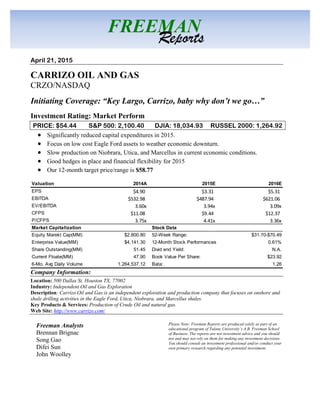

1. April 21, 2015

CARRIZO OIL AND GAS

CRZO/NASDAQ

Initiating Coverage: “Key Largo, Carrizo, baby why don’t we go…”

Investment Rating: Market Perform

PRICE: $54.44 S&P 500: 2,100.40 DJIA: 18,034.93 RUSSEL 2000: 1,264.92

Significantly reduced capital expenditures in 2015.

Focus on low cost Eagle Ford assets to weather economic downturn.

Slow production on Niobrara, Utica, and Marcellus in current economic conditions.

Good hedges in place and financial flexibility for 2015

Our 12-month target price/range is $58.77

Company Information:

Location: 500 Dallas St, Houston TX, 77002

Industry: Independent Oil and Gas Exploration

Description: Carrizo Oil and Gas is an independent exploration and production company that focuses on onshore and

shale drilling activities in the Eagle Ford, Utica, Niobrara, and Marcellus shales.

Key Products & Services: Production of Crude Oil and natural gas.

Web Site: http://www.carrizo.com/

Freeman Analysts

Brennan Brignac

Song Gao

Difei Sun

John Woolley

FREEMAN

Reports

Please Note: Freeman Reports are produced solely as part of an

educational program of Tulane University’s A.B. Freeman School

of Business. The reports are not investment advice and you should

not and may not rely on them for making any investment decisions.

You should consult an investment professional and/or conduct your

own primary research regarding any potential investment.

Valuation 2014A 2015E 2016E

EPS $4.90 $3.31 $5.31

EBITDA $532.98 $487.94 $621.06

EV/EBITDA 3.60x 3.94x 3.09x

CFPS $11.08 $9.44 $12.37

P/CFPS 3.75x 4.41x 3.36x

Market Capitalization Stock Data

Equity Marekt Cap(MM) $2,800.80 52-Week Range: $31.70-$70.49

Enterprise Value(MM) $4,141.30 12-Month Stock Performances 0.61%

Share Outstanding(MM) 51.45 Divid end Yield: N.A.

Current Floate(MM) 47.90 Book Value Per Share: $23.92

6-Mo. Avg Daily Volume 1,264,537.12 Bata: 1.26

2. Carrizo Oil and Gas (CRZO) April 21, 2015

2

FREEMAN

Reports

STOCK PRICE

PERFORMANCE

Figure 1:

5-year Stock Price

Performance

Source:Yahoo Finance (As of 4/20/2015)

INVESTMENT

SUMMARY

Our Freeman Reports analyst team gives Carrizo Oil and Gas a Market

Perform rating, and projects a 12-month target stock price of $58.77, a

7.95 percent increase from its April 20, 2014 stock price of $54.44. To

reach our target price our team used a weighted average of our PV-10

intrinsic valuation (60 percent), multiple valuation using EV/EBITDA (20

percent), and multiple valuation using P/CF (20 percent). Our projections

are based on Carrizo’s historical performance, industry outlook, and

management guidance.

Carrizo’s ability to generate returns for shareholders stems from its ability

to find, drill, and extract oil for positive net present value (NPV) projects.

Cost control is imperative in the current low oil price environment. In the

coming years, Carrizo plans to focus on its large Eagle Ford Shale

position because it offers well established distribution networks, easily

drillable land, and reasonably consistent production numbers based on

estimated reserves, and high quality oil, all of which will keep costs

down. If oil prices remain low, Carrizo plans to divert capital and assets

allocated to other plays to produce more of their existing reserves in the

Eagle Ford play because of its cost effectiveness. For 2015, Carrizo has

good hedges in place, high concentrations of properties in low cost oil

plays, no near term debt obligations due, no upcoming leasehold

obligations, and significant liquidity available from its revolver. Carrizo is

in a solid financial and operational position to weather the economic

downturn in oil.

Carrizo’s biggest challenge is low oil prices in 2015. The Niobrara, Utica,

and Marcellus plays are uneconomical to produce as a result of low oil

prices. The Marcellus play is primarily natural gas, which currently has

even weaker pricing than oil. The Niobrara play offers large upside

potential for Carrizo, however, the distribution network in the Niobrara

play is not developed and the company has no cost effective way to

3. Carrizo Oil and Gas (CRZO) April 21, 2015

3

FREEMAN

Reports

transport its product. In addition, oil prices have significantly impacted

operating profit to the firm and as a result Carrizo has had to drastically

cut capital expenditure, limiting its ability to explore for and drill new

reserves in less developed plays. Carrizo plans to develop its existing

reserves in the Eagle Ford play using a three drill rig program in 2015

because the play is the most cost effective. Management plans to focus on

the Eagle Ford Shale and keep oil production flat at Q4 2014 levels until

oil prices rise, equating to a 17 percent increase in oil production year

over year.

Figure 2: Carrizo Asset Portfolio

Source: Carrizo Scotia Howard Weil 2015 Energy Conference Presentation

INVESTMENT

THESIS

As an E&P company, Carrizo’s value is driven by its ability to explore for

new reserves, drill new wells, and increase production year over year by

replacing the natural decline in well production with new producing wells.

Because, Carrizo is currently a price taker in an economic downturn, the

company’s profitability is dependent on its ability to maintain current

production levels at lower well costs. In order to stay profitable, the

company will grow production while using a significantly smaller amount

of capital expenditure in 2015 than in the previous year. Management

plans to drill horizontal wells and produce more from its existing

developed plays in order to cut costs while increasing production. Carrizo

will cut expenditure on new plays in 2015 in order to whether the oil

pricing downturn.

4. Carrizo Oil and Gas (CRZO) April 21, 2015

4

FREEMAN

Reports

Figure 3: Carrizo CAPEX Budget

Source: Carrizo Scotia Howard Weil 2015 Energy Conference Presentation

Significantly

Reduced Capital

Expenditures in

2015

As a result of the depressed oil price environment, Carrizo’s operating

profits have decreased leaving the company with less capital to explore

for, drill, and produce new reserves. Carrizo has significant liquidity in its

revolver with only $210 million drawn from the $800 million revolver in

place. However, taking on additional debt in a precarious pricing

environment is risky. Carrzio, like many other E&P companies, was

forced to cut capital expenditures by nearly 50 percent in 2015.

