Daily Market Report April 12, 2016

•

0 likes•211 views

The QSE Index rose 0.3% led by gains in the Consumer Goods & Services and Insurance indices. National Leasing and Mazaya Qatar Real Estate Development were the top gainers rising 10.0% and 9.9% respectively. Regional indices were mixed with Saudi Arabia falling 0.5% while Kuwait gained 0.6%. Ezdan Holding Group plans to raise $2bn Sukuk to finance real estate mega projects.

Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Viewers also liked (20)

Similar to Daily Market Report April 12, 2016

Similar to Daily Market Report April 12, 2016 (20)

More from QNB Group

More from QNB Group (20)

Recently uploaded

Recently uploaded (20)

Daily Market Report April 12, 2016

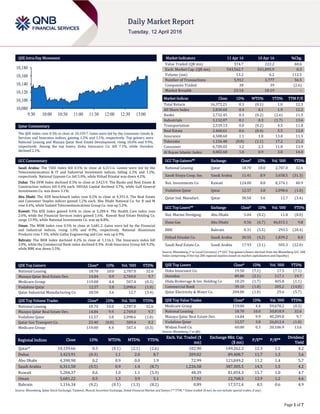

- 1. Page 1 of 7 QSE Intra-Day Movement Qatar Commentary The QSE Index rose 0.3% to close at 10,159.7. Gains were led by the Consumer Goods & Services and Insurance indices, gaining 1.2% and 1.1%, respectively. Top gainers were National Leasing and Mazaya Qatar Real Estate Development, rising 10.0% and 9.9%, respectively. Among the top losers, Doha Insurance Co. fell 7.1%, while Ooredoo declined 2.1%. GCC Commentary Saudi Arabia: The TASI Index fell 0.5% to close at 6,311.6. Losses were led by the Telecommunication & IT and Industrial Investment indices, falling 2.3% and 1.2%, respectively. National Gypsum Co. fell 5.0%, while Etihad Etisalat was down 4.2%. Dubai: The DFM Index declined 0.3% to close at 3,423.9. The Banks and Real Estate & Construction indices fell 0.4% each. SHUAA Capital declined 3.7%, while Gulf General Investments Co. was down 3.1%. Abu Dhabi: The ADX benchmark index rose 0.2% to close at 4,391.0. The Real Estate and Consumer Staples indices gained 1.2% each. Abu Dhabi National Co. for B and M rose 6.4%, while Sudatel Telecommunications Group Co. was up 5.2%. Kuwait: The KSE Index gained 0.6% to close at 5,284.4. The Health Care index rose 2.6%, while the Financial Services index gained 1.6%. Kuwait Real Estate Holding Co. surge 13.9%, while National Investments Co. was up 8.8%. Oman: The MSM Index rose 0.5% to close at 5,681.2. Gains were led by the Financial and Industrial indices, rising 1.0% and 0.9%, respectively. National Aluminium Products rose 7.3%, while Galfar Engineering and Con. was up 6.9%. Bahrain: The BHB Index declined 0.2% to close at 1,116.3. The Insurance index fell 2.0%, while the Commercial Bank index declined 0.3%. Arab Insurance Group fell 9.2%, while BBK was down 5.5%. QSE Top Gainers Close* 1D% Vol. ‘000 YTD% National Leasing 18.70 10.0 2,787.0 32.6 Mazaya Qatar Real Estate Dev. 14.84 9.9 2,769.0 9.7 Medicare Group 119.00 4.4 507.4 (0.3) Vodafone Qatar 12.57 3.8 2,098.6 (1.0) Qatar Industrial Manufacturing Co 38.50 3.6 12.7 (3.4) QSE Top Volume Trades Close* 1D% Vol. ‘000 YTD% National Leasing 18.70 10.0 2,787.0 32.6 Mazaya Qatar Real Estate Dev. 14.84 9.9 2,769.0 