Solution Manual For Financial Statement Analysis, 13th Edition By Charles H. ...

22 June Daily market report

1. Page 1 of 6

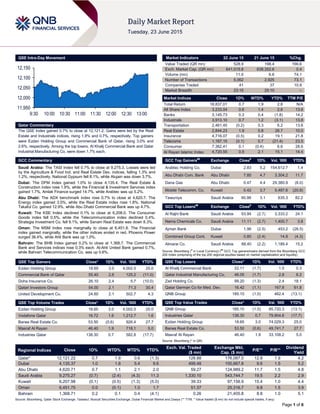

QSE Intra-Day Movement

Qatar Commentary

The QSE Index gained 0.7% to close at 12,121.2. Gains were led by the Real

Estate and Industrials indices, rising 1.9% and 0.7%, respectively. Top gainers

were Ezdan Holding Group and Commercial Bank of Qatar, rising 3.0% and

2.6%, respectively. Among the top losers, Al Khalij Commercial Bank and Qatar

Industrial Manufacturing Co. were down 1.7% each.

GCC Commentary

Saudi Arabia: The TASI Index fell 0.7% to close at 9,275.3. Losses were led

by the Agriculture & Food Ind. and Real Estate Dev. indices, falling 1.3% and

1.2%, respectively. National Gypsum fell 8.1%, while Alujain was down 3.7%.

Dubai: The DFM Index gained 1.0% to close 4,135.4. The Real Estate &

Construction index rose 1.9%, while the Financial & Investment Services index

gained 1.7%. Amlak Finance surged 14.7%, while Arabtec was up 5.2%.

Abu Dhabi: The ADX benchmark index rose 0.7% to close at 4,620.7. The

Energy index gained 3.5%, while the Real Estate index rose 1.8%. National

Takaful Co. gained 12.9%, while Abu Dhabi Commercial Bank was up 4.7%.

Kuwait: The KSE Index declined 0.1% to close at 6,208.0. The Consumer

Goods index fell 0.5%, while the Telecommunication index declined 0.4%.

Strategia Investment Co. fell 9.1%, while Sanam Real Estate was down 8.3%.

Oman: The MSM Index rose marginally to close at 6,451.8. The Financial

index gained marginally, while the other indices ended in red. Phoenix Power

surged 36.4%, while Ahli Bank was up 1.0%.

Bahrain: The BHB Index gained 0.2% to close at 1,368.7. The Commercial

Bank and Services indices rose 0.3% each. Al-Ahli United Bank gained 0.7%,

while Bahrain Telecommunication Co. was up 0.6%.

QSE Top Gainers Close* 1D% Vol. ‘000 YTD%

Ezdan Holding Group 18.65 3.0 4,002.5 25.0

Commercial Bank of Qatar 55.40 2.6 125.2 (11.0)

Doha Insurance Co. 26.10 2.4 5.7 (10.0)

Qatari Investors Group 54.00 2.1 71.3 30.4

United Development Co. 24.60 2.1 502.7 4.3

QSE Top Volume Trades Close* 1D% Vol. ‘000 YTD%

Ezdan Holding Group 18.65 3.0 4,002.5 25.0

Vodafone Qatar 16.72 1.6 1,212.7 1.6

Barwa Real Estate Co. 53.50 (0.6) 926.4 27.7

Masraf Al Rayan 46.40 1.9 718.1 5.0

Industries Qatar 138.30 0.7 582.8 (17.7)

Market Indicators 22 June 15 21 June 15 %Chg.

Value Traded (QR mn) 528.9 198.4 166.6

Exch. Market Cap. (QR mn) 641,015.8 638,352.6 0.4

Volume (mn) 11.5 6.6 74.1

Number of Transactions 5,062 2,925 73.1

Companies Traded 41 37 10.8

Market Breadth 23:15 25:10 –

Market Indices Close 1D% WTD% YTD% TTM P/E

Total Return 18,837.01 0.7 1.9 2.8 N/A

All Share Index 3,233.04 0.6 1.4 2.6 13.6

Banks 3,145.73 0.3 0.4 (1.8) 14.2

Industrials 3,913.10 0.7 1.2 (3.1) 13.8

Transportation 2,461.45 (0.2) 0.3 6.2 13.6

Real Estate 2,844.23 1.9 5.8 26.7 10.0

Insurance 4,716.07 (0.5) 0.2 19.1 21.8

Telecoms 1,167.15 (0.1) 0.7 (21.4) 23.5

Consumer 7,362.41 0.1 (0.4) 6.6 28.6

Al Rayan Islamic Index 4,720.55 0.9 2.1 15.1 14.4

GCC Top Gainers##

Exchange Close#

1D% Vol. ‘000 YTD%

Arabtec Holding Co. Dubai 2.83 5.2 154,612.7 1.4

Abu Dhabi Com. Bank Abu Dhabi 7.85 4.7 3,304.2 11.7

Dana Gas Abu Dhabi 0.47 4.4 29,380.9 (6.0)

