Andheri Call Girls In 9825968104 Mumbai Hot Models

5 November Daily Market Report

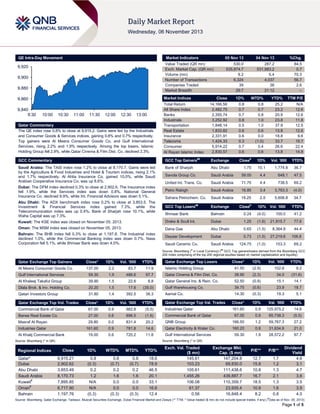

1. QE Intra-Day Movement

Market Indicators

9,920

9,900

9,880

04 Nov 13

%Chg.

530.0

535,874.7

9.2

6,324

39

29:7

287.2

531,983.2

5.4

4,037

38

21:12

84.5

0.7

70.3

56.7

2.6

–

Market Indices

9,860

9,840

9:30

05 Nov 13

Value Traded (QR mn)

Exch. Market Cap. (QR mn)

Volume (mn)

Number of Transactions

Companies Traded

Market Breadth

10:00

10:30

11:00

11:30

12:00

12:30

13:00

Qatar Commentary

The QE index rose 0.8% to close at 9,915.2. Gains were led by the Industrials

and Consumer Goods & Services indices, gaining 0.8% and 0.7% respectively.

Top gainers were Al Meera Consumer Goods Co. and Gulf International

Services, rising 2.2% and 1.9% respectively. Among the top losers, Islamic

Holding Group fell 2.9%, while Qatar Cinema & Film Dist. Co. declined 2.3%.

Close

Total Return

All Share Index

Banks

Industrials

Transportation

Real Estate

Insurance

Telecoms

Consumer

Al Rayan Islamic Index

1D%

WTD%

YTD%

TTM P/E

14,166.56

2,482.75

2,355.74

3,252.92

1,848.14

1,833.82

2,331.91

1,424.33

5,914.22

2,830.57

0.8

0.7

0.7

0.8

0.5

0.6

0.6

0.3

0.7

0.6

0.8

0.7

0.8

1.0

1.0

0.6

0.0

(1.0)

0.4

0.6

25.2

23.2

20.9

23.8

37.9

13.8

18.8

33.7

26.6

13.8

N/A

12.6

12.6

11.8

12.5

12.6

9.6

19.7

22.4

14.8

GCC Commentary

GCC Top Gainers##

Exchange

Close#

1D%

Saudi Arabia: The TASI index rose 1.2% to close at 8,170.7. Gains were led

by the Agriculture & Food Industries and Hotel & Tourism indices, rising 2.1%

and 1.7% respectively. Al Ahlia Insurance Co. gained 10.0%, while Saudi

Arabian Cooperative Insurance Co. was up 8.6%.

Bank of Sharjah

Abu Dhabi

1.75

10.1

1,774.8

36.7

Savola Group Co.

Saudi Arabia

59.00

4.4

648.1

47.5

United Int. Trans. Co.

Saudi Arabia

71.75

4.4

738.5

69.2

Petro Rabigh

Saudi Arabia

16.85

3.4

3,763.3

(4.0)

Saudi Arabia

18.25

2.5

5,606.8

34.7

Dubai: The DFM index declined 0.3% to close at 2,902.6. The Insurance index

fell 1.9%, while the Services index was down 0.8%. National General

Insurance Co. declined 9.9%, while Int. Financial Advisors was down 5.1%.

Abu Dhabi: The ADX benchmark index rose 0.2% to close at 3,853.5. The

Investment & Financial Services index gained 7.3%, while the

Telecommunication index was up 0.4%. Bank of Sharjah rose 10.1%, while

Waha Capital was up 7.3%.

Sahara Petrochem. Co.

##

#

1D% Vol. ‘000

YTD%

GCC Top Losers

Exchange

Ithmaar Bank

Bahrain

0.24

(4.0)

100.0

41.2

Kuwait: The KSE index was closed on November 05, 2013.

Drake & Scull Int.

Dubai

1.25

(1.6)

21,815.7

77.6

Oman: The MSM index was closed on November 05, 2013.

