QNBFS Daily Technical Trader Qatar - September 07, 2023 التحليل الفني اليومي ...

1 June Daily market report

1. Page 1 of 5

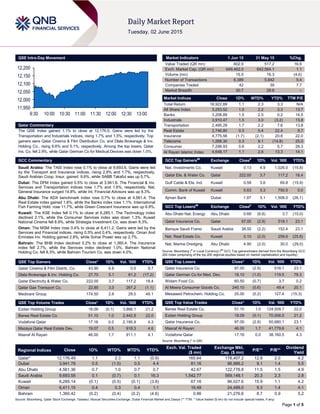

QSE Intra-Day Movement

Qatar Commentary

The QSE Index gained 1.1% to close at 12,176.5. Gains were led by the

Transportation and Industrials indices, rising 1.7% and 1.5%, respectively. Top

gainers were Qatar Cinema & Film Distribution Co. and Dlala Brokerage & Inv.

Holding Co., rising 6.6% and 5.1%, respectively. Among the top losers, Qatar

Ins. Co. fell 2.9%, while Qatar German Co for Medical Devices was down 1.0%.

GCC Commentary

Saudi Arabia: The TASI Index rose 0.1% to close at 9,693.6. Gains were led

by the Transport and Insurance indices, rising 2.9% and 1.7%, respectively.

Saudi Arabian Coop. Insur. gained 9.6%, while SABB Takaful was up 5.7%.

Dubai: The DFM Index gained 0.5% to close at 3,941.8. The Financial & Inv.

Services and Transportation indices rose 1.7% and 1.6%, respectively. Nat.

General Insurance surged 14.8%, while Int. Financial Advisors was up 8.3%.

Abu Dhabi: The ADX benchmark index rose 0.7% to close at 4,561.4. The

Real Estate index gained 1.8%, while the Banks index rose 1.1%. International

Fish Farming Hold. rose 11.7%, while Green Crescent Insurance was up 6.9%.

Kuwait: The KSE Index fell 0.1% to close at 6,285.1. The Technology index

declined 2.1%, while the Consumer Services index was down 1.3%. Kuwait

National Cinema fell 8.9%, while Strategia Investment Co. was down 8.3%.

Oman: The MSM Index rose 0.4% to close at 6,411.2. Gains were led by the

Services and Financial indices, rising 0.5% and 0.4%, respectively. Oman And

Emirates Inv. Holding gained 2.8%, while Sohar Power was up 2.7%.

Bahrain: The BHB Index declined 0.2% to close at 1,360.4. The Insurance

index fell 2.7%, while the Services index declined 1.0%. Bahrain National

Holding Co. fell 8.3%, while Bahrain Tourism Co. was down 4.0%.

QSE Top Gainers Close* 1D% Vol. ‘000 YTD%

Qatar Cinema & Film Distrib. Co. 43.90 6.6 0.5 9.7

Dlala Brokerage & Inv. Holding Co. 27.70 5.1 81.2 (17.2)

Qatar Electricity & Water Co. 222.00 3.7 117.2 18.4

Qatar Gas Transport Co. 22.85 3.0 267.2 (1.1)

Medicare Group 174.50 2.6 29.0 49.1

QSE Top Volume Trades Close* 1D% Vol. ‘000 YTD%

Ezdan Holding Group 18.09 (0.1) 3,866.1 21.2

Barwa Real Estate Co. 51.10 1.0 2,442.9 22.0

Vodafone Qatar 17.16 0.0 2,195.9 4.3

Mazaya Qatar Real Estate Dev. 19.07 0.5 918.3 4.6

Masraf Al Rayan 46.00 1.7 911.1 4.1

Market Indicators 1 Jun 15 31 May 15 %Chg.

