Independent Lucknow Call Girls 8923113531WhatsApp Lucknow Call Girls make you...

26 February Daily market report

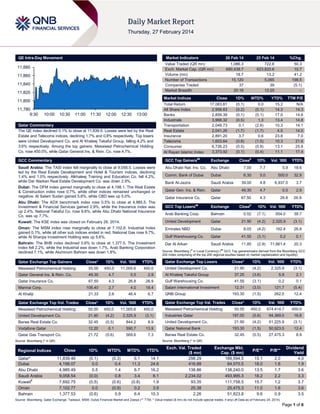

1. QE Intra-Day Movement

Market Indicators

11,880

11,860

11,840

11,820

25 Feb 14

%Chg.

1,086.3

690,438.7

18.7

15,120

37

20:16

722.6

623,820.6

13.2

5,065

39

12:25

50.3

10.7

41.2

198.5

(5.1)

–

Market Indices

11,800

11,780

9:30

26 Feb 14

Value Traded (QR mn)

Exch. Market Cap. (QR mn)

Volume (mn)

Number of Transactions

Companies Traded

Market Breadth

10:00

10:30

11:00

11:30

12:00

12:30

13:00

Qatar Commentary

The QE index declined 0.1% to close at 11,839.5. Losses were led by the Real

Estate and Telecoms indices, declining 1.7% and 0.8% respectively. Top losers

were United Development Co. and Al Khaleej Takaful Group, falling 4.2% and

3.6% respectively. Among the top gainers, Mesaieed Petrochemical Holding

Co. rose 450.0%, while Qatar General Ins. & Rein. Co. rose 4.7%.

Close

Total Return

All Share Index

Banks

Industrials

Transportation

Real Estate

Insurance

Telecoms

Consumer

Al Rayan Islamic Index

1D%

WTD%

YTD%

TTM P/E

17,083.81

2,958.63

2,859.39

3,968.32

2,049.73

2,041.26

2,891.20

1,603.64

6,726.23

3,373.92

(0.1)

(0.2)

(0.1)

(0.5)

0.1

(1.7)

3.7

(0.8)

(0.5)

(0.1)

0.0

(0.1)

(0.1)

1.3

(2.6)

(1.7)

0.6

(1.5)

(0.9)

(0.4)

15.2

14.3

17.0

13.4

10.3

4.5

23.8

10.3

13.1

11.1

N/A

14.3

14.6

14.8

14.1

14.0

7.0

21.6

25.8

17.4

GCC Commentary

GCC Top Gainers##

Exchange

Close#

1D%

Saudi Arabia: The TASI index fell marginally to close at 9,058.5. Losses were

led by the Real Estate Development and Hotel & Tourism indices, declining

1.4% and 1.0% respectively. Alkhaleej Training and Education Co. fell 4.2%,

while Dar Alarkan Real Estate Development Co. was down 2.9%.

Abu Dhabi Nat. Ins. Co.

Abu Dhabi

7.00

7.7

5.9

18.6

Comm. Bank of Dubai

Dubai

6.30

5.0

500.0

32.9

Bank Al-Jazira

Saudi Arabia

39.00

4.8

6,937.0

3.7

Qatar Gen. Ins. & Rein.

Qatar

49.30

4.7

0.5

2.9

Qatar Insurance Co.

Qatar

67.50

4.3

26.8

26.9

Dubai: The DFM index gained marginally to close at 4,198.1. The Real Estate

& Construction index rose 0.7%, while other indices remained unchanged or

negative. Al Salam Sudan gained 5.8%, while CBD was up 5.0%.

Abu Dhabi: The ADX benchmark index rose 0.5% to close at 4,985.5. The

Investment & Financial Services gained 2.9%, while the Insurance index was

up 2.4%. National Takaful Co. rose 9.6%, while Abu Dhabi National Insurance

Co. was up 7.7%.