Management provided capital expenditure guidance of $496 million for

2015, down 42 percent from $857 million in the previous year. $377

million (76.17 percent) of Carrizo’s capital expenditure plan has been

allocated to the Eagle Ford Shale because of its cost efficiency.

The majority of capital expenditures allocated to plays other than the

Eagle Ford Shale, is dedicated to exploratory and experimental programs.

Carrizo’s allocation of capital to alternative plays shows that it is looking

ahead to when oil prices recover.

Focus on Low Cost

Eagle Ford Assets

to Weather

Economic

Downturn

Carrizo will primarily focus its production efforts on its Eagle Ford assets

in 2015. Carrizo has previously developed mature operations in the Eagle

Ford Shale. To cut costs, the company plans to drill near existing

infrastructure. In an effort to increase production, Carrizo is testing 330

foot downspacing between wells in the area. The company has already

reduced the per well cost 21 percent in Q1 2015 compared to FY2014.

Carrizo management expects oil prices to recover in the near future and is

using this play to keep production stable while waiting for a recovery.

Carrizo has 260.5MMBoe of probable reserves in the Eagle Ford valued

at $3.11 billion using an SEC PV10 valuation at the end of FYE2014.

Carrizo has one rig online in Eagle Ford and plans to bring on two

additional rigs in early 2015. Carrizo’s current Eagle Ford reserves have a

SEC PV10 of over $6 billion with a three rig drilling plan according to

Management. Management is counting on additional Eagle Ford reserves

5. Carrizo Oil and Gas (CRZO) April 21, 2015

5

FREEMAN

Reports

to drive target growth of 17 percent production year over year. In

addition, Carrizo assumes that its probable reserves in the Eagle Ford will

be producible. According to management, more than 50 percent of

Carrizo’s undrilled locations are economic (IRR>10 percent) if oil is

below $50/Bbl. Specifically, over 80 percent of Eagle Ford Shale

locations have a break even cost below $44/Bbl. If price depression lasts

through 2016, Carrizo plans to divert assets from other plays to drill in the

Eagle Ford shale to continue production growth. Our intrinsic valuation is

based on $55/Bbl oil. At that price level, Carrizo’s Eagle Ford assets

generate a rate of return of 29 percent.

Figure 4: Operating Cash Flow By Region

Source: Carrizo Scotia Howard Weil 2015 Energy Conference Presentation

Slow Production in

Niobrara, Utica,

and Marcellus in

Current Conditions

Carrizo plans to aggressively cut capital expenditures, exploration,

drilling, and production efforts in its Niobrara and Utica plays. The

company is prepared to cut production and turn off wells in the event that

the price of oil drops further. Conversely, if oil prices recover, Carrizo is

positioned to continue production in its other plays. Carrizo regards

operational flexibility as an important competitive advantage in this low

oil pricing environment.

In 2015, Carrizo plans to drill one well and frac two wells in the Utica

play, which is a historically low drill count. Most of Carrizo’s capital

expenditure allocated to Utica is allocated to securing leaseholds that will

be used two or three years in the future when commodity prices are

expected to recover.

6. Carrizo Oil and Gas (CRZO) April 21, 2015

6

FREEMAN

Reports

Good Hedges in

Place and Financial

Flexibility for 2015

Carrizo has $590 million in liquidity available on its revolver and an

elected commitment of $685 million at FYE2014. Carrizo has a

debt/EBITA ratio of approximately 2.3x which is relatively low in the

highly leverage E&P industry. Management guidance states that the

company plans to keep debt/EBITDA under a 3.0x target ratio during

2015.

On 4/14/2015 Carrizo announced that it replaced $600 million in senior

bonds with $650 million in new bonds. Carrizo lowered the interest rate

on its bonds from 8.625 percent to 6.250 percent, saving the company

over $11 million a year in interest expense. The increase in bond offering

reflects the company’s financial strength and its ability to take advantage

of the low interest rate environment.

In Q1 2015, Carrizo entered into hedging positions to lock in $166.4

million of cash flows, using costless collars for March 2015, through

December 2015. The hedges will provide Carrizo with downside

protection on prices below the floor of $50/Bbl and allow Carrizo to

benefit from an increase in prices up to a ceiling of $66.46/Bbl.

Specifically, Carrizo has approximately 55 percent of its oil production

hedged at a weighted average floor price of $56.91/Bbl and 40 percent of

its natural gas production hedged at a weighted average price of

$4.29/MMBtu.

VALUATION The 12 month target price for Carrizo Oil and Gas is $58.77, a 7.95

percent increase from the $54.44 closing price as of 4/20/2015. As a

result of the increase in Carrizo’s expected stock performance, Carrizo Oil

and Gas has a Market Perform Rating. Carrizo’s target price was

reached using three valuation methods: PV-10 valuation, multiple

valuation using EV/EBITDA, and multiple valuation using P/CF.

PV-10 Valuation A PV-10 valuation is a commonly used discounted reserve valuation for

E&P companies. A PV-10 measures the revenue a company would earn

on its reserves if it were to stop acquiring new acreage today and produce

the rest of its current reserves through their useful life. The cash flows

from this process are then discounted at a 10 percent discount rate to find

the NPV and NAV of an oil company’s reserves. Major drivers in

Carrizo’s PV-10 valuation are estimated production, capex, commodity

prices, recovery rates, natural decline rates, and lease operating expense.

This methodology accurately reflects the current fundamental value of an

E&P company as it currently stands. Our base case intrinsic valuation

assumes 50 percent of Carrizo’s probable reserves will be produced in

addition to our PV-10 discounted proved reserves. Our high case, includes

100 percent of PV-10 proved reserves, 50 percent of probable reserves,

and 50 percent of possible reserves. In addition, Carrizo is assumed to

produce considerably less than estimated probable reserves in less

7. Carrizo Oil and Gas (CRZO) April 21, 2015

7

FREEMAN

Reports

profitable plays, such as the Utica and Marcellus shales. The final

intrinsic value price was reached using an average of the base case and

high case to yield a stock price of $56.89.

Table 1: Intrinsic Valuation

Multiple Valuation Oil and gas companies commonly use multiple valuations because net

income is unpredictable and financial statements do not reflect an E&P

company’s actual future expected cash flows. Our multiple valuation

examines Carrizo’s enterprise value, EBITDA, discretionary cash flow,

and share price in comparison to its peers’.