Mobile Telecomm. Co. Kuwait 0.42 3.7 5,487.6 (20.8)

Tawuniya Saudi Arabia 90.99 3.1 635.3 82.2

GCC Top Losers##

Exchange Close#

1D% Vol. ‘000 YTD%

Al Rajhi Bank Saudi Arabia 63.84 (2.7) 3,333.2 24.1

Nama Chemicals Co. Saudi Arabia 11.11 (2.7) 1,400.7 3.8

Ajman Bank Dubai 1.96 (2.5) 453.2 (26.5)

Combined Group Cont. Kuwait 0.80 (2.4) 14.8 (4.3)

Almarai Co. Saudi Arabia 88.40 (2.2) 1,189.4 15.2

Source: Bloomberg (

#

in Local Currency) (

##

GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

QSE Top Losers Close* 1D% Vol. ‘000 YTD%

Al Khalij Commercial Bank 22.11 (1.7) 1.5 0.3

Qatar Industrial Manufacturing Co. 46.05 (1.7) 2.8 6.2

Zad Holding Co. 99.20 (1.3) 2.4 18.1

Qatar German Co for Med. Dev. 16.42 (1.1) 167.8 61.8

QNB Group 185.10 (1.0) 462.4 (13.1)

QSE Top Value Trades Close* 1D% Val. ‘000 YTD%

QNB Group 185.10 (1.0) 85,720.3 (13.1)

Industries Qatar 138.30 0.7 79,904.6 (17.7)

Ezdan Holding Group 18.65 3.0 74,029.3 25.0

Barwa Real Estate Co. 53.50 (0.6) 49,741.7 27.7

Masraf Al Rayan 46.40 1.9 33,108.2 5.0

Source: Bloomberg (* in QR)

Regional Indices Close 1D% WTD% MTD% YTD%

Exch. Val. Traded

($ mn)

Exchange Mkt.

Cap. ($ mn)

P/E** P/B**

Dividend

Yield

Qatar* 12,121.22 0.7 1.9 0.6 (1.3) 128.88 176,087.0 12.8 1.9 4.2

Dubai 4,135.37 1.0 1.8 5.4 9.6 499.48 100,667.8 9.6 1.5 5.2

Abu Dhabi 4,620.71 0.7 1.1 2.1 2.0 59.27 124,989.2 11.7 1.5 4.8

Saudi Arabia 9,275.27 (0.7) (2.4) (4.3) 11.3 1,330.10 543,744.7 19.5 2.2 2.9

Kuwait 6,207.98 (0.1) (0.5) (1.3) (5.0) 39.33 97,156.9 15.4 1.0 4.4

Oman 6,451.75 0.0 (0.1) 1.0 1.7 51.37 25,316.7 9.8 1.5 3.9

Bahrain 1,368.71 0.2 0.1 0.4 (4.1) 0.26 21,405.8 8.8 1.0 5.1

Source: Bloomberg, Qatar Stock Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

11,950

12,000

12,050

12,100

12,150

9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

2. Page 2 of 6

Qatar Market Commentary

The QSE Index gained 0.7% to close at 12,121.2. The Real

Estate and Industrials indices led the gains. The index rose on

the back of buying support from non-Qatari and GCC

shareholders despite selling pressure from Qatari shareholders.

Ezdan Holding Group and Commercial Bank of Qatar were the

top gainers, rising 3.0% and 2.6%, respectively. Among the top

losers, Al Khalij Commercial Bank and Qatar Industrial

Manufacturing Co. were down 1.7% each.

Volume of shares traded on Monday rose by 74.1% to 11.5mn

from 6.6mn on Sunday. However, as compared to the 30-day

moving average of 15.1mn, volume for the day was 23.7% lower.

Ezdan Holding Group and Vodafone Qatar were the most active

stocks, contributing 34.7% and 10.5% to the total volume,

respectively.