##

GCC Top Losers

Exchange

Arab Banking Corp.

Bahrain

Kuwait: The KSE index was closed on February 26, 2014.

United Development

Qatar

Oman: The MSM index rose marginally to close at 7,102.8. Industrial Index

gained 0.1%, while all other sub indices ended in red. National Gas rose 9.7%,

while Al Sharqia Investment Holding was up 5.6%.

Emirates NBD

Gulf Warehousing Co.

Dar Al Arkan

#

Bahrain: The BHB index declined 0.6% to close at 1,377.5. The Investment

index fell 2.2%, while the Industrial was down 1.7%. Arab Banking Corporation

declined 7.1%, while Aluminum Bahrain was down 1.8%.

Qatar Exchange Top Gainers

Mesaieed Petrochemical Holding

Qatar General Ins. & Rein. Co.

YTD%

0.52

(7.1)

654.0

38.7

21.90

(4.2)

2,325.9

(3.1)

Dubai

8.05

(4.2)

162.4

26.8

Qatar

41.55

(3.1)

0.2

0.1

Saudi Arabia

11.85

(2.9)

71,661.4

20.3

Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

Close*

1D%

Vol. ‘000

YTD%

Close*

1D%

Vol. ‘000

YTD%

55.00

450.0

11,005.6

450.0

United Development Co.

21.90

(4.2)

2,325.9

(3.1)

Al Khaleej Takaful Group

37.25

(3.6)

5.9

2.1

49.30

4.7

0.5

2.9

Qatar Exchange Top Losers

67.50

Al Khaliji

4.3

26.8

26.9

Gulf Warehousing Co.

41.55

(3.1)

0.2

0.1

2.7

4.0

18.4

Salam International Investment

12.31

(3.0)

121.7

(5.4)

21.33

Mannai Corp.

2.6

46.4

6.7

QNB Group

193.30

(1.5)

262.0

12.4

Qatar Exchange Top Val. Trades

Close*

1D%

Val. ‘000

YTD%

55.00

450.0

674,414.7

450.0

197.00

(0.6)

94,369.0

16.6

21.90

(4.2)

51,225.9

(3.1)

193.30

(1.5)

50,923.5

12.4

32.45

(0.5)

27,475.3

8.9

Close*

1D%

Vol. ‘000

YTD%

Mesaieed Petrochemical Holding

55.00

450.0

11,005.6

450.0

United Development Co.

21.90

(4.2)

2,325.9

(3.1)

Barwa Real Estate Co.

32.45

(0.5)

844.2

8.9

Vodafone Qatar

12.20

0.1

590.7

13.9

Qatar Gas Transport Co.

21.72

(0.6)

569.6

7.3

Qatar Exchange Top Vol. Trades

Mesaieed Petrochemical Holding

Industries Qatar

United Development Co.

Qatar National Bank

Barwa Real Estate Co.

Source: Bloomberg (* in QR)

Source: Bloomberg (* in QR)

Qatar*

Dubai

Abu Dhabi

Saudi Arabia

Kuwait#

Oman

Bahrain

1D% Vol. ‘000

YTD%

106.40

Qatar Insurance Co.

Regional Indices

Close

Vol. ‘000

Close

1D%

WTD%

MTD%

YTD%

11,839.46

4,198.07

4,985.49

9,058.54

7,692.75

7,102.77

1,377.53

(0.1)

0.0

0.5

(0.0)

(0.5)

0.0

(0.6)

(0.3)

0.4

1.4

0.8

(0.6)

(0.9)

0.9

6.1

11.3

6.7

3.4

(0.8)

0.2

6.4

14.1

24.6

16.2

6.1

1.9

3.9

10.3

Exch. Val. Traded

($ mn)

298.29

416.88

138.86

2,234.02

93.35

25.38

2.26

Exchange Mkt.