9.7 Vodafone Qatar 12.57 3.8 2,098.6 (1.0) Qatar Gas Transport Co. 23.40 (0.0) 509.4 0.2 Medicare Group 119.00 4.4 507.4 (0.3) Market Indicators 11 Apr 16 10 Apr 16 %Chg. Value Traded (QR mn) 374.7 222.2 68.6 Exch. Market Cap. (QR mn) 543,562.7 541,895.9 0.3 Volume (mn) 13.2 6.2 112.5 Number of Transactions 5,912 3,777 56.5 Companies Traded 38 39 (2.6) Market Breadth 23:14 18:19 – Market Indices Close 1D% WTD% YTD% TTM P/E Total Return 16,372.21 0.3 (0.1) 1.0 12.3 All Share Index 2,830.60 0.4 0.1 1.9 12.2 Banks 2,732.45 0.3 (0.2) (2.6) 11.5 Industrials 3,132.07 0.1 0.3 (1.7) 13.6 Transportation 2,539.13 0.0 (0.2) 4.5 11.8 Real Estate 2,460.61 0.6 (0.4) 5.5 12.0 Insurance 4,588.60 1.1 1.8 13.8 11.5 Telecoms 1,156.48 (0.8) (1.1) 17.2 21.2 Consumer 6,709.02 1.2 2.3 11.8 13.9 Al Rayan Islamic Index 4,002.68 1.0 0.9 3.8 14.0 GCC Top Gainers## Exchange Close# 1D% Vol. ‘000 YTD% National Leasing Qatar 18.70 10.0 2,787.0 32.6 Saudi Enaya Coop. Ins. Saudi Arabia 11.41 8.9 3,658.5 (31.3) Nat. Investments Co Kuwait 124.00 8.8 8,374.1 40.9 Vodafone Qatar Qatar 12.57 3.8 2,098.6 (1.0) Qatar Ind. Manufact. Qatar 38.50 3.6 12.7 (3.4) GCC Top Losers## Exchange Close# 1D% Vol. ‘000 YTD% Nat. Marine Dredging Abu Dhabi 5.04 (8.2) 11.8 (8.0) Dana Gas Abu Dhabi 0.56 (6.7) 46,015.1 9.8 BBK Bahrain 0.31 (5.5) 293.5 (28.4) Etihad Etisalat Co. Saudi Arabia 30.55 (4.2) 1,839.2 8.0 Saudi Real Estate Co. Saudi Arabia 17.93 (3.1) 505.3 (22.0) Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the Bloomberg GCC 200 Index comprising of the top 200 regional equities based on market capitalization and liquidity) QSE Top Losers Close* 1D% Vol. ‘000 YTD% Doha Insurance Co. 19.50 (7.1) 17.5 (7.1) Ooredoo 89.80 (2.1) 117.1 19.7 Dlala Brokerage & Inv. Holding Co 18.29 (1.7) 405.8 (1.1) Commercial Bank 39.10 (1.0) 205.2 (14.8) Qatar Electricity & Water Co. 204.00 (1.0) 29.6 (5.7) QSE Top Value Trades Close* 1D% Val. ‘000 YTD% Medicare Group 119.00 4.4 59,678.2 (0.3) National Leasing 18.70 10.0 50,818.9 32.6 Mazaya Qatar Real Estate Dev. 14.84 9.9 40,289.8 9.7 Vodafone Qatar 12.57 3.8 26,012.4 (1.0) Widam Food Co. 60.00 0.3 20,186.9 13.6 Source: Bloomberg (* in QR) Regional Indices Close 1D% WTD% MTD% YTD% Exch. Val. Traded ($ mn) Exchange Mkt. Cap. ($ mn) P/E** P/B** Dividend Yield Qatar* 10,159.66 0.3 (0.1) (2.1) (2.6) 102.90 149,262.3 12.3 1.5 4.2 Dubai 3,423.91 (0.3) 1.1 2.0 8.7 209.02 89,408.7 11.7 1.3 3.6 Abu Dhabi 4,390.98 0.2 0.9 0.0 1.9 72.99 123,849.2 11.2 1.4 5.7 Saudi Arabia 6,311.58 (0.5) 0.9 1.4 (8.7) 1,226.58 387,305.5 14.5 1.5 4.2 Kuwait 5,284.37 0.6 1.0 1.1 (5.9) 48.39 81,854.3 15.7 1.0 4.7 Oman 5,681.22 0.5 1.3 3.9 5.1 17.92 22,768.3 12.9 1.2 4.6 Bahrain 1,116.34 (0.2) (0.1) (1.3) (8.2) 0.89 17,572.4 8.5 0.6 4.9 Source: Bloomberg, Qatar Stock Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any) 10,080 10,100 10,120 10,140 10,160 10,180 9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