Value Traded (QR mn) 602.9 517.2 16.6

Exch. Market Cap. (QR mn) 649,462.0 642,564.1 1.1

Volume (mn) 15.5 16.3 (4.6)

Number of Transactions 6,389 5,842 9.4

Companies Traded 42 39 7.7

Market Breadth 30:7 28:8 –

Market Indices Close 1D% WTD% YTD% TTM P/E

Total Return 18,922.89 1.1 2.3 3.3 N/A

All Share Index 3,253.52 1.0 2.2 3.3 13.7

Banks 3,208.89 1.5 2.5 0.2 14.5

Industrials 3,910.47 1.5 3.0 (3.2) 13.8

Transportation 2,495.29 1.7 2.2 7.6 13.8

Real Estate 2,746.80 0.5 0.4 22.4 9.7

Insurance 4,775.56 (1.7) (2.1) 20.6 22.0

Telecoms 1,266.30 0.3 8.1 (14.8) 25.0

Consumer 7,298.93 0.6 2.2 5.7 28.3

Al Rayan Islamic Index 4,648.17 1.1 2.6 13.3 14.1

GCC Top Gainers##

Exchange Close#

1D% Vol. ‘000 YTD%

Nat. Investments Co. Kuwait 0.13 4.9 1,026.0 (15.8)

Qatar Ele. & Water Co. Qatar 222.00 3.7 117.2 18.4

Gulf Cable & Ele. Ind. Kuwait 0.58 3.6 69.8 (15.9)

Comm. Bank of Kuwait Kuwait 0.63 3.3 750.5 0.0

Ajman Bank Dubai 1.97 3.1 1,508.0 (26.1)

GCC Top Losers##

Exchange Close#

1D% Vol. ‘000 YTD%

Abu Dhabi Nat. Energy Abu Dhabi 0.68 (6.8) 3.7 (15.0)

Qatar Insurance Co. Qatar 97.00 (2.9) 518.1 23.1

Banque Saudi Fransi Saudi Arabia 38.55 (2.2) 152.4 23.1

Nat. Real Estate Co. Kuwait 0.10 (2.0) 258.6 (25.8)

Nat. Marine Dredging Abu Dhabi 4.90 (2.0) 30.0 (29.0)

Source: Bloomberg (

#

in Local Currency) (

##

GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

QSE Top Losers Close* 1D% Vol. ‘000 YTD%

Qatar Insurance Co. 97.00 (2.9) 518.1 23.1

Qatar German Co for Med. Dev. 18.10 (1.0) 119.5 78.3

Widam Food Co. 60.50 (0.7) 3.7 0.2

Al Meera Consumer Goods Co. 240.10 (0.6) 49.4 20.1

Mesaieed Petrochem. Holding Co. 25.00 (0.2) 127.4 (15.3)

QSE Top Value Trades Close* 1D% Val. ‘000 YTD%

Barwa Real Estate Co. 51.10 1.0 124,508.7 22.0

Ezdan Holding Group 18.09 (0.1) 70,006.5 21.2

Qatar Insurance Co. 97.00 (2.9) 50,680.1 23.1

Masraf Al Rayan 46.00 1.7 41,779.6 4.1

Vodafone Qatar 17.16 0.0 38,160.5 4.3

Source: Bloomberg (* in QR)

Regional Indices Close 1D% WTD% MTD% YTD%

Exch. Val. Traded

($ mn)

Exchange Mkt.

Cap. ($ mn)

P/E** P/B**

Dividend

Yield

Qatar* 12,176.49 1.1 2.3 1.1 (0.9) 165.64 178,407.2 12.8 2.0 4.2

Dubai 3,941.78 0.5 (1.5) 0.5 4.4 81.16 96,986.2 9.1 1.4 5.5

Abu Dhabi 4,561.36 0.7 1.0 0.7 0.7 42.67 122,776.8 11.5 1.5 4.9

Saudi Arabia 9,693.58 0.1 (0.7) 0.1 16.3 1,542.77 569,148.1 20.3 2.3 2.8

Kuwait 6,285.14 (0.1) (0.5) (0.1) (3.8) 67.16 96,027.6 15.9 1.1 4.2

Oman 6,411.15 0.4 0.3 0.4 1.1 16.48 24,489.0 9.3 1.4 4.1

Bahrain 1,360.42 (0.2) (0.4) (0.2) (4.6) 0.86 21,276.6 8.7 0.9 5.2

Source: Bloomberg, Qatar Stock Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

11,950

12,000

12,050

12,100

12,150

12,200

9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

2. Page 2 of 5

Qatar Market Commentary

The QSE Index gained 1.1% to close at 12,176.5. The

Transportation and Industrials indices led the gains. The index

rose on the back of buying support from non-Qatari shareholders

despite selling pressure from Qatari and GCC shareholders.