8. Carrizo Oil and Gas (CRZO) April 21, 2015

8

FREEMAN

Reports

Peer Group

EV/EBITDA

Enterprise value (EV) over earnings before interest expense, taxes,

depletion, and amortization (EBITDA) uses a peer group average multiple

to determine a company’s enterprise value based on the expected future

EBITDA of the company being valued. Carrizo’s peer group consists of

five E&P companies similar to Carrizo in operational focus and market

capitalization. E&P companies use EV/EBITDA ratio valuation for two

important reasons. First, the ratio excludes the effect of leverage, which is

typically very high in E&P companies and varies depending on the

company. Second, EBITDA measures profits before interest, non-cash

expenses, and depletion and amortization, which can have a large impact

on an E&P firms’ earnings but does not impact EBITDA. Applying the

peer group EV/EBITDA multiple of 8.72x to Carrizo’s FY2015E

EBITDA yielded a stock price of $63.73.

Peer Group P/CF Oil and gas analysts commonly use the price to cash flow multiple

because cash flow is hard to for management to manipulate as opposed to

net income. The cash flow in this case is operating cash flow, which

excludes exploration expenses and adds back non-cash expenses,

depreciation, amortization, deferred taxes, and depletion which have a

material impact on a company’s earnings. When commodity prices are

low, multiples expand, and when commodity prices are high, multiples

contract. Applying Carrizo’s peer group P/CFPS multiple of 6.3x to

Carrizo’s FY2015E CFPS we arrived at a stock price for Carrizo of

$59.46.

Table 2: Multiple Valuation and Price Comparison

9. Carrizo Oil and Gas (CRZO) April 21, 2015

9

FREEMAN

Reports

Figure 5: Valuation

COMPANY

DESCRIPTION &

PROPERTY

OVERVIEW

As a Houston-based Independent Energy Exploration and Production

(E&P) company founded in 1993, Carrizo Oil and Gas Incorporated

(CRZO/NASDAQ) operates through its wholly-owned subsidiaries, such

as Carrizo (Marcellus) LLC. Within the upstream segment of the oil and

gas industry, Carrizo conducts nearly all of its business within the U.S.

Carrizo focuses its oil and gas exploration, production, and development

efforts on its proved reserves in the Eagle Ford, Niobrara, Marcellus, and

Utica shale plays. Within these plays, Carrizo reports 151 million barrels

of oil in proven reserves on an equivalent basis with an additional 480

million in probable reserves. In these four areas, the company has 259

developed wells producing 33 thousand barrels oil a day on an equivalent

basis. Currently, 67 percent of Carrizo’s production and reserves are oil

based.

History Carrizo initially went public in 1998 on the NASDAQ. Carrizo has

focused on horizontal drilling and the completion of unconventional

resource plays over the last ten years. In 2010, Carrizo announced the

initiation of oil focused horizontal development programs in the Eagle

Ford Shale in South Texas and Niobrara Formation in Northeastern

Colorado. As of 2011, the company accumulated proved oil and gas

reserves of 935.6 billion cubic feet equivalent comprised of 728 billion

cubic feet of natural gas, and operated 349 gross producing oil and gas

wells, making it a market leader. As of December 31, 2014 Carrizo

recorded 900 billion cubic feet equivalent in reserves with 259 net

producing wells. For the fiscal year 2014, Carrizo had record production

of 37,696 Boe/d. Carrizo performed well due to the company's previously

developed Eagle Ford shale assets and continues to improve production in

10. Carrizo Oil and Gas (CRZO) April 21, 2015

10

FREEMAN

Reports

the new Texas acreage acquired from Eagle Ford Minerals LLC (EFM)

last year.

Latest

Developments

In October of 2014, Carrizo announced the successful acquisition of

additional producing properties in the Eagle Ford Shale for $250 million

in cash. The transaction included 6,280 net acres located in LaSalle,

McMullen, and Atasoca Counties in Texas, increasing Carrizo’s position

in the Eagle Ford Shale to 82,000 net acres. Estimates of property assets

include 16.7 MMBoe net proved reserves consisting of 82 percent oil. The

company financed the transaction with a private debt offering of $300

million. The company does not traditionally purchase producing

properties, however, management felt that the acquisition was beneficial

because of its low price, high production estimates, positive impact on

cash flows, and potential increases in earnings per share. Management

expects a 17 percent increase in oil production from 2014 to 2015.

Despite rapidly dropping oil prices at the beginning of 2015, analysts

continue to rate Carrizo’s stock highly because of its Eagle Ford Shale

acquisition. Of the 21 analysts that cover the company, 14 give Carrizo’s

stock a buy rating, 6 give the stock a hold rating, and only 1 gives the

stock a sell rating. Positive sentiment for Carrizo’s stems from its Eagle

Ford Shale operations, which resulted in record Q4 oil production

increase of 70 percent year over year, with 26 percent increase in

revenues year over year despite falling oil and gas prices.

Properties Currently, Carrizo principally operates in four areas, including the Eagle

Ford Shale in South Texas, the Niobrara Formation in Colorado, the

Marcellus Shale in Pennsylvania, and the Utica Shale in Ohio, and the

company has offices in each state. Management intends to focus their

operations on the plays which yield the highest oil to gas ratios, primarily

the Eagle Ford

Eagle Ford Shale

As part of Carrizo’s strategy for shifting its operations towards crude oil,

management launched a land acquisition program in early 2010 targeting

the Eagle Ford Shale play in Texas. Carrizo restricted its land acquisitions

to the volatile oil window in the central area of the Eagle Ford Shale. As

of February 25, 2014, the company has accumulated approximately

65,500 additional net acres in the Eagle Ford Shale, producing 12.6

MBoe/d. Carrizo currently reports 122.5 MMBoe of proved reserves on

82,000 acres in this location. Currently, Carrizo has 176 wells producing

approximately 21 thousand barrels of oil a day on an equivalent basis in

this area with 220 waiting to be developed. The company’s wells in the

Eagle Ford area come online with a daily production rate of 625 barrels of

oil per day, shown in the Figure 6 below.

In the future, Carrizo’s management intends to focus the majority of

capital expenditures on this area because of the high production rate in

11. Carrizo Oil and Gas (CRZO) April 21, 2015

11

FREEMAN

Reports

comparison to the other three shale plays. Horizontal drilling remains the

focus of the drilling efforts in the Eagle Ford area.