- 2. Page 2 of 7 Qatar Market Commentary The QSE Index rose 0.3% to close at 10,159.7. The Consumer Goods & Services and Insurance indices led the gains. The index rose on the back of buying support from non-Qatari and GCC shareholders despite selling pressure from Qatari shareholders. National Leasing and Mazaya Qatar Real Estate Development were the top gainers, rising 10.0% and 9.9%, respectively. Among the top losers, Doha Insurance Co. fell 7.1%, while Ooredoo declined 2.1%. Volume of shares traded on Monday rose by 112.5% to 13.2mn from 6.2mn on Sunday. Further, as compared to the 30-day moving average of 11.3mn, volume for the day was 16.6% higher. National Leasing and Mazaya Qatar Real Estate Development were the most active stocks, contributing 21.1% and 21.0% to the total volume, respectively. Source: Qatar Stock Exchange (* as a % of traded value) Ratings, Earnings Releases, Global Economic Data and Earnings Calendar Ratings Updates Company Agency Market Type* Old Rating New Rating Rating Change Outlook Outlook Change Qatar International Islamic Bank (QIIK) Capital Intelligence Qatar FSR/LT FCR/ST FCR –/A/A2 A-/A/A2 – Positive – Qatar Islamic Bank (QIBK) Capital Intelligence Qatar FSR/LT FCR/ST FCR/SR A/A/A2/2 A/A/A2/2 – Stable – Source: News reports (* LT – Long Term, ST – Short Term, FSR- Financial Strength Rating, FCR – Foreign Currency Rating, LCR – Local Currency Rating, IDR – Issuer Default Rating, SR – Support Rating, LC – Local Currency) Earnings Releases Company Market Currency Revenue (mn) 1Q2016 % Change YoY Operating Profit (mn) 1Q2016 % Change YoY Net Profit (mn) 1Q2016 % Change YoY United Wire Factories Co. Saudi Arabia SR – – 20.2 27.8% 17.3 23.6% Oman Cables Industry Oman OMR 61.5 -15.9% – – 4.7 -2.4% Oman Chlorine Oman OMR 1.8 -2.6% 0.9 -4.0% 0.5 -17.3% Source: Company data, DFM, ADX, MSM Global Economic Data Date Market Source Indicator Period Actual Consensus Previous 04/11 Italy ISTAT Industrial Production MoM February -0.60% -0.90% 1.70% 04/11 Italy ISTAT Industrial Production WDA YoY February 1.20% 1.40% 3.80% 04/11 Italy ISTAT Industrial Production NSA YoY February 5.20% – 0.60% 04/11 China National Bureau of Statistics CPI YoY March 2.30% 2.40% 2.30% 04/11 China National Bureau of Statistics PPI YoY March -4.30% -4.60% -4.90% 04/11 China National Bureau of Statistics Leading Index February 99.0 – 98.1 Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted) Overall Activity Buy %* Sell %* Net (QR) Qatari Individuals 53.50% 55.69% (8,170,453.69) Qatari Institutions 6.30% 12.04% (21,479,272.99) Qatari 59.80% 67.73% (29,649,726.68) GCC Individuals 1.87% 1.31% 2,087,638.39 GCC Institutions 4.67% 2.53% 8,010,135.71 GCC 6.54% 3.84% 10,097,774.10 Non-Qatari Individuals 22.99% 21.82% 4,366,155.12 Non-Qatari Institutions 10.67% 6.62% 15,185,797.46 Non-Qatari 33.66% 28.44% 19,551,952.58

- 3. Page 3 of 7 Earnings Calendar Tickers Company Name Date of reporting 1Q2016 results No. of days remaining Status QIGD Qatari Investors Group 12-Apr-16 0 Due QIBK Qatar Islamic Bank 13-Apr-16 1 Due DHBK Doha Bank 18-Apr-16 6 Due CBQK Commercial Bank 19-Apr-16 7 Due KCBK Al Khaliji 19-Apr-16 7 Due QEWS Qatar Electricity & Water Company 19-Apr-16 7 Due QATI Qatar Insurance Company 19-Apr-16 7 Due MARK Masraf Al Rayan 19-Apr-16 7 Due MRDS Mazaya Qatar 19-Apr-16 7 Due QGTS Qatar Gas Transport Company (Nakilat) 19-Apr-16 7 Due DOHI Doha Insurance 20-Apr-16 8 Due QIMD Qatar Industrial Manufacturing Company 20-Apr-16 8 Due ABQK Al Ahli Bank 20-Apr-16 8 Due MCCS Mannai Corp. 20-Apr-16 8 Due GWCS Gulf Warehousing Company 20-Apr-16 8 Due MCGS Medicare Group 20-Apr-16 8 Due QNNS Qatar Navigation (Milaha) 23-Apr-16 11 Due QCFS Qatar Cinema & Film Distribution Company 24-Apr-16 12 Due UDCD United Development Company 25-Apr-16 13 Due QOIS Qatar & Oman Investment 25-Apr-16 13 Due QFLS Qatar Fuel Company 26-Apr-16 14 Due ORDS Ooredoo 27-Apr-16 15 Due QGRI Qatar General Insurance & Reinsurance 27-Apr-16 15 Due MERS Al Meera Consumer Goods Company 27-Apr-16 15 Due AHCS Aamal Company 28-Apr-16 16 Due ERES Ezdan Real Estate Company 28-Apr-16 16 Due Source: QSE