Cap. ($ mn)

189,594.5

84,070.5

138,240.0

493,995.3

111,758.5

25,475.3

51,823.8

P/E**

P/B**

15.1

18.0

13.5

18.2

15.7

11.0

9.6

2.0

1.6

1.7

2.2

1.2

1.6

0.9

Dividend

Yield

4.0

1.9

3.6

3.3

3.7

3.6

3.5

Source: Bloomberg, Qatar Exchange, Tadawul, MSM, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any) (# Data as of February 24, 2014)

Page 1 of 6

2. Qatar Market Commentary

The QE index declined 0.1% to close at 11,839.5. The Real

Estate and Telecoms indices led the losses. The index rose on

the back of buying support from non-Qatari shareholders despite

selling pressure from Qatari shareholders.

Overall Activity

Sell %*

Net (QR)

Qatari

75.79%

79.62%

(41,611,053.22)

Non-Qatari

United Development Co. and Al Khaleej Takaful Group were the

top losers, falling 4.2% and 3.6% respectively. Among the top

gainers, Mesaieed Petrochemical Holding Co. rose 450.0%,

while Qatar General Ins. & Rein. Co. rose 4.7%.

Buy %*

24.21%

20.37%

41,611,053.22

Source: Qatar Exchange (* as a % of traded value)

Volume of shares traded on Wednesday rose by 41.2% to

18.7mn from 13.2mn on Tuesday. Further, as compared to the

30-day moving average of 13.0mn, volume for the day was

44.1% higher. Mesaieed Petrochemical Holding and United

Development Co. were the most active stocks, contributing

58.9% and 12.5% to the total volume respectively.

Earnings and Global Economic Data

Earnings Releases

Company

Revenue

(mn) 4Q2013

% Change

YoY

Operating Profit

(mn) 4Q2013

% Change

YoY

Net Profit (mn)

4Q2013

% Change

YoY

AED

716.6

28.7%

–

–

123.3

23.9%

Bahrain

BHD

17.3

35.9%

–

–

6.3

41.9%

Bahrain

BHD

4.5

-16.1%

–

–

1.0

-29.3%

Market

National Corporation for

Tourism and Hotels *

Bahrain Cinema Co. *

The Bahrain Ship Repairing

and Engineering Co. *

Currency

Abu Dhabi

Source: Company data, DFM, ADX, MSM (*FY2013 Results)