Dana Gas

Abu Dhabi

0.65

(1.5)

8,364.8

44.4

Deyaar Development

Dubai

0.73

(1.5)

27,219.6

106.8

Saudi Ceramic Co.

Saudi Arabia

124.75

(1.0)

153.3

69.2

Bahrain: The BHB index fell 0.3% to close at 1,197.8. The Industrial index

declined 1.0%, while the Commercial Banking index was down 0.7%. Nass

Corporation fell 5.1%, while Ithmaar Bank was down 4.0%.

Close

Vol. ‘000

YTD%

Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

Qatar Exchange Top Gainers

Close*

1D%

Vol. ‘000

YTD%

Close*

1D%

Vol. ‘000

Al Meera Consumer Goods Co.

137.00

2.2

83.7

11.9

Islamic Holding Group

41.50

(2.9)

102.8

9.2

38.90

(2.3)

34.0

(31.6)

Qatar Exchange Top Losers

YTD%

Gulf International Services

59.30

1.9

486.6

97.7

Qatar Cinema & Film Dist. Co.

Al Khaleej Takaful Group

39.90

1.5

22.6

8.8

Qatar General Ins. & Rein. Co.

52.50

(0.9)

15.1

14.1

Dlala Brok. & Inv. Holding Co.

20.20

1.5

17.6

(35.0)

Gulf Warehousing Co.

39.75

(0.6)

23.9

18.7

Qatari Investors Group

31.80

1.4

392.5

38.3

Aamal Co.

14.30

(0.3)

19.3

5.1

YTD%

Close*

1D%

Vol. ‘000

YTD%

Qatar Exchange Top Val. Trades

Close*

1D%

Val. ‘000

Commercial Bank of Qatar

67.00

0.9

982.8

(5.5)

Industries Qatar

161.60

0.9

125,975.2

14.6

Barwa Real Estate Co.

27.00

0.6

896.5

(1.6)

Commercial Bank of Qatar

67.00

0.9

65,738.3

(5.5)

Masraf Al Rayan

29.80

0.0

831.4

20.2

QNB Group

166.50

1.2

59,767.3

27.2

Industries Qatar

161.60

0.9

781.8

14.6

Qatar Electricity & Water Co.

160.20

0.8

31,634.9

21.0

19.00

0.6

720.2

11.8

Gulf International Services

59.30

1.9

28,572.2

97.7

Qatar Exchange Top Vol. Trades

Al Khalij Commercial Bank

Source: Bloomberg (* in QR)

Source: Bloomberg (* in QR)

Regional Indices

Qatar*

Dubai

Abu Dhabi

Saudi Arabia

Kuwait#

Oman#

Bahrain

Close

1D%

WTD%

MTD%

YTD%

9,915.21

2,902.62

3,853.49

8,170.73

7,895.85

6,717.90

1,197.76

0.8

(0.3)

0.2

1.2

N/A

N/A

(0.3)

0.8

(0.7)

0.2

1.6

0.0

0.0

(0.3)

0.8

(0.7)

0.2

1.6

0.0

0.0

(0.3)

18.6

78.9

46.5

20.1

33.1

16.6

12.4

Exch. Val. Traded

($ mn)

145.61

103.23

105.61

1,455.26

106.08

61.37

0.56

Exchange Mkt.

Cap. ($ mn)

147,204.8

69,830.0

111,438.6

439,887.7

110,359.7

23,935.4

16,848.4

P/E**

P/B**

12.7

15.8

10.8

16.7

18.5

10.9

8.2

1.7

1.2

1.3

2.1

1.3

1.6

0.8

Dividend

Yield

4.6

3.1

4.7

3.6

3.5

3.9

4.0

#

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any) ( Data as of Nov. 05, 2013)

Page 1 of 5

2. Qatar Market Commentary

The QE index rose 0.8% to close at 9,915.2. The Industrials and

Consumer Goods & Services indices led the gains. The index

rose on the back of buying support from non-Qatari shareholders

despite selling pressure from Qatari shareholders.