Qatar Cinema & Film Distribution Co. and Dlala Brokerage &

Investments Holding Co. were the top gainers, rising 6.6% and

5.1%, respectively. Among the top losers, Qatar Insurance Co.

fell 2.9%, while Qatar German Co for Medical Devices was down

1.0%.

Volume of shares traded on Monday fell by 4.6% to 15.5mn from

16.3mn on Sunday. Further, as compared to the 30-day moving

average of 16.2mn, volume for the day was 3.8% lower. Ezdan

Holding Group and Barwa Real Estate Co. were the most active

stocks, contributing 24.9% and 15.7% to the total volume,

respectively.

Source: Qatar Stock Exchange (* as a % of traded value)

Ratings and Global Economic Data

Ratings Updates

Company Agency Market Type* Old Rating New Rating Rating Change Outlook Outlook Change

Qatar Islamic Insurance

Company (QISI)

Moody's Qatar IFSR Baa2 Baa1 Stable –

Source: News reports (* LT – Long Term, ST – Short Term, FSR- Financial Strength Rating, FCR – Foreign Currency Rating, LCR – Local Currency Rating, IDR – Issuer Default Rating, SR – Support Rating, LC

– Local Currency, IFSR – Insurance Financial Strength Rating)

Global Economic Data

Date Market Source Indicator Period Actual Consensus Previous

06/01 US Bureau of Eco. Analysis Personal Income April 0.40% 0.30% 0.00%

06/01 US Bureau of Eco. Analysis Personal Spending April 0.00% 0.20% 0.50%

06/01 US Bureau of Eco. Analysis PCE Deflator YoY April 0.10% 0.20% 0.30%

06/01 US Bureau of Eco. Analysis PCE Core YoY April 1.20% 1.40% 1.30%

06/01 US Census Bureau Construction Spending MoM April 2.20% 0.80% 0.50%

06/01 Germany Destatis CPI MoM May 0.10% 0.10% 0.00%

06/01 Germany Destatis CPI YoY May 0.70% 0.70% 0.50%

06/01 Germany Destatis CPI EU Harmonized MoM May 0.10% 0.10% -0.10%

06/01 Germany Destatis CPI EU Harmonized YoY May 0.70% 0.60% 0.30%

06/01 UK Markit Markit UK PMI Manufacturing SA May 52.0 52.5 51.8

06/01 Spain Markit Markit Spain Manufacturing PMI May 55.8 54.5 54.2

06/01 Italy Markit Markit/ADACI Italy Manufacturing PMI May 54.8 53.6 53.8

06/01 Italy ANFIA New Car Registrations YoY May 10.78% – 24.16%

06/01 Italy Italian Treasury Budget Balance May -4.3B – -6.0B

06/01 China China Fed. of Logistics Manufacturing PMI May 50.2 50.3 50.1

06/01 China China Fed. of Logistics Non-manufacturing PMI May 53.2 – 53.4

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

News

Qatar

QSE, CBQK working together to empower SMEs in Qatar –

The Qatar Stock Exchange (QSE) and the Commercial Bank

(CBQK) have jointly held a workshop for SMEs (small and

medium-sized enterprises) about opportunities to list on the

Qatar Exchange Venture Market (QEVM). The workshop

highlighted growth opportunities for SMEs seeking to be part of

the QEVM, which joins the QSE Main Market, and provides a

revolutionary new platform for SMEs to pursue their

entrepreneurial visions and also benefit from access to capital

through listing. According to QSE CEO Rashid bin Ali Al-

Mansoori, QEVM is all set to welcome SMEs from the wider Gulf

Cooperation Council (GCC) and Middle East & North Africa

(Mena) regions as well. (QSE)

Moody's upgrades QISI’s IFSR, outlook stable – Moody's

Investors Service has upgraded the insurance financial strength

rating (IFSR) of Qatar Islamic Insurance Company (QISI) to

Baa1 from Baa2. The rating carries a stable outlook. The rating

upgrade for QISI reflects its improved and extremely strong

capitalization in relation to insurance risk and its sustained

strong profitability both in terms of underwriting profit and

bottom-line. On the other hand, Moody's said that QISI

maintains a significant level of investment risk, as it invests

predominantly in Qatari equity and property markets.