Source: Qatar Stock Exchange (* as a % of traded value)

Ratings and Global Economic Data

Ratings Updates

Company Agency Market Type* Old Rating New Rating Rating Change Outlook Outlook Change

Banque Saudi

Fransi (BSF)

Capital

Intelligence

Saudi

Arabia

FSR/LT FCR/ST

FCR/SR

A/A+/A1/2 A+/A+/A1/2 Stable –

Source: News reports (* LT – Long Term, ST – Short Term, FSR- Financial Strength Rating, FCR – Foreign Currency Rating, LCR – Local Currency Rating, IDR – Issuer Default Rating, SR – Support Rating, LC

– Local Currency)

Global Economic Data

Date Market Source Indicator Period Actual Consensus Previous

06/22 US National Assoc. of Real. Existing Home Sales MoM May 5.10% 4.40% -2.30%

06/22 US Chicago Fed Chicago Fed Nat Activity Index May -0.17 0.12 -0.19

06/22 EU European Commission Consumer Confidence June -5.6 -5.8 -5.6

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

News

Qatar

QNBK to disclose financials on July 8 – QNB Group (QNBK)

will disclose the reviewed financial reports for the period ending

June 30, 2015 on July 8, 2015. (QSE)

SFG: Qatar’s inflation to reach 2.5% in 2016; major

infrastructure spending to continue – Samba Financial Group

(SFG) in its latest country report, has said that domestic

population pressures may push Qatar’s inflation to 2.5% in 2016

from 2% in 2015. Consumer prices have fallen sharply since the

index was rebased and reweighted in January 2015, with

inflation standing at 0.9% YoY in April. A major outcome of the

change in the index is a smaller weighting of the rental

component. Rental inflation has been elevated over the last 12

months, offset by the strong dollar and soft international

commodity prices, which have kept a lid on the overall index.

SFG expects these trends to persist. Meanwhile, SFG said

major infrastructure investments in Qatar will go ahead on the

back of planned and ongoing capital expenditure (capex) worth

around $200bn. The spending explicitly linked to the 2022 FIFA

World Cup is about $15.4bn, which represents only 7.5% of the

capex. Aided by large reserves built up from years of

accumulated oil & gas revenues, SFG expects the authorities

concerned to continue implementing the spending set out in the

National Development Strategy (NDS) when oil prices were over

$100 a barrel. (Gulf-Times.com)

Woqod signs MoU with QMIC for managing logistics –

Woqod (QFLS) has entered into a MoU with Qatar Mobility

Innovations Center (QMIC) for its ‘Masarak’ solution. As part of

the agreement, Woqod will be using Masarak’s iFleet solution

for fleet logistics and telematics management. Masarak is an

intelligent end-to-end solution and suite of services, which was

developed locally by QMIC, in partnership with the Ministry of

Municipality & Urban Planning. (Gulf-Times.com)

Al Khafji Street development to start from Wednesday – The

Public Works Authority, Ashghal will start the three-month long

first phase of the developmental works of Al Khafji Street in the

West Bay area on June 24, 2015. The works include converting

the Jelaiha roundabout into a signal-controlled intersection as

well as upgrading around 300 meters of the streets surrounding

the roundabout, namely Al Khafji Street and the Arab League

Street. (Gulf-Times.com)

Ministry blacklists 807 firms – The Ministry of Labor & Social

Affairs blacklisted 807 companies for violation of labor laws in

1H2015. The ministry has so far banned 3,913 companies —

around 5% of the total number of companies registered in Qatar.

The blacklisted companies are barred from recruiting new

workers. (Peninsula Qatar)

Council returns draft law on expats for further study – The

Advisory Council has expressed serious apprehensions about

several articles in the draft law organizing the exit, entry and

stay of foreign workers and has returned the draft for further

study. The draft law was put to vote after discussion during a

regular session of the Council on Monday, and a majority of the

members voted against it. Al Sharq reported that the Council

Chairman, Mohammed bin Mubarak Al Khulaifi, concluded the

discussion on the draft by saying that there was no need to

hurry in passing the law. The Council also sought to review

samples of new job contracts and the procedures for protecting

rights of employers and needs of citizens and expatriates. The

Overall Activity Buy %* Sell %* Net (QR)

Qatari 50.21% 68.97% (99,214,347.03)

GCC 19.88% 13.12% 35,789,890.46

Non-Qatari 29.91% 17.91% 63,424,456.57

3. Page 3 of 6

members urged the bodies concerned at the Ministry of Interior

to pay heed to their opinion on the draft law. (Peninsula Qatar)

Advisory Council approves draft law to regulate private

schools – The Advisory Council has approved a draft law

regulating private schools. The draft law replaces the old law

governing private schools and stipulates new rules and

regulations for licensing and monitoring of private schools. The

Council also approved the draft law stipulating stiffer

punishments on private education centers for violations. Centers

violating the rules can be closed for up to 60 days and their

name boards can be removed under a court order. Violators can

be forced to refund all the fees it collected from students.