Global Economic Data

Date

Market

Source

Indicator

Period

Actual

Consensus

Previous

02/26

US

MBA

MBA Mortgage Applications

21-February

02/26

US

US Census Bureau

New Home Sales

January

-8.50%

–

-4.10%

468K

400K

02/26

US

US Census Bureau

New Home Sales MoM

January

427K

9.60%

-3.40%

-3.80%

02/26

Germany

GfK AG

GfK Consumer Confidence

March

8.5

8.2

8.3

02/26

UK

ONS

GDP QoQ

4Q2013

0.70%

0.70%

0.70%

02/26

UK

ONS

GDP YoY

4Q2013

2.70%

2.80%

2.80%

02/26

UK

ONS

Government Spending QoQ

4Q2013

0.30%

0.50%

0.60%

02/26

UK

ONS

Exports QoQ

4Q2013

0.40%

0.20%

-2.80%

02/26

UK

ONS

Imports QoQ

4Q2013

-0.90%

-1.00%

0.70%

02/26

UK

ONS

Index of Services MoM

December

0.20%

0.40%

0.50%

02/26

UK

ONS

Index of Services 3M/3M

December

0.80%

0.80%

0.90%

02/26

UK

ONS

Total Business Investment QoQ

4Q2013

2.40%

1.30%

2.00%

02/26

UK

ONS

Total Business Investment YoY

4Q2013

8.50%

–

-2.40%

02/26

Spain

INE

Total Mortgage Lending YoY

December

-26.30%

–

-26.90%

02/26

Spain

INE

House Mortgage Approvals YoY

December

-30.10%

–

-27.40%

02/26

Italy

ISTAT

Hourly Wages MoM

January

0.60%

–

0.00%

02/26

Italy

ISTAT

Hourly Wages YoY

January

1.40%

–

1.30%

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

News

Qatar

Qatar bourse to see QR5bn inflows after MSCI upgrade –

The Qatar Exchange (QE) expects as much as QR5bn worth of

foreign funds to flow in after its upgrade by MSCI to emerging

market status in June 2014. QE’s Acting Chairman Dr Hussain

Ali al-Abdullah said the bourse, which is slated to see more

listings in future, could soon witness the advent of exchange

traded funds. Dr Hussain added that around QR3bn to QR5bn is

expected to come from foreign investors to Qatar, after the

market upgrade. Last year, global index compiler MSCI had

upgraded Qatar and the UAE to emerging market from frontier

status. (Gulf-Times.com)

MPHC shares jump to QR55 on debut – Mesaieed

Petrochemical Holding Company (MPHC) shares witnessed

impressive buying interest, apparently from local retail investors.

MPHC constituted more than 60% of the bourse’s total value

traded yesterday. (Gulf-Times.com)

QNNS’ net income down 16% and 13% QoQ and YoY,

respectively – QNNS posted a net profit of QR172mn in

4Q2013, declining by 16% QoQ. One of the main reasons for

the drop in profitability was due to a slowdown in Milaha

Maritime & Logistics divisions. On the positive side, the

company declared a cash dividend of QR5.00/share (DY: 5.2%)

vs. QR3.50/share in 2012. (QNNS Press Release, QNBFS

Research)

Page 2 of 6

3. UDCD posts a net loss of QR183mn in 4Q2013 – The United

Development Company's (UDCD) posted a net loss of

QR183mn in 4Q2013. The loss is primarily due to loss from

share of associates. According to the 2013 annual report

footnote, “Middle East Dredging Company Q.S.C. (the

associate) is involved in project related dredging and

reclamation activities in the Gulf states and other neighboring

countries. The associate sustained losses relating to the Satah

Al Razboot (SARB) Project. The project has been characterized

by various delays and difficulties resulting in a cost overrun on

the part of the associate. The management of the associate has

submitted a claim to the counterparty in an effort to recover a

portion of the cost overruns and the settlement amount is under

negotiation. As a result the 45.9% equity holding in the

associate is impaired in full as at 31 December 2013”. We note

that the SARB project is based in Abu Dhabi and the carrying

value of the firm was QR263.8mn in 2012. For FY2013 UDCD’s

revenue reached QR2,081.3mn, down by 23.8% YoY as

compared to QR2,730.9mn in 2012. The company’s FY2013 net

profit decreased by 55.8% YoY to QR322.8mn. EPS amounted

to QR0.96 for 2013 as compared to QR2.17 in 2012. Meanwhile,

UDCD's board of directors has recommended a cash dividend of

10%, which translates into QR1.00 per share (same as last

year), in addition to 5% bonus shares. (QE, Gulf-Times.com)

AKHI posts net profit of QR66mn in 2013 – Al Khaleej Takaful

Group (AKHI) posted a net profit of QR66mn in 2013 vs.

QR78.2mn in 2012. EPS was QR3.87 in 2013 compared to

QR5.50 in 2012. The Board of Directors recommended 30%

bonus shares 30% with the results (QR1.00 and 20% stock

dividend in 2012). (QE)

QOIS posts net profit of QR19.8mn in 2013 – Qatar Oman

Investment Company (QOIS) posted a net profit of QR19.8mn

2013 vs. QR18.8mn in 2012. EPS was QR0.629 in 2013

compared to QR0.596 in 2012. The Board of Directors

recommended cash dividends of QR0.60 per share (QR0.50 in

2012). (QE)