Al Meera Consumer Goods Co. and Gulf International Services

were the top gainers, rising 2.2% and 1.9% respectively. Among

the top losers, Islamic Holding Group fell 2.9%, while Qatar

Cinema & Film Dist. Co. declined 2.3%.

Overall Activity

Buy %*

Sell %*

Net (QR)

Qatari

48.92%

68.15%

(101,917,490.41)

Non-Qatari

51.08%

31.85%

101,917,490.41

Source: Qatar Exchange (* as a % of traded value)

Volume of shares traded on Tuesday rose by 70.3% to 9.2mn

from 5.4mn on Monday. Further, as compared to the 30-day

moving average of 6.2mn, volume for the day was 49.6% higher.

Commercial Bank of Qatar and Barwa Real Estate Co. were the

most active stocks, contributing 10.7% and 9.7% to the total

volume respectively.

Earnings and Global Economic Data

Earnings Releases

Company

Revenue

(mn) 3Q2013

% Change

YoY

Operating Profit

(mn) 3Q2013

% Change

YoY

Net Profit (mn)

3Q2013

% Change

YoY

123.4

223.6%

–

–

82.8

NA

AED

19.1

-33.9%

–

–

7.5

57.7%

AED

107.5

20.6%

–

–

20.4

-0.1%

AED

73.7

42.3%

–

–

3.0

-81.8%

Market

Dubai Financial Market Co.

(DFM)

FOODCO Holding

Gulf Medical Projects Co.

(GMPC)

Emirates Insurance Co.

(EIC)

Currency

Dubai

AED

Abu Dhabi

Abu Dhabi

Abu Dhabi

Source: Company data, DFM, ADX, MSM

Global Economic Data

Date

Market

Source

Indicator

Period

Actual

Consensus

Previous

11/05

US

ISM

ISM Non-Manf. Composite

October

55.4

54

54.4

11/05

EU

Eurostat

PPI MoM

September

0.10%

0.20%

0.00%

11/05

EU

Eurostat

PPI YoY

September

-0.90%

-0.80%

-0.80%

11/05

China

HSBC

HSBC/Markit Services PMI

October

52.6

–

52.4

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

News

Qatar

Emir vows measures to contain price rise – The Emir HH

Sheikh Tamim bin Hamad al-Thani promised that the Qatari

government will seek to contain inflation through all possible

means, including monetary and fiscal policies. Speaking at the

opening of a new term of the Advisory Council, the Emir said a

governmental committee has been set up to propose solutions

to control inflationary pressures. The government will seek to

contain it (inflation) by all available means and tools, and, in

particular, through the monetary and fiscal policies, combating

monopoly, encouraging competitiveness, setting an appropriate

timetable to invest in major projects and co-ordinating between

these projects to avert being concentrated in a short period of

time leading to pressure on the available potential capacity.

(Gulf-Times.com)

QNB Group: Qatar’s foreign reserves up $39.3bn in

September – According to a report by the QNB Group, Qatar’s

international reserves have edged higher, totaling $39.3bn in

September, indicating 16% rise on 2012 driven by high

hydrocarbon prices. According to the QNB report, the import

cover stood at 16.7 months, which is well above the IMF

recommended level of three months for pegged exchange rates.

Qatar’s international reserves have been steadily rising over the

years as foreign exchange receipts from exports grew. The

pullback in reserves in 2011 was largely due to capital outflows

for purchasing foreign assets and international reserves are

forecasted to increase gradually until 2014. Strong fiscal and

economic fundamentals have reduced Qatar’s Credit Default

Swap (CDS) spreads to historic lows in October. Four major

Asian countries, Japan, South Korea, India and China, remained

the top export destinations for Qatar. (Gulf-Times.com)

BWI signs deal with Sphinex to develop Qatar hotels – Best

Western International (BWI), a major global hotel chain, has

signed a key agreement with Sphinex Hotels & Resorts, a Qatari

hotel development company, for the development of several

new hotels in Qatar. Initially, the Area Development Agreement

concluded between BWI and Sphinex Hotels & Resorts will

include a new-build 75-room property in Doha to be operated

under BWI’s midscale “Best Western” brand. The agreement

also paves the way for future developments, which could lead to

BWI becoming a leading international hotel operator in Qatar.

