06_Joeri Van Speybroek_Dell_MeetupDora&Cybersecurity.pdf

Keynote capitals india morning note july 27-'11

1. K E Y N O T E

INSTITUTIONAL RESEARCH

India Morning Note

Wednesday, July 27, 2011

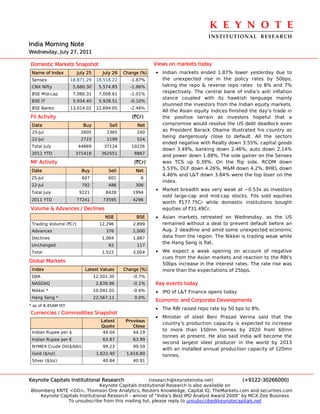

Domestic Markets Snapshot Views on markets today

Name of Index July 25 July 26 Change (%) • Indian markets ended 1.87% lower yesterday due to

Sensex 18,871.29 18,518.22 -1.87% the unexpected rise in the policy rates by 50bps,

CNX Nifty 5,680.30 5,574.85 -1.86% taking the repo & reverse repo rates to 8% and 7%

BSE Mid-cap 7,080.31 7,008.61 -1.01%

respectively. The central bank of India’s anti inflation

stance coupled with its hawkish language mainly

BSE IT 5,934.40 5,928.51 -0.10%

shunned the investors from the Indian equity markets.

BSE Banks 13,014.02 12,694.05 -2.46%

All the Asian equity indices finished the day’s trade in

FII Activity (`Cr) the positive terrain as investors hopeful that a

Date Buy Sell Net compromise would resolve the US debt deadlock even

25-Jul 2605 2365 240

as President Barack Obama illustrated his country as

being dangerously close to default. All the sectors

22-Jul 2723 2199 524

ended negative with Realty down 3.55%, capital goods

Total July 44669 37124 10226

down 3.49%, banking down 2.46%, auto down 2.14%

2011 YTD 371418 362551 8867

and power down 1.88%. The sole gainer on the Sensex

MF Activity (`Cr) was TCS up 0.39%. On the flip side, RCOM down

Date Buy Sell Net

5.53%, DLF down 4.26%, M&M down 4.2%, BHEL down

4.46% and L&T down 3.84% were the top loser on the

25-Jul 607 601 6

index.

22-Jul 792 486 306

• Market breadth was very weak at ~0.53x as investors

Total July 9221 8428 1994

sold large-cap and mid-cap stocks. FIIs sold equities

2011 YTD 77241 73595 4296

worth `177.75Cr while domestic institutions bought

Volume & Advances / Declines equities of `31.49Cr.

NSE BSE • Asian markets retreated on Wednesday, as the US

Trading Volume (`Cr) 12,296 2,899 remained without a deal to prevent default before an

Advances 376 1,000 Aug. 2 deadline and amid some unexpected economic

Declines 1,084 1,887 data from the region. The Nikkei is trading weak while

the Hang Seng is flat.

Unchanged 62 117

Total 1,522 3,004 • We expect a weak opening on account of negative

cues from the Asian markets and reaction to the RBI's

Global Markets

50bps increase in the interest rates. The rate rise was

Index Latest Values Change (%) more than the expectations of 25bps.

DJIA 12,501.30 -0.7%

NASDAQ 2,839.96 -0.1% Key events today

Nikkei * 10,041.01 -0.6% • IPO of L&T Finance opens today

Hang Seng * 22,567.11 0.0%

Economic and Corporate Developments

* as of 8.45AM IST

• The RBI raised repo rate by 50 bps to 8%.

Currencies / Commodities Snapshot

• Minister of steel Beni Prasad Verma said that the

Latest Previous

country’s production capacity is expected to increase

Quote Close

to more than 150mn tonnes by 2020 from 60mn

Indian Rupee per $ 44.04 44.19

tonnes at present. He also said India will become the

Indian Rupee per € 63.87 63.99

second largest steel producer in the world by 2013

NYMEX Crude Oil($/bbl) 99.23 99.59

with an installed annual production capacity of 120mn

Gold ($/oz) 1,622.40 1,616.80 tonnes.