Further, the Advisory Council’s Services & Public Utilities

Committee studied a floor request forwarded by a number of

members on the cost of health insurance. (Peninsula Qatar)

International

US home resale jumps to over five-year high in May – Home

resale in the US surged to a five-and-a-half years high in May as

first-time buyers stepped into the market, the latest indication

that housing and overall economic activity gathered steam in

2Q2015. The National Association of Realtors said existing

home sales increased 5.1% to an annual rate of 5.35mn units,

the highest level since November 2009. That put sales on track

for their strongest gain in 2015 since 2007. The Realtors group

revised April’s sales pace up to 5.09mn units from the previously

reported 5.04mn units. First-time buyers accounted for 32% of

transactions, the largest share since September 2012. Still, the

share remains well below the 40-45% that economists and

realtors say is required for a robust housing market. Tightening

labor market conditions are starting to spur stronger wage

growth, boosting demand for housing. (Reuters)

Greece proposes new measures to avert default, creditors

hopeful – Greece took a step back from the abyss on Monday

with the presentation of new budget proposals that Eurozone

leaders welcomed as a basis for a possible agreement in the

coming days to unlock the frozen aid and avert a looming

default. The Greek proposals included higher taxes and welfare

charges and steps to curtail early retirement, but not the nominal

pension and wage cuts first sought by lenders. Leftist Prime

Minister Alexis Tsipras also appeared to have avoided raising

value added tax on electricity or loosening job protection laws.

European Council President Donald Tusk called the Greek

proposals “a positive step forward”. He said the aim was to get

the euro group finance ministers’ approval for a cash-for-reform

package on Wednesday evening and put it to Eurozone leaders

for their final endorsement on Thursday morning. (Reuters)

Japan manufacturing declines in June as new orders dip –

The manufacturing sector in Japan contracted slightly in June as

new orders fell and output growth slowed indicating the

economy may have lost some momentum. The Markit/JMMA

flash Japan Manufacturing Purchasing Managers Index (PMI)

fell to a seasonally adjusted 49.9 in June from a final 50.9 in

May. The output index fell to a preliminary 50.5 in June,

following 51.9 in May. New orders fell to a preliminary 49.4 from

50.9 in May, also indicating the first decline in a month.

However, new export orders rose to 53.6 from a final 50.6 in the

previous month. That marked the fastest expansion in four

months, suggesting overseas demand is starting to gather

strength. The final Markit/JMMA PMI for June is due on July 1.

(Reuters)

China factory activity contracts in June; Beige Book survey

says economy recovers in 2Q2015 – According to the

HSBC/Markit Flash China Manufacturing Purchasing Managers’

survey, China’s factory activity contracted for the fourth straight

month in June but showed some signs of stabilizing. The PMI

index edged up to 49.6, a three-month high, from 49.2 in May,

but remained below the 50 mark, which separates contraction

from expansion. New orders returned to positive territory at 50.4

and new export orders fell at a slower pace, but companies

stepped up layoffs. Meanwhile, according to the China Beige

Book survey, published by New York-based CBB International,

China’s economy saw a broad-based recovery in 2Q2015 on

resurgence in retail and a rebound in property. The survey said

that companies are doing better than the official data shows,

and deflation risks may have peaked. The economy is

rebalancing as central and southwest regions outperform.

Leland Miller, President of the survey publisher, and Craig

Charney, Director of Research & Polling, said that expanding

sales volumes, rather than a stock rally, fueled the recovery.

