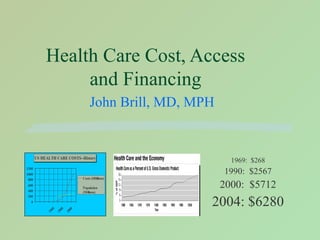

7. Approximately how much was spent on health care in the United States in 2004? A. $1.9 Billion B . $19 Billion C. $190 Billion D . $1.9 Trillion

8. What % of the United States Gross Domestic Product (GDP) is spent on health care? A. 6% B. 11% C. 16% D. 21% E. 26%

9. According to health care economist Victor Fuchs [JAMA 269 631 (1993)] and other experts, which of the following is most responsible for the high costs of health care in the US? A . Treating ‘hopeless’ cases at the end of life B . Americans’ demand for the best care available C . Malpractice and ‘defensive medicine’ D. Fraud and Abuse in health care

41. In the 1980s the U.S. auto manufacturers started to pay more for healthcare for their employees per car, than steel per car . In 1996 GM paid $1200 in health costs per car, and foreign auto manufacturers spend as little as $100, due to younger, healthier workers, and lack of retirees. Kleinke, J.D., The Bleeding Edge ,

![Goals ,[object Object],[object Object],[object Object]](data:image/gif;base64,R0lGODlhAQABAIAAAAAAAP///yH5BAEAAAAALAAAAAABAAEAAAIBRAA7)