Virar Best Sex Call Girls Number-📞📞9833754194-Poorbi Nalasopara Housewife Cal...

Keynote capitals india morning note 12 november-12

1.

India Morning Note

a

Mond

day, Novemb 12, 2012

ber 2

Dom

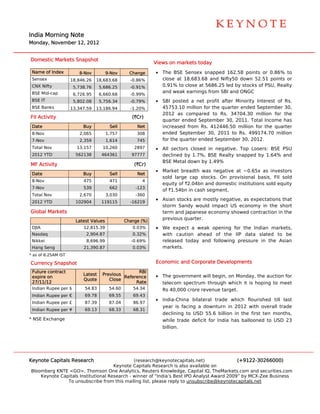

mestic Markets Snapshot

t

V

Views on ma

arkets today

y

Nam of Index

me 8-Nov 9-Nov Change • The BSE Sensex sna

E apped 162.5 points or 0.86% to

58 r

Sens

sex 18,846.26 18,683.68

1 -0.86% close at 18,683.68 aand Nifty50 down 52.51 points or

1

CNX Nifty 5,738.76 5,686.25 -0.91% 0.91% to close at 56

o 686.25 led by stocks of P

y PSU, Realty

BSE Mid-cap and weak earnings frrom SBI and ONGC

6,726.95 6,660.68 -0.99%

BSE IT 5,802.08 5,756.34 -0.79% • SBI postted a net prrofit after Minority Inter

M rest of Rs.

BSE Banks 13,347.59 13,186.94

1 -1.20% 45753.10 million for the quarter ended Sept

0 r tember 30,

2012 as compared to Rs. 347

s 704.30 millio for the

on

FII Ac

ctivity (`Cr)

quarter eended Septeember 30, 2011. Total In ncome has

Date

e Buy Sell Net increased from Rs. 412446.50 million for the quarter

m

8-Nov 2,065 1,757 308 ended September 30, 2011 to Rs. 499174.70 million

7-Nov 2,359 1,614 745 for the quarter ended September 30, 2012.

d

Total Nov

l 13,157 10,260 2897 • All secto

ors closed in negative. Top Losers: BSE PSU

n

2012 YTD

2 562138 464361 97777 declined by 1.7%, BBSE Realty snapped by 11.64% and

BSE Meta down by 1

al 1.49%

MF A

Activity (`Cr)

• Market breadth was negative a ~0.65x as investors

b s at s

Date

e Buy Sell Net

sold larg cap stocks. On prov

ge visional basi FII sold

is,

8-Nov 475 471 4

equity of `2.04bn an domestic institutions s

f nd sold equity

7-Nov 539 662 -123

of `1.54b in cash se

bn egment.

Total Nov

l 2,670 3,030 -360

• Asian sto

ocks are mos

stly negative as expectations that

e,

2012 YTD

2 102904 119115 -16219

storm Saandy would impact US economy in the short

n

Global Markets term and Japanese e

d economy sho

owed contrac

ction in the

previous quarter.

Latest Valu

ues Change (%)

C

DJIA 12,815.39 0.03% • We expe a weak opening for the Indian markets,

ect n

Nasd

daq 2,904

4.87 0.32% with cauution ahead of the IIP data slat

d ted to be

Nikke

ei 8,696

6.99 -0.69% released today and following p

pressure in the Asian

Hang Seng

g 21,390

0.87 0.03% markets..

* as of 8.25AM IST

f

Curre

ency Snapsh

hot Economic and Corporate Developm

a ments

Future contract RBI

Latest Previous • The gove

ernment will begin, on M

Monday, the auction for

expir on

re Reference

R

Quote Close

27/11/12 Rate telecom spectrum th

hrough which it is hopin to meet

ng

India Rupee per $

an 54.83 54.60 54.34 Rs 40,00 crore reve

00 enue target.

India Rupee per €

an 69.78 69.55 69.43

• India-Chiina bilateral trade which flourishe till last

ed

India Rupee per £

an 87.39 87.04 86.97

year is ffacing a dowwnturn in 20

012 with overall trade

India Rupee per ¥

an 69.13 68.33 68.31

declining to USD 55 billion in the first te months,

g 5.6 en

* NSE Exchange while traade deficit fo India has ballooned to USD 23

or s

billion.

Keyno Capitals Research

ote (research h@keynotecapitals.net) (+9122-3026 66000)

Keyno Capitals R

ote Research is also available on

Bloom

mberg KNTE <GO>, Thom mson One Ana alytics, Reute Knowledge, Capital IQ, TheMarkets.com and sec

ers curities.com

Keynote Capi

K itals Institutio

onal Research - winner of “India’s Best IPO Analyst Award 2009” by MCX-Zee Business

h t ” e

To unsubscrib from this m

T be please reply to unsubscribe@keynoteca

mailing list, p apitals.net

2.