(Reuters, Bloomberg)

Brazil current account deficit in May lower than estimated –

Brazil’s current account deficit in May was narrower than

economists had estimated, as the trade surplus grew from the

month before. According to the central bank report, the deficit in

the current account, the broadest measure of trade in goods and

services, narrowed in May to $3.4bn from $6.9bn in April and

was lower as compared to estimates of $4.6bn deficit. Foreign

investment in Brazil rose to $6.6bn from $5.8bn during May. The

current account gap through May 2015 totaled $35.8bn, down

from a $44.9bn deficit in the same period last year. Foreign

direct investment reached $25.5bn through May, compared to

$39.3bn during the same period of 2014. The central bank

lowered its estimate for the current account to a gap of $81bn in

2015 from $84bn, and left its forecast for foreign investment

unchanged at $80bn. (Bloomberg)

Regional

Strategy&: MENA digitization could add $820bn to regional

economy – According to a report released by Strategy&, the

Middle East and North Africa’s (MENA) digital market value is

expected to reach $35bn in 2015 and overall digitization

initiatives could add $820bn to the regional economy, even as

the region is seen as an attractive target for a wide array of

cyber-threats. Strategy& in its report suggested that a central

national cyber-security body (CNCB) should be initially

established, and be in charge of defining the national cyber-

security agenda. (GulfBase.com)

AATSC announces partial redemption of Sukuk – Arabian

Aramco Total Services Company (AATSC) has partially

redeemed the AATSC Sukuk (that is scheduled in every six

months) on June 21, 2015. The redemption resulted in a fixed

distribution payment of SR90mn, representing 2.40% of the

aggregate face amount of AATSC Sukuk. Accordingly, the face

amount of AATSC Sukuk becomes SR95,480 and the aggregate

face value becomes SR3.58bn. (Tadawul)

Sadara receives SAGIA’s highest investment rating –

Sadara Chemical Company (Sadara) has been classified as

‘Strategic’ by the Saudi Arabian General Investment Authority

(SAGIA). This puts Sadara in the highest classification category

achievable under SAGIA's current investment rankings.

(GulfBase.com)

Riyad Bank prices SR4bn capital-boosting Sukuk –

According to banking sources, Riyad Bank has issued capital-

boosting Sukuk worth SR4bn. The sources said that the deal,

which will enhance the bank's Tier 2 or supplementary capital,

was priced at the end of last week at 115 basis points over the

Saudi interbank offered rate. The bank had announced the

privately-placed Sukuk on May 5, 2015 with a tenor of 10 years

4. Page 4 of 6

although it allows the issuer to redeem the security after five

years. (Reuters)

ICD secures $300mn Islamic Murabaha financing – The

Islamic Corporation for the Development of the Private Sector

(ICD), the private sector arm of the Islamic Development Bank

Group (IDB), has secured a 13-month $300mn Islamic

Murabaha financing facility from Dubai Islamic Bank, First Gulf

Bank, Mizuho Bank (Malaysia) and Mizuho Bank Nederland in

early June 2015. Dubai Islamic Bank acted as the sole

coordinator of the facility, in addition to being the mandated lead

arranger along with First Gulf Bank, Mizuho Bank Malaysia and

Mizuho Bank Nederland. (GulfBase.com)

Saudi Aramco may shut Jeddah refinery – According to

sources, Saudi Arabian Oil Company (Saudi Aramco) is

considering whether to close its 90,000 barrel per day crude oil

refinery in Jeddah for several years because of age and

environmental concerns. Saudi Aramco was originally

considering whether to close it in 2018 but is now likely to

postpone the closure to as late as 2022 because of growing

domestic demand for oil products and since construction of a

new refinery at Jizan, also on the Red Sea coast, has been

delayed. (Reuters)

Nokia Networks, Zain KSA complete Saudi-first carrier

aggregation project – Nokia Networks and Zain KSA have

completed the Saudi-first carrier aggregation project, where they

combined FDD-LTE bands of 1,800 and of 2,100 megahertz

(MHz). (Reuters)

NCB completes issuance of SR1bn capital-boosting Sukuk

– The National Commercial Bank (NCB) has raised a capital-

boosting Sukuk worth SR1bn. The privately-placed Sukuk,

which would boost its Tier 1 or core capital, is Basel III compliant

and has a perpetual tenor, although the bank would have the

right to call the Sukuk on a predefined date. The Sukuk will also

extend the maturity profile of NCB's liabilities while continuing to

diversify its sources of funding. JP Morgan and NCB Capital

acted as the arrangers for the transaction. (Reuters)