Furthermore, QISI's insurance risk remains relatively

concentrated in Qatar thus exposing it to geographic

concentration risk and reliance on the Qatar’s economic

performance. Both of these factors constrain the company's

ratings over time. (Bloomberg)

Overall Activity Buy %* Sell %* Net (QR)

Qatari 51.56% 69.08% (105,659,904.40)

GCC 5.49% 6.14% (3,914,670.70)

Non-Qatari 42.95% 24.78% 109,574,575.10

3. Page 3 of 5

QDF signs MoU with Nebras Power – Qatar Development

Fund (QDF) and Nebras Power Company have signed a MoU to

develop cooperation while studying investment opportunities

related to energy projects in countries that will be agreed upon.

The MoU aims to develop a general framework and to determine

the guidelines on which both parties will cooperate to study the

investment opportunities. (QSE)

MDPS: Qatar population reaches all-time high in May –

According to figures released by the Ministry of Development

Planning & Statistics (MDPS), Qatar’s population has reached

an all-time high of 2,374,860 based on the number of people

present in the country on May 31. The country’s population

increased by approximately 200,000 people from 2,174,055 on

May 31, 2014, while it was up by around 32,000 from 2,342,725

on April 30, 2015. (Gulf-Times.com)

GDI appoints new CEO – Gulf Drilling International (GDI), a

wholly owned subsidiary of Gulf International Services, has

appointed Mr. Mubarak Awaida Al-Hajri as its new CEO with

effect from June 14, 2015. Mr. Al-Hajri has a long experience

with Qatar Petroleum, where he worked way up through different

disciplines and management levels. (QSE)

Philadelphia to be first QA’s A350 XWB route in US – Qatar

Airways (QA), the global launch customer of the A350 XWB, has

announced that Philadelphia will be the first destination it will fly

to in the US using the state-of-the-art aircraft. The Doha-based

airline plans to begin operating an A350 on its daily service from

Doha’s Hamad International Airport to Philadelphia International

Airport from January 1, 2016. The date will coincide with the

launch of services to Los Angeles, one of the three new QA

destinations in the US for 2016. (Gulf-Times.com)

International

US consumer spending stalls in April; factory activity

improves in May – The US consumer spending growth

unexpectedly stalled in April as households cut back on

purchases of automobiles and continued to boost savings,

suggesting the economy was struggling to gain momentum early

in 2Q2015. The Commerce Department said that consumer

spending remained unchanged in April as compared with

analysts' forecasts for a 0.2% rise and followed by a 0.5%

increase in March. Consumer spending was also curbed by

weak demand for utilities such as electricity and natural gas as

temperatures warmed up. Meanwhile, the Institute for Supply

Management said its national factory activity index rose to 52.8

in May from 51.5 in April. The index was boosted by a surge in

new orders and factory employment. (Reuters)

Eurozone factory growth weaker in May than initially

reported – Markit Economics said that its factory PMI for the

entire 19-nation euro region rose to 52.2 in May from 52 in April.

While that is above the key 50 mark that divides expansion from

contraction, it is below the initially reported reading of 52.3.

Markit’s report showed that input costs at factories across the

region are rising by the most in three years, while selling prices

are stagnating, squeezing companies’ margins. In Germany, the

index fell more than initially reported, dropping to 51.1 from 52.1.

France’s PMI remained below 50. On the other hand, the PMI

for Italy rose to 54.8 from 53.8 in April, the highest since 2011,

while the Spanish measure jumped to 55.8 from 54.2.

Production and new order growth in Italy was the fastest in over

four years while output and new orders rose at the quickest

pace in Spain since 2007 as new export business jumped the

most in 15 years. (Bloomberg)

UK domestic demand drives factory pick-up as exports stall

– According to a report by Markit Economics, UK manufacturing

expanded in May as the factory PMI rose to 52 from a revised

51.8 in April. The report highlighted Britain’s reliance on

domestic demand while an economic recovery has yet to gain

momentum in Europe, its biggest trading partner. Domestic

demand also fueled a pick-up in new orders, whereas export

orders were little changed in May following a drop in the

previous month. Manufacturers raised average selling prices for

the first time in five months, while input costs fell. (Bloomberg)

WB raises 2015, 2016 growth forecasts for Russia – The

World Bank (WB) said on Monday that it expects Russia's

economy to contract less sharply than previously thought in

2015, citing a recovery in oil prices in recent months, a stronger

ruble and slowing inflation. The bank forecasted Russia’s GDP

to fall by 2.7% in 2015 as opposed to 3.8% estimated earlier.

