Recommended

More Related Content

What's hot

What's hot (17)

Similar to Dissolution of the firm

Similar to Dissolution of the firm (20)

Recently uploaded

Recently uploaded (20)

Dissolution of the firm

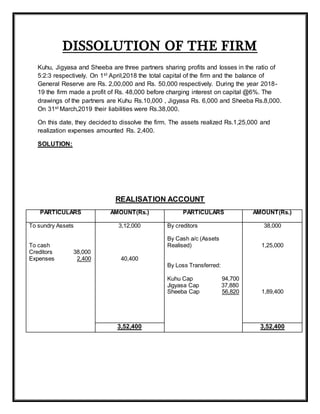

- 1. DISSOLUTION OF THE FIRM Kuhu, Jigyasa and Sheeba are three partners sharing profits and losses in the ratio of 5:2:3 respectively. On 1st April,2018 the total capital of the firm and the balance of General Reserve are Rs. 2,00,000 and Rs. 50,000 respectively. During the year 2018- 19 the firm made a profit of Rs. 48,000 before charging interest on capital @6%. The drawings of the partners are Kuhu Rs.10,000 , Jigyasa Rs. 6,000 and Sheeba Rs.8,000. On 31st March,2019 their liabilities were Rs.38,000. On this date, they decided to dissolve the firm. The assets realized Rs.1,25,000 and realization expenses amounted Rs. 2,400. SOLUTION: REALISATION ACCOUNT PARTICULARS AMOUNT(Rs.) PARTICULARS AMOUNT(Rs.) To sundry Assets To cash Creditors 38,000 Expenses 2,400 3,12,000 40,400 By creditors By Cash a/c (Assets Realised) By Loss Transferred: Kuhu Cap 94,700 Jigyasa Cap 37,880 Sheeba Cap 56,820 38,000 1,25,000 1,89,400 3,52,400 3,52,400

- 2. PARTNER’S CAPITAL ACCOUNT PARTICULARS KUHU JIGYASA SHEEBA PARTICULARS KUHU JIGYASA SHEEBA To Drawings To Realisation (Loss) To Cash 10,000 94,700 44,900 6,000 37,880 14,760 8,000 56,820 24,940 By Balance b/d By Interest on Capital By P/L Appropriation By General Reserve 1,00,000 6,000 18,600 25,000 40,000 1,200 7,440 10,000 60,000 3,600 11,160 15,000 1,49,600 58,640 89,760 1,49,600 58,640 89,760 CASH ACCOUNT PARTICULARS AMOUNT(Rs.) PARTICULARS AMOUNT(Rs.) To Realisation A/c 1,25,000 By Realisation A/c By Kuhu’s Cap By Jigyasa’s Cap By Sheeba’s Cap 40,400 44,900 14,760 24,940 1,25,000 1,25,000

- 3. MEMORANDUM BALANCESHEET LIABILITIES AMOUNT(Rs.) ASSETS AMOUNT(Rs.) Capital: Kuhu(2,00,000 x 5/10) 1,00,000 Jigyasa(2,00,000 x 2/10) 40,000 Sheeba(2,00,000 x 3/10) 60,000 General Reserve Profit Creditors 2,00,000 50,000 48,000 38,000 Sundry assets(Balancing figure) Drawings: Kuhu 10,000 Jigyasa 6,000 Sheeba 8,000 3,12,000 24,000 3,36,000 3,36,000 PROFIT AND LOSS APPROPRIATION ACCCOUNT PARTICULARS AMOUNT(Rs.) PARTICULARS AMOUNT(Rs.) To Interest on Capital Kuhu 6000 Jigyasa 1200 Sheeba 3600 To Profit Transferred to: Kuhu’s Cap 18,600 Jigyasa’s Cap 7,440 Sheeba’s Cap 11,160 10,800 37,200 By profit and loss A/c 48,000 48,000 48,000