Difference between balance sheet of manufacturing sector and banking sector

•Download as DOCX, PDF•

4 likes•10,742 views

Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Viewers also liked (13)

Similar to Difference between balance sheet of manufacturing sector and banking sector

Similar to Difference between balance sheet of manufacturing sector and banking sector (20)

More from Muhammad Zeeshan Baloch

More from Muhammad Zeeshan Baloch (20)

Recently uploaded

Recently uploaded (20)

Difference between balance sheet of manufacturing sector and banking sector

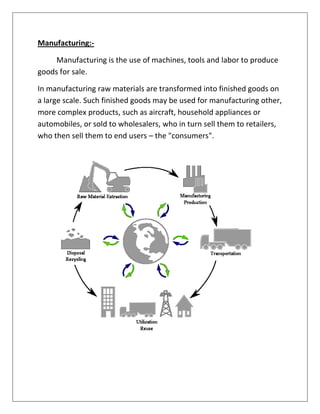

- 1. Manufacturing:- Manufacturing is the use of machines, tools and labor to produce goods for sale. In manufacturing raw materials are transformed into finished goods on a large scale. Such finished goods may be used for manufacturing other, more complex products, such as aircraft, household appliances or automobiles, or sold to wholesalers, who in turn sell them to retailers, who then sell them to end users – the "consumers".

- 2. Explanation:- As you can see in the diagram that first raw material is extracted. Second, it is transferred into output. Third it is transported. Forth it is utilized. Fifth it is disposed. After disposing it is recycled and is used as a raw material. This all work is done in manufacturing sector. Bank:- A bank is a financial institution that serves as a financial intermediary. The term "bank" may refer to one of several related types of entities: 1. Central bank 2. Commercial bank 3. Saving bank Activities of bank:- Some activities of a bank are 1. Collecting deposits from customers and giving them interest 2. Lending loans to customers (With an interest) 3. Safeguarding customers valuables by means of safe deposit vaults 4. Provide investment services like Mutual funds 5. Provide Depository services (DEMAT Accounts, Share trading etc)

- 3. The above mentioned list is not exhaustive but are some of the major functions provided by banks these days. The above all activities are performed in banking sector. Important point:- The main source of income of manufacturing sector is to sell his final goods in consumer market. A Bank's main source of income is interest. A bank pays out at a lower interest rate on deposits and receives a higher interest rate on loans. The difference between these rates represents the bank's net income. Similarities of both sectors balance sheet:- First we write accounting equation: Assets= Liabilities+ Owner’s equity In any company balance sheet we will see these things that are common. 1. Both have current assets and long term assets. 2. Both have current liabilities and long term liabilities. 3. Both have shareholders that buy the shares of the company.

- 4. Current assets of manufacturing company:- Manufacturing company current assets include cash, accounts receivable, inventory, marketable securities, and prepaid expenses. Current assets of bank:- Bank current assets include Negotiable certificates of deposit, Marketable securities, due from banks, Cash held in trust, Interest-bearing deposits in other banks. Current liabilities of manufacturing company:- Accounts payable for goods, services or supplies that were purchased for use in the operation of the business and payable within a normal period of time would be current liabilities. Current liabilities of bank:- Current liabilities include savings accounts, regular checking accounts, NOW (Negotiable Order of Withdrawal) accounts, money market deposit accounts. Short-term borrowings are usually from banks, securities dealers, the Federal Home Loan Bank, unsecured federal funds borrowings, which generally mature daily. Dividend payable (preferred stock). Long term assets of manufacturing company:- Long term assets are land, building, plants, machinery, motor vehicles, office, and computers.

- 5. Long term assets of bank:- Bank long term assets are land, machinery, building, motor vehicles, computers and furniture. Long term liabilities of manufacturing company:- Long term financing, liabilities against assets subject to finance lease, deferred liability for staff gratuity. Long term liabilities of bank:- Long term borrowing, sub-ordinate loans, fixed deposit. Difference between manufacturing sector and banking sector:- 1. In manufacturing 1. In banking sector the sector the main main source of source of income is income is interest. to sell his goods in Some other sources consumer market, are fees charges. interest on short term deposit. 2. In manufacturing 2. In banking sector sector raw material deposit is used as an is used as an input. input. 3. In manufacturing 3. In banking sector sector final goods are interest is considered considered as output. output because when a financial institution

- 6. (bank) gives loan to people then he charges interest on the loan for a certain period of time when maturity date comes. 4. Manufacturing 4. Banks earn profit companies may be in either it is high or loss because there low. They have loss in are many the shape of bad competitors to sell debts, investment same good in the securities. market. 5. The manufacturing 5. The banking sector sector has machinery also has machinery like: like: Computer Computer Plants ATM machines Because the machinery is when we give him input he gives us output.

- 7. Manufacturing Company This is a manufacturing company balance sheet as you can see that there are few things that are different from the bank balance sheet. They have assets but what assets they have in the assets that are not in bank balance sheet. Inventory Account receivable Account payable We see that in bank balance sheet there is no term like this because they do the business of finance that is a paper and manufacturing companies do the business of real goods that are consumed by consumer. The inventory is held by manufacturing company in three shapes: 1. Raw material 2. Work in progress 3. Finished goods

- 8. Bank The primary asset categories for a bank Omni Bank Omni bank Balance sheet assets are, of course, what the bank owns. Omni Bank, being a representative bank, has four main categories of assets listed on the balance sheet at the right: 1. Physical assets: This includes the buildings, land, furniture, and equipment owned by the bank. 2. Loans:- Loans are the primary source of interest revenue. While a loan is a liability for the borrower, it is an asset for the bank, for the lender. This asset includes loans to consumers (home loans, personal loans, automobile loans, credit card loans) and businesses (real estate development loans, capital investment loans). 3. Reserves:- This is small in amount, it is extremely important. Reserves are what banks use for daily transactions, such as processing checks or satisfying cash withdrawals. Banks use reserves to ensure the security of deposits. Two varieties of reserves worth noting are vault cash (the actual paper currency and coins that is kept in the bank, that is, in the vault) and Federal Reserve deposits (deposits that banks keep with the Federal Reserve System to clear checks and assist in other banking activities). 4. Investment securities:- They pay more interest than reserves, but not as much as loans. If a bank has a few extra reserves, but is not ready to lock in loans for the long term, then investment securities are the answer.