NCB: Saudi Arabia sees moderate business cycle during

2015-2016 – The National Commercial Bank (NCB) in its ‘Saudi

Economic Review’ for June 2015 said that the Kingdom will face

a moderate business cycle during 2015 and 2016, growing

around 3% in real terms. In 2015, the macroeconomic

projections were based on an average Arabian Light crude oil

price of $65/bbl and an average daily crude oil production level

of 9.8MMBD. Accordingly, this projected decline in oil prices will

result in lower oil revenues, which will weigh negatively on the

fiscal and current accounts that will register deficits of 11.7%

and 3% out of GDP, respectively. The real GDP growth is

expected to rise by 3.4%, mainly due to expected growth in the

non-oil sector by 5.1%, driven by the private sector that will

compensate for the insignificant contribution of oil. As per the

report, the key beneficiaries in 2015 will be trade, construction

and manufacturing sectors, growing at 7%, 6% and 6%,

respectively. The projections for the three sectors are supported

by the recent royal decrees, buoyant activity in the projects’

market and resilient business confidence. (GulfBase.com)

CMA approves Alistithmar Capital’s offering of investment

fund – The Capital Market Authority (CMA) Board of

Commissioners has approved the “SAIB Saudi IPO Fund” offer

by Alistithmar Capital for financial securities and brokerage

company (Alistithmar Capital). (Tadawul)

NI creates e-commerce solution for SMEs – Network

International (NI) has partnered with Nexxus Payment Group

and Aramex to create NexxusPay, an end-to-end e-commerce

solution for small & medium enterprises (SMEs) in the UAE.

NexxusPay is a customized and cost-effective one-stop platform

for small businesses looking to venture into e-commerce.

(GulfBase.com)

Foreign ownership restriction on Etisalat shares lifted –

Emirates Telecommunications Corporation (Etisalat) announced

that Federal Government decided to lift the restriction on Etisalat

stock ownership by the local institutions, foreign institutions and

expatriate individuals, provided such ownership does not exceed

20%. Currently, the UAE government owns 60% of Etisalat

shares through Emirates Investment Authority (EIA) while UAE

nationals hold 40%. EIA has no intention to reduce its stake in

Etisalat. (ADX)

DI completes acquisition of 59.66% stake in Al Mal Capital –

Dubai Investments (DI) has completed acquisition of 59.66%

stake in Al Mal Capital, which when allied to the 1.20% already

held by the company, equates to an overall shareholding of

60.86%. Al Mal offers a wide range of investment products

spread across its business lines of investment banking,

brokerage and asset management. This acquisition will enhance

DI’s in-house capabilities in managing its investment activities

while at the same time providing a steady pipeline of deal flow to

Al Mal. (DFM)

UPAC signs agreement to build mall in UAE – United

Projects Company for Aviation Services (UPAC), a subsidiary of

Agility Public Warehousing, has signed an agreement with one

of the subsidiaries of National Real Estate Company for the

development of a commercial mall in Abu Dhabi. UPAC’s

investment in the project may reach $225mn over the next three

years. (DFM)

52mn subscriptions in Emaar Misr’s IPO – Emaar Misr for

Development, the Egypt-based subsidiary of Emaar Properties,

has witnessed 52mn subscriptions in its IPO. The subscriptions

phase started on June 16 and will last until June 25, 2015.

Earlier, Emaar Misr has announced its plans to offer 600mn

shares, around 13% of the company’s capital, at a price ranging

between EGP3.5 and EGP4.25 per share. Around 15% of the

company’s offered shares, 90m shares, will be on the Egyptian

Stock Exchange (EGX). (GulfBase.com)

S&P: Dubai property prices likely to fall 10-20% in 2015 –

According to Standard & Poor's (S&P), Dubai residential

property prices are likely to fall 10-20% in 2015 because of

subdued demand, slower economic activity and downbeat

investor sentiment. In early 2015, non-resident demand from

Russia and other member countries of the Gulf Cooperation

Council remained largely subdued. S&P expects oil prices to

remain weak through to 2016-end, as the economic growth in

the UAE as a whole is likely to slow markedly in 2015 and 2016.

S&P also warned that a fall in Dubai's stock index would likely

affect investor views on property. (Reuters)

DSC: Dubai inflation rose 4.7% in May 2015 – According to

the Dubai Statistics Center (DSC), Dubai's annual inflation rate

rose 4.7% in May 2015, its highest level since 2009. The

housing and utility costs, which account for around 44% of

consumer expenses, jumped 7.8% from a year earlier in May

2015 and rose 0.7% as compared to April 2015. The food &

beverage prices, which account for 11% of the basket, rose

1.7% YoY and 3% MoM. (GulfBase.com)

Amlak mulls partnership with Emaar – Dubai-based Amlak

Finance is in talks with Emaar Properties to develop land in

distinctive locations. (GulfBase.com)