(Gulf-Times.com)

Qatar earmarks QR4bn for Industrial Area development –

Ashghal Director of Road Projects Department Saud Ali Al

Tamimi said the government has earmarked QR4bn for the

development of the Industrial Area in six phases. The first stage

will develop the old Industrial Area at a cost of QR1.3bn, which

is aimed to make the Industrial Area an integrated one with

modern infrastructure. (Peninsula Qatar)

Page 2 of 5

3. ERES to hold shareholders’ OGM on November 20 – Ezdan

Holding Group (ERES) will hold its shareholders’ ordinary

general meeting (OGM) on November 20, 2013 to discuss the

board’s recommendation to enter into a partnership with Sak

Holding Group for developing its land. (QE)

International

EU expects sluggish growth, persistent high unemployment

– The European Union (EU) expects subdued growth is likely to

keep the bloc's unemployment rate near record highs through

2015, as private-sector debt-cutting and government austerity

measures continue to weigh on consumer spending and

business investment. The European Commission's economists

predict that economic imbalances are at the root of the

Eurozone crisis, which is though diminished, will persist.

Economists downgraded their expectations for the Eurozone’s

growth next year to 1.1%, from the 1.2% forecast earlier in

spring. The forecast for 2015 stands at 1.7%. (WSJ)

ECB: Eurozone gradually recovering – The European Central

Bank President Mario Draghi said the Eurozone economy is

recovering gradually, but the interest rates paid by households

and businesses across the bloc continue to vary greatly. Draghi

also said he expected Europe's proposed banking union, if

properly implemented, can improve the situation across the

currency bloc. (Reuters)

BoJ offers upbeat view on China, US despite risks – The

Bank of Japan (BoJ) Governor Haruhiko Kuroda said the

economies of China and the US – Japan's biggest export

markets – will continue to recover and help achieve the central

bank's 2% inflation target. Kuroda said Japan’s economy is

making steady progress toward meeting the BoJ's price goal,

but reiterated his readiness to offer additional monetary stimulus

if that path is threatened by external risks. (Reuters)

Regional

Saudi PMI declines to 56.7 in October – The seasonallyadjusted Saudi Arabian Purchasing Managers’ Index (PMI)

compiled by the Saudi British Bank (SABB) and HSBC declined

to 56.7 in October 2013 from 58.7 in September. The output

growth for non-oil private sector companies stood at 58.2, which

is the second slowest in the survey's 51-month history.

However, new orders have increased in October to 64.7, but at

the slowest pace in three months. (GulfBase.com)

RCJY awards 2 infrastructure contracts worth SR300mn –

The Royal Commission for Jubail & Yanbu (RCJY) has signed

two contracts worth SR300mn to develop infrastructure of

Mardooma Quarter and implement engineering services for

energy & telecommunications in Ras Al Khair. RCJY has signed

a contract with Al Harbi Trading & Contracting Company to

develop 500 hectares of land in Mardooma Quarter, which is

expected to be completed in 26 months. Meanwhile, the

Egyptian Group along with Lahmeyer International Company

has won a contract from RCJY to implement planning, designing

and installing engineering services for high voltage electrical

substations, including power distribution networks and

telecommunications in Ras Al Khair. (GulfBase.com)

JEC signs SR162mn deal with EC Harris Mace to manage

Kingdom Tower project – Jeddah Economic Company (JEC)

has entered into an agreement worth SR162mn with EC Harris

Mace to provide project management services for the Kingdom

Tower project. This contract includes the management of all

aspects of project delivery with specific emphasis on

management of programs and costs. (Tadawul)

KAEC awards SR313mn construction contract to Rezaik Al

Jedrawi – The King Abdullah Economic City (KAEC) has

awarded SR313mn contract to Rezaik Al Jedrawi Company to

construct the Phase 1 of Al Waha residential community. This

180,000 square meter space consists of 650 units that offer

single and multi-family housing solutions. The sales and preleasing will begin in 2014, while the customer handover is

scheduled for 4Q2015. (GulfBase.com)

Savola’s shareholders approve SR5.3bn capital increase –

Savola Group Company’s shareholders have approved to

increase the company’s capital from SR5bn to SR5.34bn by

issuing 33.98mn new shares to Al Muhaidib Holding Company.

