Keynote capitals india morning note aug 2-'11

•

0 likes•17 views

- The Indian stock market indices rose slightly on August 1, recovering from recent losses as global markets stabilized after the US averted a debt default. However, Asian markets declined on concerns about slowing US manufacturing. - Car sales in India fell 15% in July from a year ago, while NHPC plans to invest $2.1 billion in two Myanmar power projects and MphasiS acquired a US insurance technology firm. - US markets finished slightly lower after lawmakers approved raising the borrowing limit, ending uncertainty but leaving investors cautious ahead of the final vote.

Recommended

Recommended

More Related Content

What's hot

What's hot (19)

Similar to Keynote capitals india morning note aug 2-'11

Similar to Keynote capitals india morning note aug 2-'11 (20)

More from Keynote Capitals Ltd.

More from Keynote Capitals Ltd. (20)

Recently uploaded

Recently uploaded (20)

Keynote capitals india morning note aug 2-'11

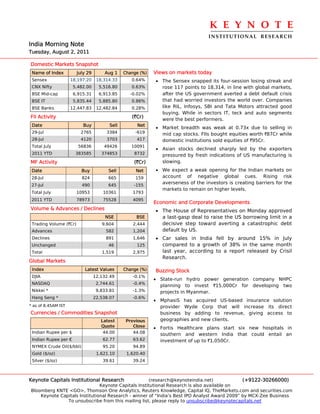

- 1. K E Y N O T E INSTITUTIONAL RESEARCH India Morning Note Tuesday, August 2, 2011 Domestic Markets Snapshot Name of Index July 29 Aug 1 Change (%) Views on markets today Sensex 18,197.20 18,314.33 0.64% • The Sensex snapped its four-session losing streak and CNX Nifty 5,482.00 5,516.80 0.63% rose 117 points to 18,314, in line with global markets, BSE Mid-cap 6,915.31 6,913.85 -0.02% after the US government averted a debt default crisis BSE IT 5,835.44 5,885.80 0.86% that had worried investors the world over. Companies BSE Banks 12,447.83 12,482.84 0.28% like RIL, Infosys, SBI and Tata Motors attracted good buying. While in sectors IT, teck and auto segments FII Activity (`Cr) were the best performers. Date Buy Sell Net • Market breadth was weak at 0.73x due to selling in 29-Jul 2765 3384 -619 mid cap stocks. FIIs bought equities worth `87Cr while 28-Jul 4120 3703 417 domestic institutions sold equities of `95Cr. Total July 56836 49426 10091 • Asian stocks declined sharply led by the exporters 2011 YTD 383585 374853 8732 pressured by fresh indications of US manufacturing is MF Activity (`Cr) slowing. Date Buy Sell Net • We expect a weak opening for the Indian markets on 28-Jul 824 665 159 account of negative global cues. Rising risk 27-Jul 490 645 -155 averseness of the investors is creating barriers for the markets to remain on higher levels. Total July 10953 10361 1793 2011 YTD 78973 75528 4095 Economic and Corporate Developments Volume & Advances / Declines • The House of Representatives on Monday approved NSE BSE a last-gasp deal to raise the US borrowing limit in a Trading Volume (`Cr) 9,604 2,444 decisive step toward averting a catastrophic debt Advances 582 1,204 default by US. Declines 891 1,646 • Car sales in India fell by around 15% in July Unchanged 46 125 compared to a growth of 38% in the same month Total 1,519 2,975 last year, according to a report released by Crisil Research. Global Markets Index Latest Values Change (%) Buzzing Stock DJIA 12,132.49 -0.1% • State-run hydro power generation company NHPC NASDAQ 2,744.61 -0.4% planning to invest `15,000Cr for developing two Nikkei * 9,833.81 -1.3% projects in Myanmar. Hang Seng * 22,538.07 -0.6% • MphasiS has acquired US-based insurance solution * as of 8.45AM IST provider Wyde Corp that will increase its direct Currencies / Commodities Snapshot business by adding to revenue, giving access to Latest Previous geographies and new clients. Quote Close • Fortis Healthcare plans start six new hospitals in Indian Rupee per $ 44.00 44.08 southern and western India that could entail an Indian Rupee per € 62.77 63.62 investment of up to `1,050Cr. NYMEX Crude Oil($/bbl) 95.20 94.89 Gold ($/oz) 1,621.10 1,620.40 Silver ($/oz) 39.61 39.24 Keynote Capitals Institutional Research (research@keynoteindia.net) (+9122-30266000) Keynote Capitals Institutional Research is also available on Bloomberg KNTE <GO>, Thomson One Analytics, Reuters Knowledge, Capital IQ, TheMarkets.com and securities.com Keynote Capitals Institutional Research - winner of “India’s Best IPO Analyst Award 2009” by MCX-Zee Business To unsubscribe from this mailing list, please reply to unsubscribe@keynotecapitals.net