- 4. Page 4 of 7 News Qatar ERES plans to raise $2bn Sukuk to finance real estate “mega projects” – Ezdan Holding Group (ERES) CEO Ali al-Obaidli said that the company is planning to raise a $2bn Sukuk to finance “mega projects” in the real estate sector as part of its strategy in investment diversification. Ezdan received the green signal during its ordinary and extraordinary general assembly, which approved the issuance of Shariah- compliant bonds worth $2bn and endorsed the board’s recommendation to distribute 5% cash dividends to shareholders at the rate of Dh50 per share. Ali al- Obaidli also said, “We have now received the approval from the board and plan to raise the funds in stages. The first stage will involve $500mn, which we plan to raise by May or June this year.” He added “The use of the remaining funds will depend on our spending. Maybe by the end of 2016 we may use part of it and the rest will depend on the progress of our projects. The $500mn will be used to finance Ezdan’s current real estate development projects.” (Gulf-Times.com) QSE suspends trading of QIGD shares on April 12 – The Qatar Stock Exchange (QSE) suspended trading of Qatari Investors Group’s (QIGD) shares on April 12, 2016 due to its EGM being held on that day. (QSE) QISI ratifies 40% cash dividends – Qatar Islamic Insurance Company (QISI), in its Annual General Meeting (AGM), approved all items on agenda, including the board’s proposal to distribute cash dividends of 40% of the paid-up capital (QR4 per share) for FY2015. (Peninsula Qatar) CI affirms QIBK ratings; outlook stable – Capital Intelligence Ratings (CI), a global credit rating agency, affirmed Qatar Islamic Bank’s (QIBK) financial strength rating (FSR) at ‘A’ and long- and short-term foreign currency ratings at ‘A’ and ‘A2’, respectively. The ratings reflect the QIBK’s intrinsic financial profile, the robust growth potential of the economy and ongoing government support for all Qatari banks. Based on the strength of the Qatari government balance sheet, the support rating is affirmed at ‘2’. Although the outlook on all ratings is maintained at “Stable”, CI said this is beginning to come under considerable pressure due to tight liquidity. The FSR is not only supported by good asset quality, still good profitability, and a more-than-satisfactory total capital adequacy ratio but also by its leadership role in the Islamic banking, which is growing faster than the conventional ones domestically. (Gulf-Times.com) CEO: CI rating affirmation reflects on QIIK’s strong initiatives – Qatar International Islamic Bank (QIIK) CEO Abdulbasit Ahmed al- Shaibei said that the rating affirmation from Capital Intelligence (CI) “reflects the strong initiatives made by the bank and the systematic and continuous implementation” of the interim and strategic plans approved by its Board of Directors. Al-Shaibei said it also reflects on the “maximum efforts” made by QIIK for taking advantage of low-risk opportunities, both internally and externally. Recently, Capital Intelligence Ratings confirmed QIIK’s financial strength rating at ‘A-‘ with a positive outlook. It also affirmed the bank’s long- and short-term foreign currency ratings at ‘A’ and ‘A2’, respectively, clearly indicating the bank’s strong position and credit worthiness. On the grounds of the QIIB rating affirmation, CI said the bank maintained the profitability level of the operational activities and its high quality assets, as well as high levels of liquidity; in addition to maintaining the capital adequacy at a good level and working to its enhancement through the issuance of capital instruments eligible under the first tranche of the capital. (Gulf-Times.com) Q-Post launches new e-commerce service – To cash in on the growing e-commerce market across the world, Qatar Postal Services Company (Q-Post) launched its new service “Connected by Qatar Post”. The formal launch of the international parcel forwarding service was announced at the Arab Future Cities Summit in the presence of HE the Transport and Communication Minister Jassim Saif Ahmed al-Sulaiti. Speaking on the occasion, Q- Post Chairman and Managing Director Faleh al-Naiemi expressed the hope that the country’s residents would avail the services of the new platform developed by the postal corporation while placing orders for their ever growing requirements from such markets as the US and the UK. Within a couple of weeks, the e- commerce platform will also cover Japan, China, and Germany. More countries are to be added to the network later. (Gulf- Times.com) Booz Allen: Around 19% of current retail payments in Qatar made digitally – According to a report by global consulting and technology firm Booz Allen Hamilton, nearly 19% of the current retail payments by value in Qatar are made digitally, compared with 72% in the UK and 90% in Sweden. The report noted that Middle East and North Africa (MENA) countries have the opportunity to double or triple adoption of digital payments. A modern payment infrastructure has the potential to create new and sustainable revenue streams for commercial banks in the region. The report, titled “Doubling Digital Payments in Mena,” recommends that in the face of a slowing global economy, regional central banks adopt a more strategic approach to regulatory policy making in order to realize the full potential of the digital economy in the MENA region. (Gulf-Times.com) CRA to launch new domain ‘.doha’ for city entities, organizations – Communications Regulatory Authority (CRA) to launch “.doha” as a new top-level domain (TLD) for eligible entities and organizations in the city to register their websites. This comes as part of CRA’s strategy to foster the development of Qatar’s domain extensions as a key public resource, by providing stable, secure, and trusted domain name services, as a priority in helping shape the country’s role in the digital economy. (Gulf-Times.com) Canon Solutions opens direct operation in Qatar – Canon Middle East, a leader in imaging solutions, held the official inauguration of its direct operation Canon Office Imaging Solutions (Doha) and the launch of its first dedicated business solutions showroom. This is the first time a global technology brand has set up a direct in- country presence in Qatar, Canon Middle East claimed in a statement. Canon Office Imaging Solutions (Doha) has been established in partnership with Salam Technology, Canon’s longstanding imaging solutions distribution partner in Qatar. (Gulf-Times.com) International UK consumers slow their spending in March – According to two surveys, British consumers reined in their spending last month, which added to signs of a slowdown in the country’s economy. The British Retail Consortium (BRC) said retail sales failed to grow for the first time in nearly a year in March as the Easter holiday hit food sales because many supermarkets were closed on Easter Sunday. The BRC’s figures are not seasonally adjusted. Food sales over the last three months fell by 0.7%, their biggest decline since June 2015. However, at the same time the holiday provided a boost to sales of furniture. Shoppers typically splash out on big-ticket items in the days after Easter. BRC CEO Helen Dickinson said the numbers were “relatively disappointing”. She said they also suggested that consumers were spending more money online rather than at shops and on leisure and entertainment, which do not feature in the retail sales numbers. On a like-for-like basis, stripping out changes in the amount of retail space open to shoppers over the past 12 months, sales fell by 0.7% in March,