QCB to issue T-bills worth QR4bn – The Qatar Central Bank

(QCB) will issue treasury bills for periods of three, six and nine

months on March 4, 2014. The total amount of issuance is worth

QR4bn. (QCB)

QEWS’ AGM approves 75% dividend – Qatar Electricity &

Water Company’s (QEWS) AGM approved the distribution of

profits of 75% dividend from the original share value. One bonus

share will be issued for every ten shares held. (QE)

CBQK’s AGM, EGM to be held on March 16 – The

Commercial Bank of Qatar’s (CBQK) announced that its AGM

and EGM will be held on March 16, 2014 at Commercial Bank

Plaza located on Al Markhiyah Street. The agenda includes

board’s approval for increasing the bank’s capital from

QR2,474.5mn to QR2,969.4mn by issuing one bonus share to

its shareholders for every five shares held, and authorize the

board to dispose of fractional shares. (QE)

ABQK approves agenda, 30% bonus shares – Ahli Bank’s

(ABQK) AGM has approved its board’s proposal to distribute

free shares among its shareholders by an amount of 30% of the

bank’s capital. Hence, ABQK approved increasing the bank’s

capital by adding 38,122,501 free shares, so that the capital

rises to 165,197,503 shares. (QE)

BRES closes candidacy for board membership for 20142016 – Barwa Real Estate Company’s (BRES) announced the

closure of nominations for its board of directors for the new term

of three years (2014-2016). (QE)

QGRI’s AGM, EGM to be held on March 16 – Qatar General

Insurance & Reinsurance Company (QGRI) announced that its

AGM and EGM are scheduled to be held on March 16, 2014.

The agenda includes the board’s proposal to increase the

company’s capital by 20% by giving bonus shares equivalent to

one new share for every five existing shares. With this, QGRI’s

capital will be raised to QR691.8mn from QR576.5mn. (QE)

Official holiday for Qatar Exchange on March 2 – The Qatar

Exchange (QE) will be closed on March 2, 2014 due to an

official holiday declared by the Qatar Central Bank. Trading on

the exchange will resume on March 3, 2014. (QE)

Lusail Expressway to be ready by 2016 – Ashghal’s Senior

Civil Engineer Mohamed Eissa Shamya said that the authority

has completed 18% of its overall work on the Lusail Expressway

project and expects it to be ready by 4Q2016. Shamya stated

that the project includes the reconstruction of the current Lusail

Expressway south of the former Arch roundabout to the northern

canal corridor. It consists of a 5.3-kilometer long four-lane

highway in addition to extra lanes to facilitate traffic between

intersections. The project includes three major interchanges: the

Wahda Interchange; the Onaiza Interchange, which will be a

complete free-flow interchange built on three levels; and the

Pearl Interchange that will become a three-level interchange to

provide a visually appealing access to Pearl Qatar. (GulfTimes.com)

International

UK recovery broadens due to long-awaited investment –

Britain's economic recovery broadened in the last three months

of 2013, driven by a pick-up in business investment and trade,

which will hearten the Bank of England and the government.

Consumer spending and a turnaround in the housing market

have been the main drivers behind Britain's surprisingly rapid

upturn, which started last year. However, recent data suggested

a more balanced recovery may be building, little more than a

year before a general election. The Office for National Statistics

said the UK’s GDP rose by 0.7% in the fourth quarter, which is

in line with forecasts and its earlier estimate. That rise capped

off the fastest rate of full-year growth since the financial crisis.

(Reuters)

French jobless figure rises to record in January – The

number of people out of work in France rose by 8,900 in

January to reach a record level, with President Francois

Hollande's goal of taming unemployment eluded him yet again.

The Labor Ministry’s data showed that the number of people

registered as jobless reached 3,316,200 in mainland France, up

0.3% MoM and 4.4% YoY. With this, Hollande's popularity has

plummeted to record lows, since he failed to live up to his

pledge to reduce unemployment by the end of 2013, in the face

of a weak recovery in the Eurozone's second-biggest economy.