The WB also raised growth forecast for 2016 to 0.7% while the

economy is expected to expand by 2.5% in 2017. The WB's lead

economist for Russia, Birgit Hansl said that the changed

conditions would allow the central bank to ease monetary policy

at a faster rate this year, supporting the economy. However, the

outlook for the Russian economy remained uncertain. (Reuters)

Indian factory growth accelerates in May – According to a

survey by HSBC, Indian manufacturing sector grew at its fastest

pace in four months in May on improved domestic demand,

even as input costs remained high and firms adopted a cautious

approach on hiring. The HSBC/Markit PMI surged to 52.6 in

May, from 51.3 in April, with levels of production and new orders

rising at the fastest rates since January 2015. The data shows

that manufacturing sector has been growing for 19 consecutive

months now. (Economic Times)

Regional

Sipchem starts commercial operations at cable insulation

plant – Saudi International Petrochemical Company (Sipchem)

has begun commercial production at the cable insulation

polymers plant of its affiliate Gulf Advanced Cables Insulation

Company. The plant is located in Sipchem’s complex in Jubail

Industrial City and produces several types of cable insulation

polymers, which are used for fabricating electrical cable

insulation materials. (Tadawul)

KHI sells 50% stake in Mauritius resort to Sun Resorts –

Kingdom Hotel Investments (KHI), a wholly-owned subsidiary of

Kingdom Holding Company (KHC), has sold 50% stake in Four

Seasons Resort Mauritius to its joint venture partner, Sun

Resorts. (Reuters)

Al Hammadi completes selling fractions shares – Al

Hammadi Development & Investment Company (Al Hammadi)

has completed the selling of 33,634 fractions shares arising out

of the company's capital increase. The company had sold the

shares on May 6, 2015 for a value of SR2.1mn at an average

price of SR62.27 per share. Meanwhile, the Samba Financial

Group will deposit the fractional shares’ amount into the

company shareholders’ accounts on June 2, 2015. (Tadawul)

Saudi CMA approves Bahri’s Sukuk issue – The Saudi

Capital Market Authority (CMA) has approved the offering of the

National Shipping Company of Saudi Arabia's (Bahri) Sukuk

issue. The offering size will be determined later by the company,

and the prospectus will be released to the public in due course.

(GulfBase.com)

Dur Hospitality plans to invest SR1.5bn in hospitality,

residential projects – Saudi-based property & hotel developer,

Dur Hospitality Company, is planning to invest SR1.5bn in a

portfolio of 20 hotels and six residential complexes in the

Kingdom, over the next seven years. The company is further

planning to expand into emerging cities in Saudi Arabia such as

4. Page 4 of 5

Jubail, Yunbu and Tabuk; and has announced its first Holiday

Inn in Tabuk – the first hotel to be developed under the master

development agreement (MDA) inked between InterContinental

Hotel Group (IHG) and Dur Hospitality in 2014. (GulfBase.com)

IHG signs agreement with Al Majd to build world's largest

Holiday Inn in Makkah – InterContinental Hotels Group (IHG)

has signed an agreement with property developer Al Majd Al

Arabiah Company for the construction of the world’s largest

Holiday Inn hotel in Makkah, Saudi Arabia. The 5,154-room

Holiday Inn, Makkah Abraaj Al Tayseer, will open in Makkah in

2015 at the site where the current Abraaj Al Tayseer pilgrim

accommodation is located. The property is slated to open in

phases, with nearly 1,650 rooms across two towers expected to

open by 2015-end, while the remaining 3,500 rooms are slated

to open over the following three years. (GulfBase.com)

WEC: UAE’s nuclear energy projects to be delivered on

time – Jeffrey Benjamin, Senior Vice President of Nuclear

Power Plants at the US-based Westinghouse Electric Company

(WEC) said that the UAE’s nuclear energy projects, developed

by Emirates Nuclear Energy Company (ENEC), are making

progress with the reactors expected to be delivered on time. He

said that falling oil prices are not going to compromise focus on

nuclear energy, since fossil fuel prices tend to fluctuate often,

while that of nuclear and renewable energy are more stable.

