Value Proposition canvas- Customer needs and pains

A Mulligan for Capesize Owners ?

1. Tanker Opinions are published by the Tanker Research & Consulting department at Poten & Partners. For feedback on this opinion, to receive this via email every week, or for information on our

services and research products, please send an email to tankerresearch@poten.com. Please visit our website at www.poten.com to contact our tanker brokers.

How bulker conversions will impact the tanker market

While the tanker market has gone from strength to

strength on the back of sharply lower oil prices and

moderate fleet expansion, the dry cargo market, in

general, and capesize bulk carriers, in particular, are in

the doldrums. The dry bulk orderbook for 2015 and

2016 delivery remains high, in particular for Capesize

vessels. Is it realistic to expect that a significant portion

of these large bulk carriers are going to be converted to

Aframax or Suezmax tankers?

Scorpio announced recently that it had reached

agreements with shipyards in South Korea and Romania

to modify six newbuilding contracts for Capesize bulk

carriers into newbuilding contracts for LR2 product

tankers. It has been reported that several other owners

are currently negotiating with shipyards as well. Is this

the beginning of a trend?

We caution against expecting too many additional

conversions to come to fruition. For these deals to

materialize a number of elements need to fall into place.

Firstly, the yard needs to be able to build and have

current designs for both bulkers and tankers. Secondly,

these yards need to be willing to switch the order. This

will probably be possible only for owners with a certain

stature that have ordered a series of vessels at that yard.

The shipbuilder will want to ensure that these

conversions do not significantly interrupt planned

construction and procurement. Shipyards are also keen

to maintain their profit margins when changing from one

vessel-type to the other.

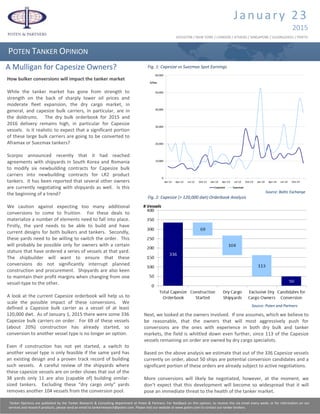

A look at the current Capesize orderbook will help us to

scale the possible impact of these conversions. We

January 23

2015

POTEN TANKER OPINION

HOUSTON / NEW YORK / LONDON / ATHENS / SINGAPORE / GUANGZHOU / PERTH

defined a Capesize bulk carrier as a vessel of at least

120,000 dwt. As of January 1, 2015 there were some 336

Capesize bulk carriers on order. For 69 of these vessels

(about 20%) construction has already started, so

conversion to another vessel type is no longer an option.

Even if construction has not yet started, a switch to

another vessel type is only feasible if the same yard has

an existing design and a proven track record of building

such vessels. A careful review of the shipyards where

these capesize vessels are on order shows that out of the

38 yards only 11 are also (capable of) building similar-

sized tankers. Excluding these “dry cargo only” yards

removes another 104 vessels from the conversion pool.

Fig. 1: Capesize vs Suezmax Spot EarningsA Mulligan for Capesize Owners?

Next, we looked at the owners involved. If one assumes, which we believe to

be reasonable, that the owners that will most aggressively push for

conversions are the ones with experience in both dry bulk and tanker

markets, the field is whittled down even further, since 113 of the Capesize

vessels remaining on order are owned by dry cargo specialists.

Based on the above analysis we estimate that out of the 336 Capesize vessels

currently on order, about 50 ships are potential conversion candidates and a

significant portion of these orders are already subject to active negotiations.

More conversions will likely be negotiated, however, at the moment, we

don’t expect that this development will become so widespread that it will

pose an immediate threat to the health of the tanker market.

Fig. 2: Capesize (> 120,000 dwt) Orderbook Analysis

Source: Poten and Partners

Source: Baltic Exchange