This will be done in exchange of acquiring 10% shareholding in

Savola and 18.6% stake in Al Azizia Panda United Company.

(Tadawul)

Saudi CMA approves Bawan’s 15mn shares IPO – The Saudi

Capital Market Authority (Saudi CMA) has approved the initial

public offering of 15mn shares of Bawan Holding Company,

representing 30% of the company’s share capital. A portion of

these shares will be allotted to mutual funds and authorized

persons. Shares will be offered from November 27 to December

3, 2013. (Tadawul)

Astra Food’s IPO of 11mn shares approved – The Saudi

CMA has approved the initial public offering of 11mn shares of

Astra Food Company, which represents 40% of the company’s

share capital. A portion of these shares will be allocated to

mutual funds and authorized persons. Shares will be offered

from December 18 to December 24, 2013. (Tadawul)

Saudi CMA authorizes Mulkia Investment as principal

underwriter – The Saudi CMA’s Board of Commissioners has

authorized Mulkia Investment Company as the principal,

underwriter, for managing investment funds and client portfolios,

as well as arranging, advising and custody in the securities

businesses. (Tadawul)

JMC’s BoD recommends to 50% capital increase – Jarir

Marketing Company’s (JMC) Board of Directors has

recommended a 50% increase in the company’s capital from

SR600mn to SR900mn. (GulfBase.com)

UAE PMI declines to 56.3 points in October – The HSBC

UAE PMI declined to 56.3 points in October 2013 from 56.6

points in September. Firms in the UAE have seen their output

growth to fall to 56.4 in October from 57.9 in September. New

orders were strongest in the survey's 51-month history standing

at 64.6 in October as compared to 65 in September. Growth in

new export orders rose to 58.9 points. However, employment

creation across the UAE's non-oil private sector has slowed

moderately to 52.7 points in October. Output price growth has

slipped into negative territory at 49 points in October, while input

price growth slowed slightly to 54.2 points in October.

(GulfBase.com)

Ras Al Khaimah seeks bids for 2 utility projects worth

$450mn – Ras Al Khaimah will undertake bidding for two utility

projects worth $450mn to meet the growing power demand and

enable new developers to participate in the development of

utility infrastructure. This initial power tender will be to supply 20

MW of solar power. The Emirate will also float a separate tender

for a water project that will supply approximately 22mn gallons

of water per day. (GulfBase.com)

Sharjah hotels report 10% growth in 9M2013 – According to

the data released by the Sharjah Commerce & Tourism

Development Authority (SCTDA), the Emirate’s hotel industry

has witnessed a robust 10% growth during January-September

2013. A total number of 1.4mn international tourists have visited

Page 3 of 5

4. Sharjah until September as compared to 1.3mn visitors during

January-September 2012. The data showed that Arab tourists

comprised 13% of the total figures, whereas Asian tourists

constituted 14%. SCTDA found that the total number of hotel

rooms has reached 9,573, which is expected to touch 12,000 by

2015. (GulfBase.com)

Etisalat inks share purchase deal with Vivendi to acquire

53% stake in Maroc Telecom – The Emirates

Telecommunications Corporation (Etisalat) has signed a share

purchase agreement for the acquisition of Vivendi’s 53% stake

in Itissalat Al Maghrib (Maroc Telecom) for €4.2bn in cash. The

cash transaction also includes 7.4 Moroccan Dirhams per share

paid by Maroc Telecom to the French company. The purchase

will give the UAE telecom operator control over the largest

carrier in Morocco. (ADX)

Thuraya Telecom signs partnership deal with Vocality –

Thuraya Telecommunications Company has entered into a

strategic partnership agreement with Vocality to provide

Vocality’s solutions for its global network of service partners that

serve commercial and defense satellite communication markets.