(GulfBase.com)

DSE Oman wins several contracts worth AED350mn in

Oman – Drake & Scull Engineering Oman (DSE Oman), a

subsidiary of Drake & Scull International (DSI), has been

awarded several contracts worth a total of AED350mn. Under

the terms of the agreement, DSE Oman will deliver mechanical,

electrical and plumbing (MEP) works for the Oman Convention

and Exhibition Centre (OCEC) in Seeb, two hotels in Saraya

Bandar Jissah near Muscat, and an airport hangar related

facility. The project, which is expected to begin soon, is

scheduled to be completed by 2017. Moreover, DSE Oman will

undertake the supply, installation, testing and commissioning of

core MEP systems for two of the 5-star beachfront properties at

Saraya Bandar Jissah, near Muscat. The two hotels are

expected to be handed over by 2017 and 2016, respectively.

Additionally, DSE Oman will start work on the supply,

installation, testing and commissioning of low side heating,

ventilating and air conditioning (HVAC) and plumbing work for

an airport hangar related facility on an accelerated basis, with an

aim to complete the project work by early-2016. (DFM)

Dubai FDI signs MoU with TEC – The Dubai Investment

Development Corporation (Dubai FDI) has signed a MoU with

the Tunisia Economic City (TEC) to share knowledge and

expertise on the economic development strategies and attract

foreign investment. The MoU is part of the Dubai FDI’s effort to

facilitate investment inflows and support businesses in order to

expand to new markets through Dubai. (GulfBase.com)

Emaar Misr scales back pricing of Egyptian IPO – Emaar

Misr, the Egypt-based subsidiary of Emaar Properties, has

scaled back the price of its listing of 600mn shares on the

Egyptian bourse to $353mn from an earlier $367mn. The Emaar

listing is expected to be the largest flotation on the Cairo

exchange since 2007. Meanwhile, the Egyptian subsidiary has a

portfolio of investments in Egypt worth around $6.95bn.

According to the Egyptian newspapers, the shares will be priced

at a maximum of EGP4.49 each, which means that the offer is

expected to raise EGP2.69bn. The company had previously

aimed to price the shares at EGP4.70 each. (GulfBase.com)

ADGM signs MoU with DED – Abu Dhabi Global Market

(ADGM) has signed a MoU with the Abu Dhabi Department of

Economic Development (DED). The MoU provides a framework

for cooperation and collaboration between the two parties,

particularly regarding respective policies, company registrations,

licensing and regulatory matters, alongside statistics and

information sharing. (GulfBase.com)

Abu Dhabi Ports signs AED130mn Musataha agreement

with SIDDCO Group for engineering facility – Abu Dhabi

Ports and the UAE-based SIDDCO Group have signed a

Musataha agreement worth AED130mn to set up an engineering

facility at Khalifa Port’s industrial zone (Kizad). The new facility

branded as ‘iNGENIUM’ is spread over an area of 122,000

square meters, and will deliver precision automated engineering

and fabrication for the regional oil & gas sector. (GulfBase.com)

Danah shareholders approve withholding 2014 dividend –

Shareholders of the Danah Al Safat Foodstuff Company’s have

approved withholding of the dividend payout for 2014. The

shareholders also approved to offset its previous losses, which

would be financed through reserves. (GulfBase.com)

GEC refuses Muscat Municipality’s settlement offer for

Muscat Expressway projects – Galfar Engineering &

Contracting (GEC) has received an offer letter from Muscat

Municipality regarding the settlement of Muscat Express Way

and Central Corridor road projects. Based on an independent,

detailed technical and legal advice, GEC’s board has decided

not to accept the offer and to pursue other options for the way

forward. (MSM)

ONICH, Ominvest get shareholders’ nod for merger –

Respective shareholders at the Oman International

Development & Investment Company (Ominvest) and Oman

National Investment Corporation Holding’s (ONICH) have

approved the proposed merger of the two companies. As per the

plan, ONICH shareholders would receive 1.052 Ominvest

shares for each share they held currently. Meanwhile,

Ominvest’s shareholders had backed the plan to increase its

authorized capital to OMR90mn from OMR50mn, and its issued

capital to OMR55.28mn from OMR37.04mn. (MSM)

Oman increases mining royalty rates to 10% from July 2015

– The Public Authority for Mining in Oman has decided to

increase mining royalty rates to 10% from 5%, effective July 1,

2015. (GulfBase.com)