Moody's assigns P-1 rating to NBAD's Euro Commercial

Paper program – Moody's Investors Service has assigned a

5. Page 5 of 6

Prime-1 short-term foreign and local currency ratings to the

$5bn Euro-commercial paper (ECP) program of National Bank

of Abu Dhabi (NBAD; Aa3 long term bank deposits rating with a

stable outlook; baseline credit assessment a3; Prime-1 short

term ratings). (GulfBase.com)

ADIC appoints Chairman – Abu Dhabi Investment Council

(ADIC) has appointed Sheikh Mohammed bin Zayed Al-Nahyan,

the Crown Prince of Abu Dhabi, as its Chairman. He replaces

President Sheikh Khalifa bin Zayed Al-Nahyan. (Reuters)

Kuwait’s Al-Zour oil refinery to be delayed beyond 2019 –

Kuwait's Al-Zour oil refinery is expected to be pushed beyond

early 2019 as state refiner Kuwait National Petroleum Company

(KNPC) is seeking additional funds to finance the refinery. The

615,000 barrels per day oil refinery, originally planned more than

a decade ago, would be the biggest in the Middle East, but the

project has been repeatedly delayed by bureaucratic and

political issues, including tensions between Kuwait's parliament

and the cabinet. (Reuters)

NBK: Kuwait current account surplus narrows on lower oil

prices – According to National Bank of Kuwait (NBK), Kuwait

current account surplus narrowed from KD20.2bn in 2013 to

KD15.1bn in 2014. The surplus was mainly driven lower by a

decline in the goods and services balance, as oil export

revenues declined and the deficit in net services outflows

swelled to a new high. Higher investment income though helped

offset some of that decline. The goods and services balance slid

from KD25.6bn in 2013 to KD22bn in 2014, mainly on the back

of a 10% YoY decline in oil exports. Solid import growth and a

widening of the net services deficit also contributed to the

decline in the trade balance. The fall in oil exports was due to a

9% YoY drop in oil prices and a 2% YoY decrease in production.

Imports grew at a slower but still strong pace of 7% YoY in

2014, rising to KD7.8bn. Meanwhile, net services outflows

continued to rise and hit a new high of KD5bn in 2014. The rise

was predominantly driven by a KD0.4bn increase in travel

spending. (GulfBase.com)

CBO approves Ominvest-ONIC merger – The Central Bank of

Oman’s (CBO) board has approved the merger between Oman

International Development & Investment Company (Ominvest)

and Oman National Investment Corporation (ONIC).

(GulfBase.com)

OHB EGA approves capital increase of OMR70mn – The

Oman Housing Bank’s (OHB) extraordinary general assembly

(EGA) has approved a proposal to increase the bank's capital

from OMR30mn to OMR100mn. The EGA approved to increase

the capital in cash and amend the related provisions of the

bank's articles of association accordingly. The increase will

enhance the bank's financial resources and enable it to meet its

loan plans, as well as support the construction growth in the

Sultanate. (GulfBase.com)

Takaful, Copart Bahrain sign agreement – Takaful

International Company and Copart Bahrain have signed an

agreement to regulate the sale of damaged cars from traffic

accidents through an auction. This agreement will ensure full

regulation of the sale of damaged vehicles after reimbursing the

insured client. (Bahrain Bourse)

GFH to appeal against BCDR’s decision – The Bahrain

Chamber for Dispute Resolution (BCDR) has dismissed the

legal case filed by the Gulf Finance House (GFH) against

Tanmiyat Investment Group and others. The legal case was filed

for the reimbursement of $60mn previously paid to the

defendant in 2005 by GFH as underwriting fees toward Legends

project. Accordingly, GFH’s legal team is considering the

reasons behind BCDR’s verdict, as it prepares to lodge an

appeal before the court of cassation. (Bahrain Bourse)

CBB: Sukuk Al-Salam securities oversubscribed by 276% –

The Central Bank of Bahrain (CBB) announced that the monthly

issue of the Sukuk Al-Salam Islamic securities for the BHD43mn

issue, which carries a maturity of 91 days, has been

oversubscribed by 276%. The expected return on the issue,

which begins on June 24, 2015 and matures on September 23,

2015, is 1.20% equivalent to 1.20% for the previous issue on

May 27, 2015. The securities are issued by the CBB on behalf of

the Government of the Kingdom of Bahrain. (GulfBase.com)

