Exports under GST : LUT & Bond

•

1 like•2,233 views

Exports Under GST: How to Use Bond or LUT?

Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Viewers also liked (10)

Similar to Exports under GST : LUT & Bond

Similar to Exports under GST : LUT & Bond (20)

Recently uploaded

Recently uploaded (20)

Exports under GST : LUT & Bond

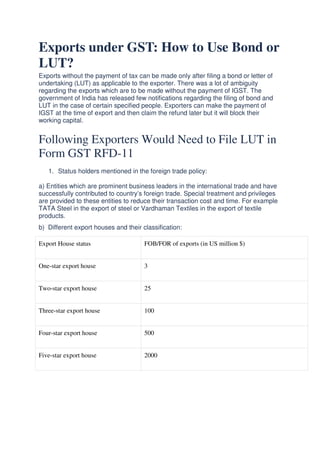

- 1. Exports under GST: How to Use Bond or LUT? Exports without the payment of tax can be made only after filing a bond or letter of undertaking (LUT) as applicable to the exporter. There was a lot of ambiguity regarding the exports which are to be made without the payment of IGST. The government of India has released few notifications regarding the filing of bond and LUT in the case of certain specified people. Exporters can make the payment of IGST at the time of export and then claim the refund later but it will block their working capital. Following Exporters Would Need to File LUT in Form GST RFD-11 1. Status holders mentioned in the foreign trade policy: a) Entities which are prominent business leaders in the international trade and have successfully contributed to country’s foreign trade. Special treatment and privileges are provided to these entities to reduce their transaction cost and time. For example TATA Steel in the export of steel or Vardhaman Textiles in the export of textile products. b) Different export houses and their classification: Export House status FOB/FOR of exports (in US million $) One-star export house 3 Two-star export house 25 Three-star export house 100 Four-star export house 500 Five-star export house 2000

- 2. C) Manufacturers who are also status holders as per (a) and (b) they will be permitted by to self-certify the goods as manufactured as per their Industrial Entrepreneur Memorandum (IEM) / Industrial Licence (IL)/ Letter of Intent (LOI). 2. Registered person who has received foreign currency for at least a total of 10% of the exports turnover and such value is more than 1 Crore in the preceding financial year would be required to file a letter of undertaking (LUT). *The applicant shall not have been prosecuted under the CGST act 2017 or any other current laws for an amount exceeding INR 250 Lakhs. Export by Issuing Bond Any other registered person other than mentioned above doing exports without the payment of IGST would need to file a bond which is available in the form GST RFD- 11 under GST. Small exporters should file GST RFD-11 prior to the export if they want to avoid the blocking of working capital. A detailed analysis of the form GST RFD-11 is provided in our series of article on refund forms. You would need to select which type of document is furnished (Bond or LUT) in the form GST RFD-11. Conclusion Relief and clarification have been provided to the exporters to continue exporting without the payment of tax and the blockage of working capital.