

$3,712,000,000.00 $696,000,000.00 $3,016,000,000.00 $31,634,000,000.00 7.22% $2,285,098,800.00 $730,901,200.00

Return on Invested Capital 9.53% NOPAT/Inv. Capital

Firm is Creating Shareholder Wealth

CALCULATION OF MVA - MARKET VALUE ADDED

Less: Cash & Cash Equiv

*Market Value of

Equity

**Plus: Market Value

of Debt

Equals: Market Value of

Firm

***Minus: Total Invested

Capital Equals: MVA

9,297,000,000.00$ $103,048,860,000.00 $10,376,000,000.00 $113,424,860,000.00 $31,634,000,000.00 $81,790,860,000.00

Plus: Minority Interest Firm is Creating Shareholder Wealth

15,000,000.00$ Enterprise Value (EV) $104,142,860,000.00

*=P0 * Shares Outstanding EBITDA 5,660,000,000.00$

**=ST Debt + LT Debt EV/EBITDA 18.39979859

***=Common Stock + Paid-In Capital + Retained Earnings

****MVA =Mkt Value of Firm - Total Invested Capital