Figure 6: Eagle Ford Type Curve

Source: Carrizo Scotia Howard Weil 2015 Energy Conference Presentation

Niobrara Formation

Carrizo’s land position in the Niobrara Formation is located in Weld and

Morgan Counties. Currently, Carrizo has 54 wells producing

approximately 2.6 thousand barrels of oil a day on an equivalent basis in

this area with 11 waiting to be developed. Additionally, the Company is

currently developing and testing for more drilling potential in this area. As

of December 31, 2014, the company accumulated approximately 35,900

net acres in the Niobrara Formation. Carrizo currently has 5.6 MMBoe of

proved reserves in this area. Going forward, the Niobrara formation

remains Carrizo’s secondary focus behind the Eagle Ford due to a lower

percentage of gas production coming from the Niobrara compared to the

Utica and Marcellus areas.

Marcellus Shale

The Marcellus Shale, one of the most active and economical natural gas

plays in the America, extends from New York to Eastern Ohio and West

Virginia. Most of Carrizo’s land position in this area rests in West

Virginia and northeastern and central Pennsylvania. In 2007, Carrizo

launched a leasing program in the play, and currently owns an interest in

approximately 33,400 net acres. Drilling in the Marcellus shale is

predominately horizontal. Carrizo has net production of approximately 8.4

MBoe/d with 22.2 MMBoe of proved reserves in this acreage. Production

in this area comes from 27 producing wells. Because of depressed natural

gas markets and a high concentration of natural gas in the Marcellus

formation, Carrizo intends to reduce capital expenditures in this area

moving forward.

12. Carrizo Oil and Gas (CRZO) April 21, 2015

12

FREEMAN

Reports

Utica Shale

Carrizo’s leasing and drilling activities in the Utica Shale are primarily in

Guernsey and northern Noble Counties, Ohio. The Company currently

owns more than 120 net potential drilling locations on 28 thousand acres

in the Utica Shale. Carrizo currently estimates 0.7 MMBoe in proved

reserves in the Utica. The company currents operates only two developed

wells producing less than one thousand barrels of oil a day on an

equivalent basis without any wells waiting to be developed. Carrizo plans

to scale back all capital expenditures in this formation to more effectively

focus assets in the Eagle Ford Shale play.

INDUSTRY

ANALYSIS

Carrizo operates within the global oil and gas industry. Specifically,

Carrizo is a U.S. upstream company which operates strictly on land. The

segments of the oil and gas industry include:

Service Companies

Upstream Companies

Midstream Companies

Downstream Companies

Fully Integrated Companies

Service companies supply upstream companies with anything they may

need to extract oil and gas from the earth, including everything from drill

bits to supply boats. Upstream companies specialize in locating crude oil

and natural gas (including liquids), leasing/buying land, and extracting the

commodities from beneath the earth’s surface and ocean floor. Investors

refer to these companies as exploration and production companies (E&P).

Midstream companies transport the oil or gas from the well to the plant or

storage facility. Downstream companies buy the raw oil or gas, process it

into usable end products, and sell it to the public. Integrated companies

operate within all of the above sectors. The “super majors” are the five

largest publically traded, fully integrated oil and gas companies.

13. Carrizo Oil and Gas (CRZO) April 21, 2015

13

FREEMAN

Reports

Figure 7: Production and Profit

Source: Thomson Reuters (As of 2015)

The United States is the world’s third-largest petroleum producer, with

more than 500,000 producing wells and approximately 4,000 oil and

natural gas platforms operating in U.S. waters. Together, oil and gas

supply 65 percent of U.S. energy. The nation’s 144 refineries process

more than 17 million barrels of crude oil every day. Oil and gas

production facilities include 16,000 establishments with a value of

shipment of $134 billion. The oil and gas industry employs 9.8 million

people. According to their annual reports, the five super majors reported a

combined $1.53 trillion in revenue in 2014. As seen in Figure 7, the

revenue of any oil and gas company within any segment is highly

correlated with the prices of crude oil and natural gas.

Crude Oil and

Natural Gas Pricing

Commodity prices have dropped more than 50 percent since June 2014,

and the U.S. oil and gas industry has been through an extended economic

downturn. The most recent WTI price is around $55(ICE) and Brent price

is around $63(ICE).The natural gas price is $2.59(NYMEX). The above

oil and gas prices are low compared to recent historical levels.

Supply and demand determine crude oil and natural gas prices. Global

energy consumption is the basis of worldwide oil demand and

macroeconomic factors influence the total usage of oil. As the gross

domestic production of a country increases, so too will its energy

consumption. When U.S. GDP growth is slow and supply is high, prices

decline dramatically. Heating is the main driver of natural gas demand in

the U.S., making the demand, and therefore prices, seasonal. The

macroeconomic side of the natural gas demand is influenced by energy

usage abroad and some domestic consumption. The amount of oil

produced, called the supply side, is influenced by two key factors. First,

14. Carrizo Oil and Gas (CRZO) April 21, 2015

14

FREEMAN

Reports

oil and gas are difficult to find and extract, making technological

advances a key factor in the success of E&P companies. Second, once

reserves are located, the producer can choose how much to extract and

sell. At this point geopolitics come into play. Several Middle Eastern

countries own oil and gas companies, and because they control nearly 40

percent of the world’s supply, artificially regulating supply is in their best

interest. Oil producing nations created Organization of the Petroleum

Exporting Countries (OPEC) to decide how much oil and gas they should

produce.

In 2014, the balance between supply and demand tipped in the opposite

direction. Prices for crude oil shifted dramatically from June 2014 to the

beginning of 2015 because of several macroeconomic factors. The U.S.

shale revolution, through the usage of hydraulic fracturing and horizontal

drilling, enabled the United States to produce as much crude oil as Saudi

Arabia, the number one producer in the world, causing a large increase in

supply. Around the same time, the market experienced large declines in

GDP from Asian and European countries, causing a global decline in

demand which affected energy prices in the US. Extended declines in

GDP caused the European Union and other countries to enact quantitative

easing measures, causing exchange rates to fall to pre-housing crisis

levels. Crude oil is priced in U.S. dollars around the globe. The strength

of the dollar causes foreign consumers to import less crude oil, further

weakening demand. Given decreased demand, OPEC acted

uncharacteristically by refusing to decrease production in order to reach

equilibrium, in an effort to strengthen their market share.

Equilibrium theories predict that the amount of oil demanded by

customers is exactly the same as the amount being produced by oil and

gas companies. With no significant decrease in production on the horizon,

demand must increase in order for crude oil prices to rebound. In a recent

microeconomic trend report, Goldman Sachs asserted that China is set to

take over as the number one fossil fuel consumer in the world in the near

future, but its demand for oil is relatively low. In addition, the report

stated that oil consumption in emerging markets is slow. This could create

a new equilibrium price for oil that is much lower than prices over the last

decade. A recent study from the U.S. Energy Information Administration

(EIA) projects that oil consumption worldwide will remain relatively flat

over the next three years.