TOP GAINERS

G Buzzing St

tocks

(BSE A-Group)

Previous Current Change • Dena Ba

ank expects to achieve a total busin

ness of Rs

Company Name

Close(`) Price(`) (%)

Mahindra & Mah 901.75 962.15 6.70% 1.5 lakh crore by the end of this fiscal on th back of

s he

Asho Leyland

ok 24.1 25.7 6.64% sound growth in dep

posits and ad

dvances.

L&T Finance Hol 62.35 64.2 2.97%

Idea Cellular 90.7 93.35 2.92% • Tata Mo

otors will undertake thre -day bloc closure

ee ck

Adity Birla Nuv

ya 922.8 947.8 2.71% at its Jamshedpur p

plant from N

November 12 to 14 in

2

(BSE Mid-Cap)

E the wake of poor demand.

Previous Current Change

Company Name • Coal Ind Ltd is like to take a final call o its exit

dia ely on

Close(`) Price(`) (%)

Mahindra & Mah 901.75 962.15 6.70% from Int

ternational C

Coal Venture (ICVL) in the next

es

Asho Leyland

ok 24.1 25.7 6.64%

board m

meeting.

Radic Khaitan

co 121.1 127.15 5.00%

Shipp

ping Corp 51.65 53.75 4.07% • Pantaloo and Future Ventures India will

on Retail a

Resp

ponsive Inds 93 96 3.23%

demerge their fashion business

e ses into a n

new listed

TOP LOSERS

L unit that will simplif the busine

fy esses into th

hree main

(BSE A-Group)

segments.

Previous Current Change

Company Name • Reliance Communic

e cations expe

ects the full revenue

l

Close(`) Price(`) (%)

Apoll Hosp

lo 858.05 804.8 -6.21% impact o its recent tariff hike t reflect by the next

of t to y

Aurobindo Phar 178.45 170.2 -4.62%

Andh Bank

hra 108.9 104.6 -3.95%

financial year.

SBI 2243.55 2156.35 -3.89%

• Apollo T

Tyres said it has signed an agreem

t d ment with

Godr Inds

rej 319.6 307.6 -3.75%

(BSE Mid-Cap)

E striking workers for resumption of normal p

production

Previous Current Change at its Va

adodara plan bringing to an end 1 days of

nt, 17

Company Name

Close(`) Price(`) (%)

labour unrest at the unit.

u

Mana

appuram Fin 38.15 32.85 -13.89%

Apoll Hosp

lo 858.05 804.8 -6.21%

Maha

arashtra Sea 343.1 325 -5.28%

Shree Global Trd 47.6 45.25 -4.94%

Aurobindo Phar 178.45 170.2 -4.62%

Keyno Capitals Research

ote (research

h@keynotecapitals.net) (+9122-3026

66000)

3.

India and Global Economic C

Calendar

Countries /

C Monday Tuesd

day Wednesday

W

Regions 12/Nov 13/No

ov 14/Nov

Indian Manufacturing

India Indian M Money Su

M3 upply

Ouutput (MoM)

Indian Ind

dustrial Production

(YoY)

US

Japan Ind

dustrial Produ

uction

Global UK CPI (

(YoY) UK Une

employment Rate

(MoM)

G

German ZEW Economic

W Euro Ind

dustrial Production

Sentim

ment (MoM)

KEYNOTE CAPITALS LTD.

E

The Ruby, 9th Floor, Senapati Ba

, S apat Marg, Dadar (W), M

D Mumbai – 40 028

00

Tel. : +912

22-30266000

0 • www.ke

eynotecapita

als.com

Disclaim

mer: This repo is purely for informatio purpose an is based on public infor

ort f on nd o rmation. News content is a attributable to

o

various media, unles specified ot

s ss therwise. All m

market related statistical da pertains to the immedia

d ata o ately preceding trading dayy,

unless stated otherw

wise. Neither the information nor any opin

nion expresse in this repo constitutes an offer, or a invitation to

ed ort an o

make an offer, to bu or sell the s

a uy securities menntioned herein We or any o our directors, officers or employees sh

n. of hall not in any

y

way be responsible for any loss a

e arising from th use of this report. Inves

he s stors are advi

ised to apply their own jud

dgment before e

acting o the conten of this repo The report has not been edited due t time constraints.

on nts ort. t n to