Mumtalakat plans more investments in 2015 – Bahrain’s

Mumtalakat Holding Company (Mumtalakat) is planning few

more investments before 2015-end, and is looking to invest in

the GCC region, Europe and the US, after making significant

investments in 2014 in its quest for diversification. The

sovereign fund’s 2014 revenues rose 11% to be at BHD1.2bn

with a gross profit of BHD181mn. (GulfBase.com)

Alba appoints two new managers for key departments –

Aluminium Bahrain (Alba) has appointed S. Hussain S. Fadhel

as the Manager of Reduction Lines 1-3 and Mustafa A. Rahman

as the Manager for Carbon 3. (Bahrain Bourse)

6. Contacts

Saugata Sarkar Sahbi Kasraoui QNB Financial Services SPC

Head of Research Head of HNI Contact Center: (+974) 4476 6666

Tel: (+974) 4476 6534 Tel: (+974) 4476 6544 PO Box 24025

saugata.sarkar@qnbfs.com.qa sahbi.alkasraoui@qnbfs.com.qa Doha, Qatar

Disclaimer and Copyright Notice: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of QNB SAQ (“QNB”). QNBFS is regulated by the

Qatar Financial Markets Authority and the Qatar Exchange QNB SAQ is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is

not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. QNBFS accepts no liability

whatsoever for any direct or indirect losses arising from use of this report. Any investment decision should depend on the individual circumstances of the investor and be based on specifically

engaged investment advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report

has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. QNBFS does not make any

representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. For reports dealing with Technical Analysis,

expressed opinions and/or recommendations may be different or contrary to the opinions/recommendations of QNBFS Fundamental Research as a result of depending solely on the historical

technical data (price and volume). QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment

decisions that differ significantly from, or even contradict, the views and opinions included in this report. This report may not be reproduced in whole or in part without permission from QNBFS

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 6 of 6

Rebased Performance Daily Index Performance

Source: Bloomberg Source: Bloomberg

Source: Bloomberg Source: Bloomberg (*$ adjusted returns;

#

Market closed on 22 June, 2015)

80.0

100.0

120.0

140.0

160.0

180.0

200.0

220.0

May-11 May-12 May-13 May-14 May-15

QSE Index S&P Pan Arab S&P GCC

(0.7%)

0.7%

(0.1%)

0.2%

0.0%

0.7%

1.0%

(2.0%)

(1.0%)

0.0%

1.0%

2.0%

SaudiArabia

Qatar

Kuwait

Bahrain

Oman

AbuDhabi

Dubai

Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D%* WTD%* YTD%*

Gold/Ounce 1,185.89 (1.2) (1.2) 0.1 MSCI World Index 1,796.12 1.2 1.2 5.1

Silver/Ounce 16.22 0.7 0.7 3.3 DJ Industrial 18,119.78 0.6 0.6 1.7

Crude Oil (Brent)/Barrel (FM

Future)

63.34 0.5 0.5 10.5 S&P 500 2,122.85 0.6 0.6 3.1

Crude Oil (WTI)/Barrel (FM

Future)

59.68 0.1 0.1 12.0 NASDAQ 100 5,153.97 0.7 0.7 8.8

Natural Gas (Henry

Hub)/MMBtu

2.78 (1.2) (1.2) (7.3) STOXX 600 394.25 2.4 2.4 8.1

LPG Propane (Arab Gulf)/Ton 35.63 2.5 2.5 (27.3) DAX 11,460.50 4.0 4.0 9.3

LPG Butane (Arab Gulf)/Ton 45.00 (1.1) (1.1) (28.3) FTSE 100 6,825.67 1.4 1.4 5.6

Euro 1.13 (0.1) (0.1) (6.3) CAC 40 4,998.61 4.0 4.0 9.9

Yen 123.37 0.5 0.5 3.0 Nikkei 20,428.19 0.7 0.7 13.4

GBP 1.58 (0.4) (0.4) 1.6 MSCI EM 987.30 1.3 1.3 3.2

CHF 1.09 (0.4) (0.4) 7.9 SHANGHAI SE Composite#

4,478.36 0.0 0.0 38.4

AUD 0.77 (0.6) (0.6) (5.5) HANG SENG 27,080.85 1.2 1.2 14.8

USD Index 94.33 0.3 0.3 4.5 BSE SENSEX 27,730.21 1.5 1.5 0.5

RUB 53.94 (0.2) (0.2) (11.2) Bovespa 53,863.68 0.3 0.3 (7.3)

BRL 0.32 0.6 0.6 (14.0) RTS 978.85 1.2 1.2 23.8

174.2

138.5

125.7