The Nature of the

Production Process

E&P companies usually have four operational phases: exploration,

acquisition, development, and production. In the exploration phase, E&P

companies search for potential oil and gas through geological fieldwork,

geological modeling, seismic imaging, and exploratory drilling.

Successful exploration plays a key role in maintaining reserves and future

revenue for E&P companies. If E&P companies detect oil and gas, they

will start the acquisition phase, which usually involves leasing land to

drill wells on target properties. Drilling wells is risky because it requires

15. Carrizo Oil and Gas (CRZO) April 21, 2015

15

FREEMAN

Reports

large amounts of capital, labor, technology, and environmental regulation

compliance. To share risk, many companies tend to enter into joint

ventures with well-funded partners at this phase. Oil and gas drilling is a

speculative activity that involves numerous risks and could have a

significant impact on the operational and financial position of a company.

An E&P company drills oil and gas wells and connects them to pipelines

for distribution. After this phase, oil and gas can be extracted and

transported to downstream companies. Finally, oil refineries refine crude

oil into various marketable end products including gasoline, diesel fuel

and jet fuel. Companies will continue to produce at a particular well as

long as its output is economically viable. Figure 8 shows the process of oil

and gas production.

Figure 8: Oil and Gas Production Map

Source: Energy Information Administration

In the past, U.S. E&P companies have utilized technological innovations

in drilling techniques such as hydro-fracking in the development of oil

shale, horizontal drilling in the development of the natural gas shale plays,

and environment friendly methods like pipeline maintenance and repair.

As previously discussed, oil and gas companies must consistently produce

new wells to grow production. E&P companies also innovate renewable

energy resources such as converting water into snow, and solar power, to

streamline operations.

Customers and

Suppliers

Oil exploration and production is a complex process that involves

specialized technology and equipment. Owning production equipment is

costly and requires extensive maintenance, so most oil companies utilize

oilfield services companies that supply the infrastructure, equipment, and

technology to explore for, extract, and transport crude oil and natural gas

16. Carrizo Oil and Gas (CRZO) April 21, 2015

16

FREEMAN

Reports

from the earth to the refinery, and eventually to the consumer.

Oilfield services companies provide five key roles in the market.

1. Oilfield equipment suppliers build rigs and supply hardware for

rig maintenance and upgrades.

2. Oilfield disposal services suppliers provide saltwater disposal and

transportation services for oil and gas companies.

3. Oil exploration and production services contractors deal in seismic

imaging technology or provide drilling services.

4. Oil and gas pipeline companies build onshore pipelines to

transport oil and gas between cities, states, and countries.

5. Oil and gas maritime transportation companies supply the tankers

and services to transport large quantities of oil and gas across the

ocean.

The oilfield service market is a highly competitive environment. E&P

companies have bargaining power in this market because they can switch

to other suppliers if current suppliers do not make competitive offers.

Table 3 presents customers that account for more than 10 percent of

Carrizo’s oil and gas sales for each year respectively.

Table 3: Carrizo’s Major Customers

(a) Revenues from the customer were below 10% during the year.

Source: Carrizo 2014 Annual Report

As other purchasers are available in all areas of Carrizo’s operations,

Carrizo’s sales will not significantly deteriorate from the loss of any one

current customer.

Carrizo’s Position

in the Industry

Carrizo owns a small share of the market. In 2014, Carrizo realized oil

and gas revenues of $720.2 million and production is 12.0 MMBoe. Table

4 illustrates a comparison between Carrizo’s production and the total

production of U.S. energy industry.

17. Carrizo Oil and Gas (CRZO) April 21, 2015

17

FREEMAN

Reports

Table 4: Carrizo Production against Entire U.S. Energy Industry

Source: Energy Information Administration (As of 2015)

Carrizo’s discretionary cash flow for 2014 was $512 million.

Discretionary cash flow is an important metric for E&P companies

because they often carry large amounts of debt, capital expenditures, and

depreciation on their books making net income a less accurate measure of

cash flow. Discretionary cash flow is an important measure of whether or

not a company will be able to service its debt and expand cash flow in the

future.

Carrizo’s replacement ratio for 2014 was 513 percent. The reserve

replacement ratio shows whether an E&P company is replacing reserves

or depleting them. The ratio is important for oil and gas companies

because reserves are constantly in natural decline and E&P companies

must consistently add reserves to its books to grow effectively.

Porter’s Five

Forces

Porter’s five forces is a framework for evaluating the strategy,

development, and weaknesses of a given industry. Each force is rated as

either low, medium, or high from the perspective of the company being

analyzed.

Threat of entry: Medium

E&P firms such as Carrizo must overcome large capital requirements

because the costs associated with startup are high. According to Wood

Mackenzie, U.S. upstream operations spent $140 billion in 2014. Carrizo,

a relatively small company, had a capital expenditure budget upwards of

$690 million in 2014. New companies face large financing and liquidity

stress in developing the infrastructure required for finding and developing

new wells.

In addition, locating and developing oil and gas reserves requires

interrelated technical expertise and human capital. E&P firms need

specialists in geography, legal teams, petroleum engineering experts, and

operations specialists to perform competitively. Exploration requires

extensive capital because it includes the process of finding usable

reserves, licensing land, drilling wells and obtaining distribution channels.

Labor cost is usually considered a fixed cost in the E&P industry.

Geopolitical factors and high fixed costs also make entering this industry

difficult because exploration is time consuming and expensive, and

regulatory requirements are strict.

18. Carrizo Oil and Gas (CRZO) April 21, 2015

18

FREEMAN

Reports

Bargaining Power of Suppliers: Low

Carrizo’s suppliers mostly consist of oil and gas field services suppliers

such as Halliburton. These companies assist Carrizo in logistical activities

such as surveying properties, drilling wells, and cementing wells.

Carrizo’s suppliers charge the company a day rate to rent equipment such

as drilling rigs and hydraulic fracturing equipment. Concentration in the

oil and gas field services industry is relatively low meaning that there are

several competitors, but there are few large companies that own expensive

assets that Carrizo must rent in order to produce oil and gas.

Bargaining Power of Buyers: Low

In the oil and gas industry, buyers have no bargaining power because the

price of oil is determined by supply and demand in the worldwide market.

Future and spot prices driven by the global exchange of oil as a

commodity play a significant role in determining the price of oil. Oil

prices are quoted as a differential between the premium quality products

and the products oil companies are actually producing. WTI and Brent,

which are traded on the NYMEX, are the benchmarks for oil prices.