- 5. Page 5 of 7 their worst performance since August 2015. British households have been the main engine of the country’s economic recovery, which began in 2013, helped by near-zero inflation, falling unemployment and gradually rising pay. However, consumer confidence has weakened recently, possibly reflecting concerns about the global economy and Britain’s referendum on its membership of the European Union, which is due to take place on June 23. (Reuters) German economy gained pace at start of year – The Economy Ministry said Germany’s economy has picked up pace at the start of 2016, driven by the domestic economy, while the foreign trade environment remains subdued. (Reuters) Japan machinery orders fall, strong yen clouds outlook – Cabinet Office data has revealed that Japan’s core machinery orders fell less than expected in February in a sign that capital expenditure is starting to stabilize, but a strong yen, which can hurt corporate earnings, clouds the outlook. The 9.2% monthly decline in core orders, a highly volatile data series regarded as a leading indicator of capital spending in the coming six to nine months, was less than economists’ median estimate for a 12.4% MoM fall. Japan’s policymakers are counting on capital expenditure to create more jobs and raise wages. However, if recent gains in the yen continue, companies could curb investment plans on worries that corporate profits will fall. Orders from manufacturers fell 30.6% MoM, which was the largest decline on record. Orders from the services sector rose 10.2%, marking the biggest increase since September. In January, core machinery orders jumped 15.0% MoM, the biggest gain since January 2003, due to large orders from the steel industry. The Cabinet Office said machinery orders are showing signs of picking up, unchanged from its assessment last month. The yen has gained more than 10% against dollar in 2016, as investors seek the currency as a safe haven. A rising yen tends to worry Japanese companies because it lowers exporters’ earnings. (Reuters) BOJ: Japan households’ inflation expectations hit three-year low – According to a central bank survey, Japanese households’ sentiment worsened in the three months to March and their expectations of inflation fell to levels before the Bank of Japan (BOJ) deployed its massive asset-buying program three years ago. The survey’s bleaker outlook keeps alive expectations of additional monetary stimulus even as BOJ Governor Haruhiko Kuroda maintained his optimism that the world’s third-largest economy was recovering moderately. Kuroda, however, warned that he was closely watching how a recent surge in the yen and slumping Tokyo stock prices could affect the outlook. Kuroda said, “Global financial markets remain unstable as investors are becoming increasingly risk averse due to uncertainty over the outlook of emerging and resource-exporting economies.” He said, “The BOJ will not hesitate to take additional easing steps if needed to achieve its inflation target.” The BOJ’s quarterly survey on people’s livelihood showed the ratio of households who expect prices to rise a year from now stood at 75.7% in March, down from 77.6% in December and the lowest level since March 2013. The survey showed eighty percent of the total number of households surveyed expects inflation to pick up five years from now, down slightly from December. That level was the lowest since December 2012. A separate index measuring households’ confidence about the economy stood at minus 22.5 in March, worsening from minus 17.3 in December to the lowest level since March 2015. The gloomy outcome underscores the dilemma the BOJ faces as it battles mounting external headwinds for the economy with its dwindling policy tool-kit. (Reuters) Premier: China economy shows positive signs but pressure lingers – Premier Li Keqiang has said that