- 2. K E Y N O T E INSTITUTIONAL RESEARCH TOP GAINERS (BSE A-Group) Buzzing Stock Previous Current Change • Jyoti Structures has bagged orders worth `438Cr Company Name Close (`) Price (`) (%) from Vidyut Vitran Company Adani Enter 586.10 637.80 8.82 MANAP FIN 55.05 58.90 6.99 • Surana Industries board approves issue of 80lakh Mah & Mah Fin 637.75 673.20 5.56 shares at `500/share JUBL FOOD 852.50 891.75 4.60 • Shriram EPC wins an order to setup a 75mn litre Ranbaxy Lab 539.00 561.50 4.17 diesel tank storage facility in Queensland Australia (BSE Mid-Cap) • Sun Pharma set to pick up an 11% stake in an Israeli Previous Current Change investment company specializing in life sciences Company Name Close(`) Price(`) (%) • The National Highways Authority of India awarded a Godfrey Phil 3004.95 3307.30 10.06 `2815Cr contract in Madhya Pradesh to TVS Motor 49.35 53.45 8.31 infrastructure player GVK that will fetch it an annual MANAP FIN 55.05 58.90 6.99 premium of about `190Cr for 30 years, more than COX KINGS 208.40 222.90 6.96 the total project cost. Gujarat Mnrl 159.55 169.40 6.17 • Vedanta Resources has received conditional approval from the Indian government for its TOP LOSERS acquisition of a stake in Cairn India. (BSE A-Group) Previous Current Change US markets Company Name Close(`) Price(`) (%) JSW Steel 774.20 694.80 -10.26 US markets finished Monday’s roller-coaster session National Alum 75.50 71.30 -5.56 with a slight loss, with investors on uncertain footing Bharat Forge 329.10 311.00 -5.50 before lawmakers vote on raising the federal borrowing Crompton Greav 169.20 160.35 -5.23 limit. After triple-digit swings in either direction, the Jindal Saw 152.65 145.00 -5.01 Dow Jones Industrial Average ended down 10.75 points, or 0.1%, at 12,132.49, its seventh straight losing (BSE Mid-Cap) session -- the longest since the one ending July 2, 2010. Previous Current Change Company Name Close(`) Price(`) (%) Himadri Chem 56.65 52.80 -6.80 Usha Martin 44.70 41.75 -6.60 Bajaj Elect 219.10 206.85 -5.59 Bharat Forge 329.10 311.00 -5.50 India Infoline 83.55 79.00 -5.45 KEYNOTE CAPITALS LTD. 4th Floor, Balmer Lawrie Building, 5, J. N. Heredia Marg, Ballard Estate, Mumbai 400 001. INDIA Tel. : 9122-2269 4322 / 24 / 25 • www.keynoteindia.net Disclaimer: This report is purely for information purpose and is based on public information. News content is attributable to various media, unless specified otherwise. All market related statistical data pertains to the immediately preceding trading day, unless stated otherwise. Neither the information nor any opinion expressed in this report constitutes an offer, or an invitation to make an offer, to buy or sell the securities mentioned herein. We or any of our directors, officers or employees shall not in any way be responsible for any loss arising from the use of this report. Investors are advised to apply their own judgment before acting on the contents of this report. The report has not been edited due to time constraints.