(Reuters)

China lifts FC deposit rates cap in Shanghai FTZ – In a

move to further liberalize foreign currency (FC) deposits, China's

central bank said it will remove interest rate ceilings on smaller

foreign currency deposits in Shanghai Free Trade Zone (FTZ)

from March 1 as part of its long-anticipated financial reforms.

The People's Bank of China said deposits worth less than $3mn

owned by businesses and individuals registered in the FTZ will

receive the same rate of interest. Currently, regulatory caps

apply to one-year or other shorter-term deposits in US dollars,

Japanese yen, Euros and Hong Kong dollars. Deposits worth

more than $3mn are not subject to ceilings. Last year, China

launched the Shanghai FTZ as a part of its new set of fiscal

reforms to halt the slowdown and revitalize its economy. (ET)

Page 3 of 6

4. Regional

Saudi CMA approves ASLAK’s capital rise – The Saudi

CMA’s board has approved the United Wire Factories

Company’s (ASLAK) request to increase its capital from

SR390mn to SR438.8mn by issuing one bonus share for every

eight existing shares. This increase will be paid by transferring

an amount of SR48.8mn from the retained earnings account.

Consequently, the company's outstanding shares will increase

from 39mn to 43.9mn shares. Eligibility for the bonus shares is

limited to those shareholders who are registered at the close of

trading on the day of the extraordinary general assembly, which

will be determined later. (Tadawul)

AIG proposes SR129.7mn cash dividend for 2013 – Astra

Industrial Group’s (AIG) board of directors has proposed the

distribution of cash dividend worth SR129.7mn to its

shareholders for 2013. The dividend per share will be SR1.75,

representing 17.5% of the par value. Those shareholders who

are registered with the Securities Depository Center on the day

of the general assembly will be eligible for this dividend (to be

announced). (Tadawul)

Bahri receives dry bulk vessel Bahri Wafi – The National

Shipping Company of Saudi Arabia (Bahri) announced that its

subsidiary Bahri Dry Bulk has received a dry bulk vessel named

Bahri Wafi from a Japanese shipyard. This is the fourth vessel

delivered among the five vessels that were contracted in 2012.

These vessels have a capacity of 82,000dwt and a length of 229

meters, consuming less fuel and ecofriendly. The last vessel

under construction is expected to be delivered in 1H2014. The

financial impact of the delivered vessel will materialize during

1Q2014. (Tadawul)

APC declares SR204.99mn cash dividends for 2H2013 –

Advanced Petrochemical Company’s (APC) board of directors

approved to distribute cash dividends of SR204.99mn for

2H2013 by SR1.25 per share, which represents 12.5% of the

share capital. Shareholders who are registered with the

company at the end of trading on the day of the fifth

extraordinary general assembly shall be eligible for this

dividend. This brings the total earnings to SR368.89mn for the

year ended December 31, 2013, indicating SR2.25 per share.

(Tadawul)

SCCI: 96% of Sharjah firms optimistic – The Sharjah

Chamber of Commerce & Industry (SCCI), in collaboration with

Dun & Bradstreet, released the first Sharjah Chamber Business

Confidence Survey, which found that 96% of businesses in the

Emirate expect the overall business situation to either improve

or maintain its current level over the coming months. The

Sharjah Chamber Business Confidence Index stands at 137.6

points in 1Q2014, indicating positive and rising sentiments

among the business community. The Sharjah Chamber

Business Confidence Survey and its accompanying business

confidence indices are expected to become important tools for

businesses and policymakers to forecast the short-term

economic growth in the Emirate. (GulfBase.com)