Figure 9 shows the WTI and Brent index over the last 15 years and

demonstrates the price determined by the spot market. The differential

between the benchmark and the price that a company receives is a

function of oil quality and distance from major processing hubs.

In addition, oil and gas companies hedge against oil price fluctuations

with futures contracts that guarantee a specific price for the oil they

produce. Through the use of hedging, companies have more predictable

plan for the future and ensure that buyers have less bargaining power over

the price of oil.

Figure 9: World Oil Index Movement due to Arbitrage

Source: Thomson Reuters (As of 2015)

19. Carrizo Oil and Gas (CRZO) April 21, 2015

19

FREEMAN

Reports

Availability of Substitutes: Low

Fossil fuels are the most widely used sources of energy. External

competition stems from hydro, solar, wind, and nuclear power; however,

competition is minimal because alternative power sources cannot generate

energy on a large scale. According to the Institute for Energy Research,

oil accounted for 95.1 percent of transportation energy consumption and

67 percent of electricity generation in 2014.

Competitive Rivalry: High

Competition in the exploration and production industry is high and the

trend of competition is steady. The exploration and production industry is

fragmented and the four largest companies account for only 25 percent of

industry revenue. Oil and gas companies compete on a price basis;

however, because oil prices are previously determined by macroeconomic

factors, they compete on a basis of cost. Companies compete by lowering

extraction costs thereby bolstering margins. Oil companies also compete

on a quality basis because higher quality oil and gas is valuable.

PEER ANALYSIS Carrizo’s peer group consists of six upstream, onshore focused firms

which are independent and similar in terms of the areas in which they

operate and their market capitalization. Carrizo’s peers are Chesapeake

Energy, Range Resources, Rosetta Resources, SM Energy, and

Southwestern Energy. The companies operate inside the U.S., primarily

within the Eagle Ford, Barnett, Utica, Marcellus, and Bakken shale plays.

As shown in Table 5, all six companies are within the midcap range in

terms of market capitalization.

Table 5: Peer Data

Source: Bloomberg and 2014 Company Annual Reports

Chesapeake Energy

Co. (CHK/NYSE)

Chesapeake is an independent oil and gas exploration and production

company and the 11th largest producer of oil and NGL’s in the U.S. The

company holds a large portfolio of unconventional onshore assets in

major shale plays across the U.S. including properties in the Barnett,

Eagle Ford, Utica, Haynesville, and Marcellus Shales. In Q3 of 2014 the

company produced 726 MBoe/d, of which 70 percent was natural gas. In

2014 Chesapeake spent $5 billion in capital expenditures to increase

production on existing properties and increase leaseholds in the

Marcellus Shale as well as Utica Shale. Chesapeake is forecasting 10

percent overall production growth for 2015.

20. Carrizo Oil and Gas (CRZO) April 21, 2015

20

FREEMAN

Reports

Range Resources

Corp. (RRC/NYSE)

Range’s headquarters are in Fort Worth, Texas. Range has producing

upstream wells in the Marcellus, Mid-Continent, and Southern

Appalachian regions. Range’s capital expenditure for the 12 months

ending on September 30, 2014 was $1.13 billion. Revenue for the same

period was $1.2 billion. In 2014, Range produced 425 Bcfe in total, and

early in 2015 the company announced that its proved reserves have

increased 26 percent to 10.3 Tcfe.

Rosetta Resources

Inc.

(ROSE/Nasdaq)

Rosetta operates strictly out of the Eagle Ford Shale and the Permian

Basin formation. The company expected to spend $1.2 billion in capital

expenditures in 2014. Total production for for 2014 was 63 - 66 Mboe

per day and in 2015 the company expects to produce 76 – 82 Mboe per

day.

SM Energy Co.

(SM/NYSE)

SM Energy is an independent exploration and production company that

focuses on oil and gas resource plays in North America. SM Energy’s

primary producing properties are 144,000 net acres in the Eagle Ford

Shale and 238,000 net acres in the Bakken Shale. In addition the firm

leases property in the Rocky Mountain, Mid-Continental, and Permian

regions. In Q3 of 2014, the company produced 143 MBoe/d of which 54

percent was gas and only nine percent was oil. In 2014, SM Energy put a

$1.9 billion capital budgeting plan into effect to increase its position in

the Eagle Ford and Bakken Shales. The company expects to grow

revenues by approximately 15 percent in 2015. In 2013, SM Energy had

estimated reserves of 428.7 MMBoe.

Southwestern

Energy Co.

(SWN/NYSE)

Southwestern has offices in Spring, Texas and Conway, Arizona. Current

upstream operations are located in the Marcellus, Fayetteville, Arkoma,

East Texas, Brown Dense, DJ Basin, and New Brunswick plays.

Southwestern’s capital expenditure for the 12 months ending on

September 30, 2014 was $2.24 billion. Revenue for the same period was

$3.98 billion. Southwestern also has a mid-stream segment which

supports its exploration and production strategy. In 2014 Southwestern

produced 758 – 764 Bcfe. After a recent acquisition from Statoil and

WPX energy, Southwestern increased its proved reserves to 9.5 Tcfe and

expects to produce 2.5 Bcfe/d in 2015.

MANAGEMENT

PERFORMANCE

&

BACKGROUND

Carrizo’s management team, including veterans and experienced

newcomers, plays a key role in the company’s operations and focuses on

stable growth rate, excellent assets, and operational flexibility. The top

executives’ collective experience and expertise in the E&P industries

form a strong foundation for Carrizo’s strategic success.

As shown in Table 6, Carrizo’s management team has improved ROIC

by more than its peer average since 2010, excluding Rosetta because of

its much smaller market cap. Carrizo has reported a positive ROIC every

21. Carrizo Oil and Gas (CRZO) April 21, 2015

21

FREEMAN

Reports

year since 2010. The company’s success is a result of its active pursuit of

new opportunities such as the new acreage acquired in the Eagle Ford

Shale in 2014.

Table 6: ROIC

Source: Bloomberg (As of 4/20/2015)

S.P. “Chip”

Johnson

President and Chief Executive Officer(58)

S.P. “Chip” Johnson, a co-founder of Carrizo, has served as President,

Chief Executive Officer, and a director since December 1993. Prior to

joining Carrizo, Mr. Johnson worked as Operations Superintendent,

Manager of Planning and Finance, and Manager of Development

Engineering at Shell Oil Company for 15 years. From 2003 to January

2011, he served as a director of Pinnacle Gas Resources, Inc. Currently

he is also a director of Basic Energy Services, Inc., an oilfield service

provider. Mr. Johnson is a Registered Petroleum Engineer and holds a

B.S. in Mechanical Engineering from the University of Colorado.