Silver ($/oz) 40.84 40.91

Keynote Capitals Institutional Research (research@keynoteindia.net) (+9122-30266000)

Keynote Capitals Institutional Research is also available on

Bloomberg KNTE <GO>, Thomson One Analytics, Reuters Knowledge, Capital IQ, TheMarkets.com and securities.com

Keynote Capitals Institutional Research - winner of “India’s Best IPO Analyst Award 2009” by MCX-Zee Business

To unsubscribe from this mailing list, please reply to unsubscribe@keynotecapitals.net

2. K E Y N O T E

INSTITUTIONAL RESEARCH

TOP GAINERS Buzzing Stock

(BSE A-Group) • NTPC is set to start work at its proposed 1,320 MW

Previous Current Change thermal project in Bangladesh in the next six

Company Name months.

Close (`) Price (`) (%)

Glen Pharma 328.95 337.60 2.63 • Glenmark Pharmaceuticals has received `65Cr from

Aurobindo Phar 181.15 185.60 2.46 Salix Pharmaceuticals Inc, USA, as an advance

Mana Gen 57.80 58.60 1.38 payment to upgrade its plant for production of

Coal India 369.15 374.00 1.31 Crofelemer, used for treating diarrhoea.

Apollo Hosp 508.15 514.20 1.19 • Allahabad Bank will provide loans to farmers and

(BSE Mid-Cap) rural artisans to buy solar off-grids made by Environ

Previous Current Change Energy Corporation India Pvt Ltd. by entering into an

Company Name agreement with the company.

Close(`) Price(`) (%)

India Sec 40.20 47.40 17.91 • Orient Paper Industries board meet today for

Ballarpur Inds 33.90 36.35 7.23 restructuring

UTV Software 901.80 950.45 5.39

• SKS Microfinance board approves QIP of Rs900Cr by

Ruchi Soya 98.05 102.05 4.08

issue of equity shares to QIB's

Wockhardt 417.60 434.05 3.94

• State-run iron ore miner NMDC's production had

TOP LOSERS risen by about 7% to 6.1mn tonne during the April-

June quarter riding on the back of improved logistics

(BSE A-Group)

and better weather conditions. The country's largest

Previous Current Change carmaker Maruti Suzuki India (MSI) would invest

Company Name

Close(`) Price(`) (%)

about `3,000Cr in 2012-13 financial year on various

Lanco Infra 20.20 18.95 -6.19

areas, including expanding capacity and new model

IDFC 143.30 134.85 -5.90 launches.

Reliance Comm 107.50 101.55 -5.53

GVK Power 19.50 18.55 -4.87 US markets

Indiabul Real Est 115.80 110.25 -4.79

US markets closed near session lows Tuesday as no

(BSE Mid-Cap) clear stand came over hiking the debt ceiling. In its

Previous Current Change third straight losing session, the Dow industrials fell

Company Name

Close(`) Price(`) (%) 91.50 points, or 0.7%, to 12,501.30, with 24 of its 30

Kwality Dairy 161.35 150.55 -6.69 components declining. Losses were led by 3M Co.,

KGN Inds 56.85 54.05 -4.93 which fell 5.4%. The industrial giant said its quarterly

GVK Power 19.50 18.55 -4.87 results were dented by the disaster in Japan and

Indiabu Real Est 115.80 110.25 -4.79 declining demand for LCD televisions. The S&P 500

SREI Infra 49.20 46.95 -4.57 Index fell 5.49 points, or 0.4%, to 1,331.94, with

industrials the hardest hit and technology up the

most among its 10 industry groups.

KEYNOTE CAPITALS LTD.

4th Floor, Balmer Lawrie Building, 5, J. N. Heredia Marg, Ballard Estate, Mumbai 400 001. INDIA

Tel. : 9122-2269 4322 / 24 / 25 • www.keynoteindia.net

Disclaimer: This report is purely for information purpose and is based on public information. News content is attributable to

various media, unless specified otherwise. All market related statistical data pertains to the immediately preceding trading day,

unless stated otherwise. Neither the information nor any opinion expressed in this report constitutes an offer, or an invitation to

make an offer, to buy or sell the securities mentioned herein. We or any of our directors, officers or employees shall not in any

way be responsible for any loss arising from the use of this report. Investors are advised to apply their own judgment before

acting on the contents of this report. The report has not been edited due to time constraints.