UAE’s loan growth exceeds 7% in 2013 – According to the

UAE Central Bank, bank lending in the UAE grew 7.1% YoY in

2013. Bank loans grew at their fastest pace since 4Q2009,

reaching 7.1% YoY in December 2013. However, loans &

advances rose just 0.3% on a MoM basis after a big jump in

November. The acceleration in credit growth averaged 5.5%

through 2013 (compared with average 2.7% in 2012), providing

further evidence of the broader economic expansion in the UAE

last year, although private sector credit growth remains lower

than in Saudi Arabia and Qatar. (Bloomberg)

MAG Group invests AED15bn in UAE – Dubai-based MAG

Group said that it is investing up to AED15bn in Dubai and the

rest of the UAE. The group’s projects include a residential

development worth AED2bn, located in the Meydan district,

which features 106 townhouses and 29 five-storey apartment

buildings. MAG Group also expects to launch a AED750mn

residential project in Sharjah, a AED700mn Art Centre in Barsha

and a AED865mn City of Arabia residential project. (Bloomberg)

Cars Taxi enters Qatari market – Dubai-based Cars Taxi is set

to expand its operations by driving into Qatar in the next quarter.

Cars Taxi’s Group Executive Director Abdulla Sultan Al

Sabbagh said the company will start its operations in the Gulf

country in May 2014 with 300 taxis and will expand its fleet by

another 200 by the end of June. The company has operations in

Singapore, Malaysia, India and Bahrain. (Bloomberg)

Dubai launches 2 more Halal Zones – Economic Zones World

(EZW), in collaboration with Dubai Islamic Economy

Development Centre (DIEDC), announced a plan to develop two

Halal Zones, specifically designed to cater to the Halal product

markets. Earlier this week, Dubai Industrial City, a member of

Tecom Investments, also announced the launch of Halal Cluster

at Gulfood exhibition. (Bloomberg)

Arabtec denies plans to acquire Kuwait's Kharafi National –

Dubai-based builder Arabtec denied that it planned to acquire

Kuwaiti construction firm Kharafi National. According to sources,

Arabtec had been in talks with Kharafi National – a part of the

Kharafi Group – to fully acquire the company. (Reuters)

ADPC signs deal with Etihad Rail – Abu Dhabi Ports

Company (ADPC) has signed a deal with Etihad Rail to provide

the framework for an integrated bulk and container railway

terminal facility to be built at the Khalifa Port. The 1,200

kilometers long Etihad Rail network will complement ADPC’s

transportation and industrial infrastructure interlinking its

facilities, Khalifa Industrial Zone Abu Dhabi (Kizad) and the

adjacent Khalifa Port. After it is integrated with ADPC’s

infrastructure, the railway network will offer an enhanced

transportation system to logistics companies, combining sea,

road and rail transport. The network will also form a vital part of

a wider GCC railway network, connecting the UAE with Bahrain,

Kuwait, Oman, Qatar and Saudi Arabia. (Bloomberg)

HSBC Bank Oman approves CEO transition plans – HSBC

Bank Oman’s board of directors has approved the transition

plans for the bank’s Chief Executive Officer as part of the

succession plans for senior executives. Mr. Ewan Stirling will

take on a new role as Head of UK Transformation with the

HSBC Group based in London. A senior and well-experienced

successor has been identified from within the HSBC Group.

These appointments will be effective only on regulatory approval

and following HSBC Bank Oman’s Annual General Meeting.

(MSM)

BEDB: Bahrain attracts 35 foreign investments in 2013 –

Bahrain Economic Development Board (BEDB) revealed that 35

new international businesses established operations in the

Kingdom in 2013 as a result of direct outreach activities carried

out by the BEDB. This is in line with BEDB’s efforts to promote

Bahrain’s business environment and to attract more FDI to the

Kingdom. In 2013, the BEDB attracted $114mn worth of foreign

investment into the country from North America, Europe and

Asia – a 12% rise over 2012. This boost will help create around

800 jobs in the Kingdom over the next three years across a

range of sectors, including financial and professional services,

logistics, manufacturing and healthcare. (GulfBase.com)