(GulfBase.com)

Empower in talks to buy Palm Utilities – Dubai-based

Empower (a unit of Dubai Electricity & Water Authority) is

reportedly in advanced talks to buy Palm Utilities (owned by

Dubai World) for about $500mn. Empower is trying to raise

around $600mn from six banks to fund the acquisition.

(Bloomberg)

JLL: Abu Dhabi home prices pick up due to 5% rise in

prices of prime properties – According to a report by Jones

Lang LaSalle (JLL), home prices in Abu Dhabi are picking up in

3Q2013 due to a 5% rise in prices of prime properties. JLL’s

Regional Director & Head of Abu Dhabi Office David Dudley

said that prime residential sales market has proved to be the

best performing segment in 2013, with a steady increase in

transaction volumes and QoQ growth in sales prices for prime

stock. The prime residential, rental, retail, hospitality and office

sectors have remained stable and are poised for recovery as

supply and demand of properties have become more balanced.

The report showed that short-term demand will be fuelled by

progress on major infrastructure projects such as the airport

expansion, Etihad Rail, Saadiyat Island museums and other

major infrastructure initiatives. However, the long-term market

recovery will be dependent on the government’s ongoing

initiatives to diversify the economy and generate sustainable

demand growth. The report also showed that prime residential

rents have remained unchanged in 3Q2013 at AED130, 000,

while secondary residential rents have continued to fall in

3Q2013. (GulfBase.com)

KFH inks MoU with Foulath to finance $115mn – The Kuwait

Finance House (KFH) has signed a MoU with Bahrain-based

Gulf United Steel Holding Company (Foulath) to finance $115mn

for five years. (GulfBase.com)

Oman’s revenue declines 4.2% to OMR10.48bn for 9M2013 –

According to a report released by the National Center for

Statistics & Information (NCSI), the Omani government's

revenue has declined 4.2% YoY to OMR10.48bn for the nine

months ended on September 30, 2013. This fall was mainly due

to decline in net oil revenue, which declined 2.5% to OMR7.9bn.

The report showed that crude oil production during JanuarySeptember 2013 rose 2.9% YoY to 256.5mn barrels, while the

average oil price fell 4.3% YoY to $104.87 per barrel. The

average daily production stood at 939,400 barrels per day (bpd)

during January-September 2013 as compared to 910,000 bpd

for the corresponding period in 2012. Moreover, the report

showed that Oman's gas revenue has declined 10.9% YoY to

OMR1.1bn, while custom duties stood at OMR139.1mn,

indicating a decrease of 18.6% YoY. (GulfBase.com)

Tilal Development issues OMR50mn sukuk – Tilal

Development Company has successfully issued OMR50mn

sukuk. This five-year sukuk offers a profit rate of 5% and was

privately placed with investors. The proceeds from this issue will

be used to expand Tilal Complex in Muscat. (Reuters)

Moody's: Bahrain's Baa2 rating supported by its surplus

BoPs, assistance from GCC members – According to

Moody's Investors Service, Bahrain's Baa2 rating is supported

by its surplus balance of payments and the financial assistance

received from the members of the GCC region. The key

constraint on Bahrain's creditworthiness is due to its unsettled

politics, which hold negative implications for its fiscal accounts

and future growth trajectory. (GulfBase.com)

Investcorp’s US-based arm acquires assets worth $250mn –

Bahrain-based Investcorp’s US-based real estate arm has

acquired a group of offices and retail assets worth $250mn in

Greater Chicago, Los Angeles, Minneapolis and New York

areas. These properties comprise more than 1.6mn square feet

of space and have a combined occupancy rate of around 92%.

(Bahrain Bourse)

appoints

new

CFO

–

The

Bahrain

Batelco

Telecommunications Company (Batelco) has appointed Faisal

Qamhiyah as the company’s new CFO. (Reuters)

FGB appoints banks to arrange dollar denominated bond

sale – First Gulf Bank (FGB) is planning to sell a US dollardenominated, benchmark-sized bond. The bank has appointed

the Bank of America Merrill Lynch, Citigroup, Deutsche Bank

and HSBC Holdings to arrange the bond sale, which is expected

to raise $500mn. The initial price thought for this issue is 185

basis points over mid-swaps with maturity in January 2019.