CBB’s new ISLI to enhance ASBB’s activities and boost

profitability – Al Salam Bank-Bahrain (ASBB) Director and

Group CEO Yousif Taqi said that the new Islamic Sukuk

Liquidity Instrument (ISLI), which is recently introduced by the

Central Bank of Bahrain (CBB), will play a vital role in enhancing

return for ASBB and boost its profitability, as well as contributing

toward Bahrain’s overall national economic development. (DFM)

5. Contacts

Saugata Sarkar Sahbi Kasraoui QNB Financial Services SPC

Head of Research Head of HNI Contact Center: (+974) 4476 6666

Tel: (+974) 4476 6534 Tel: (+974) 4476 6544 PO Box 24025

saugata.sarkar@qnbfs.com.qa sahbi.alkasraoui@qnbfs.com.qa Doha, Qatar

Disclaimer and Copyright Notice: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of QNB SAQ (“QNB”). QNBFS is regulated by the

Qatar Financial Markets Authority and the Qatar Exchange QNB SAQ is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is

not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. QNBFS accepts no liability

whatsoever for any direct or indirect losses arising from use of this report. Any investment decision should depend on the individual circumstances of the investor and be based on specifically

engaged investment advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report

has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. QNBFS does not make any

representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. For reports dealing with Technical Analysis,

expressed opinions and/or recommendations may be different or contrary to the opinions/recommendations of QNBFS Fundamental Research as a result of depending solely on the historical

technical data (price and volume). QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment

decisions that differ significantly from, or even contradict, the views and opinions included in this report. This report may not be reproduced in whole or in part without permission from QNBFS

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 5 of 5

Rebased Performance Daily Index Performance

Source: Bloomberg Source: Bloomberg

Source: Bloomberg Source: Bloomberg (*$ adjusted returns)

80.0

100.0

120.0

140.0

160.0

180.0

200.0

220.0

May-11 May-12 May-13 May-14 May-15

QSE Index S&P Pan Arab S&P GCC

0.1%

1.1%

(0.1%)

(0.2%)

0.4%

0.7%

0.5%

(0.5%)

0.0%

0.5%

1.0%

1.5%

SaudiArabia

Qatar

Kuwait

Bahrain

Oman

AbuDhabi

Dubai

Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D%* WTD%* YTD%*

Gold/Ounce 1,189.10 (0.1) (0.1) 0.4 MSCI World Index 1,778.28 (0.1) (0.1) 4.0

Silver/Ounce 16.77 0.1 0.1 6.8 DJ Industrial 18,040.37 0.2 0.2 1.2

Crude Oil (Brent)/Barrel (FM

Future)

64.88 (1.0) (1.0) 13.2 S&P 500 2,111.73 0.2 0.2 2.6

Crude Oil (WTI)/Barrel (FM

Future)

60.20 (0.2) (0.2) 13.0 NASDAQ 100 5,082.93 0.3 0.3 7.3

Natural Gas (Henry

Hub)/MMBtu

2.60 (1.6) (1.6) (13.2) STOXX 600 400.57 (0.3) (0.3) 5.5

LPG Propane (Arab Gulf)/Ton 45.38 2.8 2.8 (7.4) DAX 11,436.05 (0.3) (0.3) 4.8

LPG Butane (Arab Gulf)/Ton 58.00 2.7 2.7 (7.6) FTSE 100 6,953.58 (1.0) (1.0) 3.2

Euro 1.09 (0.5) (0.5) (9.7) CAC 40 5,025.30 (0.1) (0.1) 6.1

Yen 124.77 0.5 0.5 4.2 Nikkei 20,569.87 (0.6) (0.6) 12.8

GBP 1.52 (0.6) (0.6) (2.4) MSCI EM 1,002.93 (0.1) (0.1) 4.9

CHF 1.06 (0.6) (0.6) 5.1 SHANGHAI SE Composite 4,828.74 4.6 4.6 49.5

AUD 0.76 (0.5) (0.5) (7.0) HANG SENG 27,597.16 0.6 0.6 16.9

USD Index 97.39 0.5 0.5 7.9 BSE SENSEX 27,848.99 0.2 0.2 0.7

RUB 53.57 2.4 2.4 (11.8) Bovespa 53,031.32 0.5 0.5 (11.7)

BRL 0.32 0.3 0.3 (16.4) RTS 953.88 (1.5) (1.5) 20.6

175.0

141.9

128.6