Brad Fisher Vice President and Chief Operating Officer(53)

Brad Fisher has served as Vice President and Chief Operating Officer

since March 2005. Starting in July 2000, he served as Vice President of

Operations, and he served as General Manager of Operations from April

1998 to June 2000. Prior to joining Carrizo, Mr. Fisher spent 14 years

with Cody Energy Services. He held various managerial and technical

positions at Ultramar Oil & Gas Limited, last serving as Senior Vice

President of Engineering and Operations. Mr. Fisher holds a B.S. in

Petroleum Engineering from Texas A&M University. At Carrizo’s 2015

Analyst Conference, Mr. Fisher showed that the operations team had a

good track record of meeting production goals and Capex guidance. The

company will enter the learning curve at a much higher point in the

coming year.

David Pitts Vice President, Chief Financial Officer, Chief Accounting Officer

and Treasurer(47)

David Pitts has served as Vice President, Chief Financial Officer, Chief

Accounting Officer, and Treasurer since August 2014. Mr. Pitts had

previously worked as Carrizo’s Vice President and Chief Accounting

Officer since January 2010. Prior to joining Carrizo, Mr. Pitts was an

audit partner with Ernst & Young and a Senior Manager at Arthur

Andersen. Mr. Pitts is a CPA and holds a B.S. in Accounting and

22. Carrizo Oil and Gas (CRZO) April 21, 2015

22

FREEMAN

Reports

Business from Southwest Baptist University.

Dick Smith Vice President of Land(56)

Dick Smith has served as Vice President of Land for Carrizo Oil & Gas

since August 2006. Prior to joining Carrizo, Mr. Smith held the position

of Vice President of Land for Petrohawk Energy Corporation from its

inception in January of 2004 through August 2006 and was responsible

for managing the entire corporate land function. Mr. Smith was with

Unocal Corporation where he held the position of Land Manager for the

U.S. Gulf Region with areas of concentration in the OCS, Onshore

Texas, Louisiana, and Louisiana State Waters from April, 2001 through

the end of 2003. Mr. Smith is a Certified Professional Landman with a

BBA in Petroleum Land Management from the University of Texas at

Austin.

Gregg Evans Vice President of Exploration(64)

Gregg Evans has served as Vice President of Exploration since March

2005. Prior to joining Carrizo, he worked as Vice President North

America Onshore Exploration for Ocean Energy from 2001 to 2003.

From 1996 to 2000, he worked at Burlington Resources where he served

as Chief Geophysicist North America, Gulf of Mexico Deep Water

Exploration Manager, and Geoscience Manager for the Western Gulf of

Mexico Shelf. Prior to that, Mr. Evans served as Division Exploration

Manager of the Rocky Mountain Region and the Gulf Coast area and also

held various other technical and managerial positions with Burlington

Resources. Mr. Evans holds a B.S. in Geophysical Engineering from the

Colorado School of Mines and received the Cecil H. Green award for

outstanding geophysical student.

Andy Agosto Vice President of Business Development

Andy Agosto has been involved with the oil and gas industry for 30

years. In 2003, Mr. Agosto joined Carrizo Oil & Gas as Vice President of

Business Development to develop and manage its efforts in the Barnett

Shale and Eagle Ford Shale plays. Prior to joining Carrizo, Mr. Agosto

was Chief Operating Officer for CCNG, Inc. focusing on the midstream

and service side of the energy business. Mr. Agosto earned his B.S. in

Chemical Engineering from Texas A&M University. At Carrizo’s recent

2015 Analyst Conference, Mr. Agosto talked about valuation

benchmarking for the company and showed investors how the company

compares to its competitors operating in the Eagle Ford Shale.

RISK ANALYSIS

& INVESTMENT

CAVEATS

Carrizo oil and gas is subject to a number of risks including operational,

regulatory, and financial risks that are systematic in the exploration and

production industry. These risks may significantly impact Carrizo’s

ability to generate cash flows, raise capital, and plan new drilling

projects.

23. Carrizo Oil and Gas (CRZO) April 21, 2015

23

FREEMAN

Reports

Operational Risks Operational risks for E&P companies include reserve longevity,

commodity price volatility, technological risks, drilling risks, capital

requirements, and reserve estimates. Drilling and producing oil is a

speculative activity that has inherent uncertainties and therefore risks that

may have an adverse impact on Carrizo’s business.

Reserve Longevity

The primary focus of an E&P Company to ensure long term success is

the ability to replace oil and gas production and sales with additional

proved reserves. If an E&P company continues to produce without

replenishing its reserves, the company will run dry and cease to operate.

Carrizo can increase reserves in two ways. First, Carrizo can buy

property bearing proved reserves, which can be expensive. Second,

Carrizo can also explore for and produce oil and gas itself by leasing the

land and equipment, which yields higher margins if successful.

Operational inputs, such as land and equipment, determine the cost of

production for oil and gas but, no individual company can determine the

price paid for the final product. Carrizo faces the risk of failure in finding

new wells to replace depleted reserves and grow production.

Commodity Price Volatility

In Carrizo’s 2014 10-K, management outlines volatile oil and gas prices

as the primary risk for the company. E&P companies have more price

risk than the midstream and downstream segments because they are

“price takers.” Carrizo must sell its product at prices which the market

determines. Oil and gas prices change with global supply and demand.

These prices can be cyclical. Gas is in higher demand during the colder

months than in warmer months, making it seasonally cyclical. There is a

direct link between oil prices and demand via the gross domestic

production of energy consuming nations, making demand economically

cyclical. Uncertain prices affect the company’s ability to forecast

revenue, profitability, cash flow, and could impact the firm’s ability to

borrow funds and obtain additional financing. Carrizo uses hedging to

lock in the price of future production and guarantee the feasibility of

certain projects. E&P companies benefit most from hedging when prices

decline in a sharp manner. The 50 percent decline in energy prices from

June to December 2014 is a perfect example of a situation in which

hedges become profitable. Management emphasizes that as a result of

recent volatile oil and gas prices, the company is particularly dependent

on the production and sale of oil, but current economic conditions may

force the company to curtail operations. The company also emphasizes

that certain wells that were once profitable to drill no longer meet

Carrizo’s internal rate of return requirements and are no longer

economically viable.

24. Carrizo Oil and Gas (CRZO) April 21, 2015

24

FREEMAN

Reports

Technology

The technological feasibility of producing oil and gas is essential in terms

of a company’s success. Although Carrizo does not invest money directly

into research and development, the equipment and methods Carrizo uses

to find and extract hydrocarbons from beneath the Earth’s surface, are

extremely expensive to develop. Service companies spend millions of

dollars inventing and procuring efficient tools and processes to discover

and produce oil and gas, such as drill bits and hydraulic fracturing rigs.