Page 4 of 6

5. CINEMA declares 50% cash dividend – Bahrain Cinema

Company’s (CINEMA) board of directors has recommended a

cash dividend of 50% (20% bonus share) to its shareholders

who are registered on the date of the AGM & EGM. (Bahrain

Bourse)

Page 5 of 6

6. Rebased Performance

Daily Index Performance

180.0

170.0

160.0

150.0

140.0

130.0

120.0

110.0

100.0

90.0

80.0

1.0%

0.5%

0.5%

144.4

(0.0%)

(0.5%)

S&P Pan Arab

Dec-13

S&P GCC

Source: Bloomberg

Asset/Currency Performance

Gold/Ounce

Silver/Ounce

Crude Oil (Brent)/Barrel (FM

Future)

Natural Gas (Henry

Hub)/MMBtu

North American Spot LPG

Propane Price

North American Spot LPG

Normal Butane Price*

Euro

Source: Bloomberg (*Market Closed on February 26, 2014)

Close ($)

1D%

WTD%

YTD%

1,330.57

(0.8)

0.5

10.4

21.24

(2.8)

(2.8)

9.1

109.52

0.0

(0.3)

4.84

(7.3)

116.75

Global Indices Performance

Close

1D%

WTD%

YTD%

16,198.41

0.1

0.6

(2.3)

S&P 500

1,845.16

0.0

0.5

(0.2)

(1.2)

NASDAQ 100

4,292.06

0.1

0.7

2.8

(22.1)

11.4

STOXX 600

337.70

(0.2)

0.5

2.9

(3.7)

(13.7)

(7.7)

DAX

9,661.73

(0.4)

0.0

1.1

123.00

0.0

(4.3)

(9.4)

FTSE 100

6,799.15

(0.5)

(0.6)

0.7

DJ Industrial

1.37

(0.4)

(0.4)

(0.4)

CAC 40

102.38

0.1

(0.1)

(2.8)

Nikkei

GBP

1.67

(0.1)

0.3

0.7

MSCI EM

CHF

1.12

(0.4)

(0.3)

0.3

SHANGHAI SE Composite

AUD

0.90

(0.6)

(0.1)

0.6

USD Index

80.43

0.4

0.2

RUB

36.02

1.0

1.4

BRL

0.43

(0.4)

(0.2)

0.6

Yen

Dubai

May-13

Oman

Oct-12

Abu Dhabi

QE Index

Mar-12

(0.6%)

Bahrain

Aug-11

(0.1%)

Kuwait *

(1.0%)

Jan-11

0.0%

0.0%

0.0%

0.0%

Qatar

131.5

Saudi Arabia

Jun-10

170.1

4,396.91

(0.4)

0.4

2.4

14,970.97

(0.5)

0.7

(8.1)

956.26

0.1

(0.3)

(4.6)

2,041.25

0.3

(3.4)

(3.5)

HANG SENG

22,437.44

0.5

(0.6)

(3.7)

0.5

BSE SENSEX

20,986.99

0.6

1.4

(0.9)

9.6

Bovespa

46,599.21

(0.2)

(1.6)

(9.5)

1,286.07

(1.6)

(2.2)

(10.9)

Source: Bloomberg (*Market closed on February 26, 2014)

RTS

Source: Bloomberg

Contacts

Saugata Sarkar

Ahmed M. Shehada

Keith Whitney

Sahbi Kasraoui

Head of Research

Head of Trading

Head of Sales

Manager - HNWI

Tel: (+974) 4476 6534

Tel: (+974) 4476 6535

Tel: (+974) 4476 6533

Tel: (+974) 4476 6544

saugata.sarkar@qnbfs.com.qa

ahmed.shehada@qnbfs.com.qa

keith.whitney@qnbfs.com.qa

sahbi.alkasraoui@qnbfs.com.qa

QNB Financial Services SPC

Contact Center: (+974) 4476 6666

PO Box 24025

Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 6 of 6