China’s economy has showed more positive signs but downward pressures still persisted, vowing to take steps to deal with overcapacity. The government will push forward “supply-side reforms”, while keeping economic growth within a reasonable range. Li said, “There are more positive factors in economic operations, but the downward pressure remains relatively big.” “We cannot ignore risks in some sectors.” Li said the government would ensure the launch of investment projects in a timely manner to help underpin growth. The government will quicken reforms to eliminate outdated capacity in coal and steel sectors and use “market-based” debt-to- equity swaps to help lower firms’ debt levels. China’s economy has seen positive changes since the start of this year. Li said last week China’s economic indicators showed signs of improvement in the 1Q2016. The government is due to release key economic data, including 1Q2016 economic growth, next week. China’s economic growth slowed to 6.8% in the 4Q2015, its weakest since the financial crisis that began in 2007 and 2008. (Reuters) Russian Central bank says 1Q2016 current account surplus at $11.7bn – According to the Central Bank, Russia’s current account surplus was worth an estimated $11.7bn in the 1Q2016. The estimated net capital outflow in 1Q2016 was $7bn. (Reuters) Regional Banque Saudi Fransi net profit up by 2.67% YoY in 1Q2016 – Banque Saudi Fransi has reported net profit of SR1.08bn in 1Q2016 as compared to SR1.05bn in 1Q2015, representing an increase of 2.67% YoY. The total assets of the bank stood at SR184.02bn at the end of March 31, 2016 as compared to SR193.88bn on March 31, 2015. Loans & advances reached SR124.98bn, while customer’s deposits stood at SR141.82bn. EPS amounted to SR0.89 in 1Q2016 versus SR0.87 in 1Q2015. (Tadawul) Alinma Bank net profit surges 13.66% YoY in 1Q2016 – Alinma Bank has reported net profit of SR391mn in 1Q2016 as compared to SR344mn in 1Q2015, representing an increase of 13.66% YoY. The total assets of the bank stood at SR91.61bn at the end of March 31, 2016 as compared to SR83.69bn on March 31, 2015. Loans & advances reached SR60.25bn, while customer’s deposits stood at SR68.79bn. EPS amounted to SR0.26 in 1Q2016 versus SR0.23 in 1Q2015. (Tadawul) Buruj Cooperative Insurance announces renewal of insurance license – The Saudi Arabian Monetary Agency (SAMA) has renewed Buruj Cooperative Insurance Company’s insurance license in General and Health insurance starting from March 23, 2016 for three years till February 18, 2019. (Tadawul) Saudi Real Estate OGM approves 5% dividend – Saudi Real Estate Company’s ordinary general assembly meeting (OGM) has approved distribution of 5% dividend (SR 5 per share) amounting to SR60mn for 2H2015. Shareholders registered in Tadawul records at the end of the trading day on which the assembly is held will be eligible for dividend distribution. (Tadawul) Saudi Arabia to supply Egypt with 700,000 tons of petroleum products a month – According to an Egyptian General Petroleum Corp (EGPC) official, Saudi Arabia will provide Egypt with 700,000 tons of petroleum products a month under a five-year $23bn deal between Saudi Aramco and EGPC. Under the 700,000 tons monthly supply deal, Saudi Aramco will provide Egypt with 400,000 tons of gas oil, 200,000 tons of benzene and 100,000 tons of Mazut. The financing for the petroleum and petroleum products will have an interest rate of 2% and will be repaid over 15 years. (Reuters) IPIC denies any links with BVI-incorporated firm linked to Malaysia's 1MDB – International Petroleum Investment Company (IPIC) said neither itself nor its unit Aabar Investments have any links to a British Virgin Islands-incorporated firm named in a report into the troubles at Malaysian state fund 1MDB. Both IPIC and Aabar have confirmed that Aabar BVI was not an entity within