(Reuters)

Habtoor Leighton bags $160mn contract from ADAC –

Habtoor Leighton Group (HLG) has signed a new contract with

Abu Dhabi Airport Company (ADAC) worth $160mn. HLG will

install supporting infrastructure, build roads and bridges and

carry out electrical & plumbing work. The company will begin its

work in November and expects to complete within 18 to 24

months. (Bloomberg)

Page 4 of 5

5. Rebased Performance

Daily Index Performance

150.0

1.4%

140.0

1.2%

142.5

130.0

128.2

120.0

0.8%

0.7%

0.2%

0.0%

116.9

110.0

0.0%

0.0%

100.0

90.0

S&P Pan Arab

S&P GCC

Source: Bloomberg

Asset/Currency Performance

Dubai

Oman*

Bahrain

Jul-13

Kuwait*

May-12 Dec-12

Abu Dhabi

QE Index

Oct-11

Qatar

Jan-10 Aug-10 Mar-11

(0.3%)

(0.3%)

Saudi Arabia

(0.7%)

80.0

Source: Bloomberg (*- Kuwait, Oman were closed on November 05, 2013)

Close

1D%

WTD%

YTD%

15,618.22

(0.1)

0.0

19.2

S&P 500

1,762.97

(0.3)

0.1

23.6

(5.2)

NASDAQ 100

3,939.86

0.1

0.5

30.5

(2.8)

(1.9)

STOXX 600

321.89

(0.2)

0.1

15.1

(0.1)

0.4

30.4

DAX

9,009.11

(0.3)

0.0

18.3

140.00

(0.2)

(1.1)

(19.1)

FTSE 100

6,746.84

(0.2)

0.2

14.4

Euro

1.35

(0.3)

(0.1)

2.1

Yen

98.50

(0.1)

(0.2)

13.5

Nikkei

GBP

1.60

0.5

0.8

(1.3)

CHF

1.09

(0.4)

(0.1)

0.2

AUD

0.95

(0.0)

0.7

(8.5)

USD Index

80.71

0.2

(0.0)

RUB

32.55

0.7

0.5

BRL

0.44

(1.7)

(1.2)

(10.2)

Gold/Ounce

Silver/Ounce

Crude Oil (Brent)/Barrel (FM

Future)

Natural Gas (Henry

Hub)/MMBtu

North American Spot LPG

Propane Price

North American Spot LPG

Normal Butane Price

Close ($)

1D%

WTD%

YTD%

Global Indices Performance

1,311.81

(0.2)

(0.3)

(21.7)

DJ Industrial

21.71

0.2

(0.8)

(28.5)

105.33

(0.8)

(0.5)

3.36

(0.5)

116.75

4,253.34

(0.8)

(0.5)

16.8

14,225.37

0.2

0.2

36.8

MSCI EM

1,016.30

(1.0)

(1.1)

(3.7)

SHANGHAI SE Composite

2,157.24

0.4

0.4

(4.9)

HANG SENG

23,038.95

(0.6)

(0.9)

1.7

1.2

BSE SENSEX

20,974.79

(1.2)

(1.0)

8.0

6.6

Bovespa

53,831.85

(1.1)

(0.3)

(11.7)

1,460.23

(1.0)

(1.0)

(4.4)

Source: Bloomberg

CAC 40

RTS

Source: Bloomberg

Contacts

Saugata Sarkar

Ahmed M. Shehada

Keith Whitney

Sahbi Kasraoui

Head of Research

Head of Trading

Head of Sales

Manager - HNWI

Tel: (+974) 4476 6534

Tel: (+974) 4476 6535

Tel: (+974) 4476 6533

Tel: (+974) 4476 6544

saugata.sarkar@qnbfs.com.qa

ahmed.shehada@qnbfs.com.qa

keith.whitney@qnbfs.com.qa

sahbi.alkasraoui@qnbfs.com.qa

QNB Financial Services SPC

Contact Center: (+974) 4476 6666

PO Box 24025

Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 5 of 5