- 6. Page 6 of 7 either corporate group. Further, both IPIC and Aabar have confirmed that neither has received any payments from Aabar BVI nor has IPIC or Aabar assumed any liabilities on behalf of Aabar BVI. (Reuters) Etihad Etisalat, Bayanat Al Oula sign agreement with Japan’s NEC – Etihad Etisalat Company and Bayanat Al Oula have signed an agreement with Japan’s NEC for provision of network managed services for the upcoming three years. The agreement represents an expansion in the scope of work between the two parties. Accordingly, NEC will provide the network managed services for (Microwave-PTP) networks as business solutions reflected in the control and management of daily operations, corrective actions, and preventive maintenance, and improving the operating system, as well as keeping pace with the latest developments of the system. (GulfBase.com) KHI sells 100% stake in InterContinental Hotel Lusaka – Kingdom Hotel Investments (KHI), a subsidiary of Kingdom Holding Company (KHC), has sold its 100% interest in the InterContinental Hotel Lusaka to QG Africa Hotel LP, a Mauritius-based fund managed by QG Investments Africa Management, for a gross consideration of $35.9mn. (GulfBase.com) Saudi Kayan Petrochemical restarts ethylene glycol/oxide ethylene plant – Saudi Kayan Petrochemical Company has restarted a plant that produces ethylene glycol and oxide ethylene after scheduled maintenance and some technical repairs. The affiliate of Saudi Basic Industries Corporation (SABIC) had said in January 2016 that it would shut the plant down on March 1 for 48 days, having initially postponed the work from last October. (GulfBase.com) KSA might increase $8bn sovereign loan – According to sources, Saudi Arabia has attracted substantial demand for its first foreign borrowing in more than a decade, and is likely to increase the size of the loan. Reportedly, the Kingdom asked banks for a loan worth between $6-8bn that would run for five years, as the Kingdom seeks to plug a record budget deficit caused by low oil prices. (GulfBase.com) Morgan Stanley hires Motaz Alangari as KSA investment banking head – According to Reuters, Morgan Stanley has appointed Motaz Alangari as its investment banking head for Saudi Arabia. Motaz joins the US bank from Samba Capital, the investment banking arm of Samba Financial Group. (Reuters) DPR secures AED993mn in syndicated debt financing – Dubai Parks and Resorts (DPR) has secured AED993mn of debt financing to fund part of the proposed Six Flags branded theme park, which would further enhance the DPR destination offering. The debt portion accounts for approximately 37% of the total financing being raised. Earlier, on March 28, 2016, the company announced that it is seeking to raise AED 2.67 billion primarily to finance the development of Six Flags Dubai, through a combination of debt and equity funding. The debt funding is being provided by Abu Dhabi Commercial Bank, Dubai Islamic Bank, and Sharjah Islamic Bank. Six Flags Dubai is expected to open in 4Q2019. (DFM) Emirates NBD: Dubai private sector output rebounds in March – According to the Emirates NBD Dubai Economy Tracker Index, the private sector economy in Dubai, UAE signaled a solid rebound in business conditions during March 2016, following the slight deterioration recorded during February 2016. The seasonally adjusted index, a composite indicator designed to give an accurate overview of operating conditions in the non-oil private sector economy rose to 52.5 in March 2016, up from 48.9 in February 2016. Moreover, the latest reading pointed to the fastest improvement in business conditions since November 2015, largely reflecting renewed output and new order growth alongside a slight acceleration in staff hiring. (GulfBase.com) MRE establishes new subsidiary – Manazel Real Estate (MRE) has announced the launch of Al Manzel, a new subsidiary responsible for managing and operating the company’s Dari initiative. Established to support UAE Nationals in 2012, Dari connects the recipients of governmental housing loans with consultants, qualified experts at Manazel, who oversee the new home’s construction from design to delivery. (ADX) Aldar launches AED6bn Yas Acres project – Aldar Properties Chairman Abo Bark Al-Khouri said that the company has launched the Yas Acres project with investments worth AED6bn. This golf and waterfront development, which will add 1315 villas to Yas Island, is one of the most significant new residential developments to be launched in Abu Dhabi by Aldar. (ADX) IPIC in talks with banks for potential bond sale – According to sources, International Petroleum Investment Company (IPIC) is in talks with banks over issuing a bond denominated in euros. The company is talking to the nine banks that backed a €3.6bn euro loan issued on behalf of its subsidiary Aabar Investments in March 2016 about the new bond issue. The proceeds of the potential bond will be used to refinance an upcoming maturity. IPIC has a €1.25bn bond that was originally sold in 2011 and falls due in mid- May 2016. (Reuters) Emirates Driving AGM approves 30% cash dividend – Emirates Driving Company’s general assembly meeting (AGM) has approved the board of directors’ (BoD) proposal to distribute 30% cash dividend from the paid-up capital for the year ended December 31, 2015. (ADX) Cluttons: Abu Dhabi sees big demand for affordable housing – According to Cluttons’ Abu Dhabi Spring 2016 Property Market Outlook report, the downward readjustment of housing allowances among companies in Abu Dhabi is creating further strain on the higher end of the residential market and underscores the need to address the UAE capital’s lack of affordable housing options. The shrinking pool of high-end management level tenants in the oil & gas sector in particular, has meant rising void periods for properties at the higher end of the rental spectrum and increased demand for more affordable options. (GulfBase.com) Pembina Pipeline, PIC evaluate world-scale integrated polypropylene facility in Alberta – Pembina Pipeline Corporation and Kuwait's PIC have evaluated the world-scale integrated polypropylene facility in Alberta. The project could consume approximately 35,000 barrels per day (bpd) of propane and could produce up to 800,000 metric tons per year of polypropylene. Polypropylene would be transported in a pellet form to markets across North America and internationally. The final investment decision is expected to be made by middle of 2017. Subject to regulatory, environmental and Pembina's BoD’s approval, the project is expected to be in service by 2020. (Reuters)

- 7. Contacts Saugata Sarkar Shahan Keushgerian Zaid al-Nafoosi, CMT, CFTe Head of Research Senior Research Analyst Senior Research Analyst Tel: (+974) 4476 6534 Tel: (+974) 4476 6509 Tel: (+974) 4476 6535 saugata.sarkar@qnbfs.com.qa shahan.keushgerian@qnbfs.com.qa zaid.alnafoosi@qnbfs.com.qa ` QNB Financial Services SPC Contact Center: (+974) 4476 6666 PO Box 24025 Doha, Qatar Disclaimer and Copyright Notice: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of QNB SAQ (“QNB”). QNBFS is regulated by the Qatar Financial Markets Authority and the Qatar Exchange QNB SAQ is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. QNBFS accepts no liability whatsoever for any direct or indirect losses arising from use of this report. Any investment decision should depend on the individual circumstances of the investor and be based on specifically engaged investment advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. For reports dealing with Technical Analysis, expressed opinions and/or recommendations may be different or contrary to the opinions/recommendations of QNBFS Fundamental Research as a result of depending solely on the historical technical data (price and volume). QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the views and opinions included in this report. This report may not be reproduced in whole or in part without permission from QNBFS COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS. Page 7 of 7 Rebased Performance Daily Index Performance Source: Bloomberg Source: Bloomberg Source: Bloomberg Source: Bloomberg (*$ adjusted returns) 80.0 100.0 120.0 140.0 160.0 180.0 Mar-12 Mar-13 Mar-14 Mar-15 Mar-16 QSE In d e x S&P Pa n Ara b S&P GCC (0.5%) 0.3% 0.6% (0.2%) 0.5% 0.2% (0.3%) (1.0%) (0.5%) 0.0% 0.5% 1.0% SaudiArabia Qatar Kuwait Bahrain Oman AbuDhabi Dubai Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D%* WTD%* YTD%* Gold/Ounce 1,257.90 1.5 1.5 18.5 MSCI World Index 1,632.14 (0.0) (0.0) (1.8) Silver/Ounce 15.93 3.6 3.6 14.9 DJ Industrial 17,556.41 (0.1) (0.1) 0.8 Crude Oil (Brent)/Barrel (FM Future) 42.83 2.1 2.1 14.9 S&P 500 2,041.99 (0.3) (0.3) (0.1) Crude Oil (WTI)/Barrel (FM Future) 40.36 1.6 1.6 9.0 NASDAQ 100 4,833.40 (0.4) (0.4) (3.5) Natural Gas (Henry Hub)/MMBtu 1.88 (5.3) (5.3) (18.7) STOXX 600 332.87 0.4 0.4 (4.4) LPG Propane (Arab Gulf)/Ton 45.38 2.0 2.0 16.0 DAX 9,682.99 0.7 0.7 (5.7) LPG Butane (Arab Gulf)/Ton 53.00 1.0 1.0 (7.8) FTSE 100 6,200.12 0.8 0.8 (4.0) Euro 1.14 0.1 0.1 5.0 CAC 40 4,312.63 0.3 0.3 (2.3) Yen 107.94 (0.1) (0.1) (10.2) Nikkei 15,751.13 (0.1) (0.1) (7.6) GBP 1.42 0.8 0.8 (3.4) MSCI EM 824.01 0.9 0.9 3.8 CHF 1.05 (0.1) (0.1) 5.0 SHANGHAI SE Composite 3,033.96 1.8 1.8 (13.9) AUD 0.76 0.5 0.5 4.2 HANG SENG 20,440.81 0.4 0.4 (6.8) USD Index 93.95 (0.3) (0.3) (4.7) BSE SENSEX 25,022.16 2.2 2.2 (4.3) RUB 66.69 (0.6) (0.6) (8.0) Bovespa 50,165.47 2.6 2.6 29.8 BRL 0.29 2.7 2.7 13.4 RTS 900.98 2.5 2.5 19.0 116.2 91.3 89.4