The more technologically advanced these products become, the more

Carrizo must pay in day rates to the service companies to use them.

Carrizo prices the inherent risks of operations into the projects the

company takes on. In addition, many of Carrizo’s competitors are large

fully-integrated oil companies with large amounts of capital resources.

E&P companies are heavily dependent on technological advances and

Carrizo may not have access to technology as advanced as its

competitors, which gives larger companies a competitive advantage.

Drilling Risk

Carrizo’s growth strategy is based on a “growth through the drill bit”

principal, but drilling for oil and gas is a speculative activity that carries

significant risks. One of the major risks in drilling for oil is the

possibility that the company will not establish commercially productive

oil or gas wells. Drilling costs are substantial and even after drilling is

completed and production begins, a well may not be commercially

productive and economically viable. In addition, volatile oil prices may

force Carrizo to delay or cancel drilling projects in several locations,

which will lead to lower cash flows, lower production, and difficulties

expanding the business.

Reserve Estimates

E&P companies estimate oil and gas reserves using volumetric analysis

but these estimates may be inaccurate. Carrizo clearly states that

“reservoir engineering is a subjective and inexact process of estimating

oil and gas that cannot be measured in an exact manner.” As of February

2015, 57 percent of Carrizo’s proved reserves were undeveloped, and

when production begins, proved reserves are subject to upward or

downward adjustment. Finally, all oil wells are subject to natural decline,

a well may suffer from a natural decline rate much steeper than projected

and as a result, management may miss its production target rates.

Capital Requirements

Exploration and production is an extremely capital intensive industry that

requires large amounts of investment for a business to grow. For 2015,

Carrizo anticipates the need for additional outside funding to successfully

continue operations. Because of the recent downturn in oil prices, most

25. Carrizo Oil and Gas (CRZO) April 21, 2015

25

FREEMAN

Reports

exploration and production companies have significantly cut capital

expenditure by an average of 50 percent. The company may not be able

to acquire additional capital under its existing credit facilities in the

current oil environment. With less capital, Carrizo will have to severely

limit its development drilling programs, which means that the company

may not be able to keep pace with natural decline and will struggle to

grow revenue.

Industry Regulation

E&P companies are subject to heavy regulation from local, state, and

federal sources. Carrizo must adhere to laws that cover drilling permits,

well testing, plug and abandonment, and well spacing, which can cost the

company millions of dollars. As environmental regulations have become

more stringent, compliance costs for companies like Carrizo have

become significantly higher in recent years.

Greenhouse Gas Emissions

Increased scrutiny of the E&P industry may occur as a result of the

EPA’s 2011-2016 National Enforcement Initiative, “Assuring Energy

Extraction Activities Comply with Environmental Laws”, increasing

attention in the United States and worldwide to the issue of climate

change and the contributing effect of GHG emissions. Concerns about

emissions may affect operations by limiting drilling opportunities or

imposing materially increased costs on E&P companies including

Carrizo.

Hydraulic Fracturing

The EPA has asserted federal regulatory authority over hydraulic

fracturing under the federal Safe Drinking Water Act, and has released

draft permitting guidance for hydraulic fracturing operations. Several

states, including states where Carrizo operates such as Colorado, Ohio,

and Texas, have proposed or adopted legislative or regulatory restrictions

on hydraulic fracturing through additional permit requirements, public

disclosure of fracturing fluid contents, water sampling requirements, and

operational restrictions. Those ongoing changes could reduce the

volumes of oil and gas that the company can economically recover,

which could materially and adversely affect revenues and results of

operations.

Pipeline Regulations

Although most E&P firms do not own or operate pipelines or facilities

under direct regulation of the FERC, the FERC’s regulations of third-

party pipelines and facilities could indirectly affect Carrizo’s ability to

market production. Beginning in the 1980s, the FERC initiated a series of

major restructuring orders that required pipelines, among other things, to

perform open access transportation. The FERC’s changes substantially

increased competition in the natural gas market. The effect the FERC’s

other activities will have on access to markets, the fostering of

26. Carrizo Oil and Gas (CRZO) April 21, 2015

26

FREEMAN

Reports

competition and the cost of Carrizo’s daily operations, remains to be

seen.

Tax Laws

In addition to environmental legislation, the U.S. Congress is currently

debating significant changes to oil and gas tax laws. Proposed changes

may reduce certain tax deductions that are currently available with

respect to oil and gas exploration and development. Any such change can

negatively affect Carrizo’s financial position and operations.

Financial Risk Carrizo operates in a capital intensive industry and certain financial risks

arise when the company takes on debt to finance operations. Financial

risk is particularly relevant today because the current low price of oil has

forced E&P companies to cut capital spending and limit drilling projects.

Cash Flow Risk

The current ratio and quick ratio are indicators of a company’s short-term

liquidity. As Figure 7 shows, Carrizo’s current ratio is 0.66, which is

marginally lower than its peer average; however, its quick ratio is 0.65,

which is marginally higher than its peers. The company’s current and

quick ratios suggest that Carrizo will be able to service current liabilities

on its balance sheet using resources that are immediately available.

Credit Risk

Drilling for oil requires large sums of money, which E&P companies

usually use debt to finance. The more debt a company uses to support

operations, the more the company has to pay in interest on a percentage

and total basis. Therefore, debt heavy E&P companies are sensitive to

interest rate changes. Higher debt levels increase the probability of a

company going bankrupt if production and/or prices fall. Debt-to-Asset

Ratio and Debt-to-Equity Ratio measure a company’s leverage and credit

risk. As Figure 7 shows, Carrizo’s Debt-to-Asset Ratio and Debt-to-

Equity Ratio are significantly higher than its peers, which means Carrizo

has more credit risk than its peers. In addition, Carrizo has an interest

coverage ratio of 16.4, marginally lower than its peers, which means that

Carrizo is less capable of paying interest expense obligations from its

operating income than its peers. Carrizo’s cash generated-to-cash

required ratio is 0.4, among the lowest of its peers, showing the

company’s cash on hand has been significantly reduced because of the

downturn in oil. In addition, as Figure 8 shows, Carrizo’s Debt-to-Asset

Ratio had low fluctuation in the past five years, which is an indication of

the company’s stable credit management.

Hedging

Carrizo hedges a portion of its forecasted production to manage exposure

to commodity price risk. As of March 24, 2015, Carizo’s hedge positions

for 2015 were comprised of 30,000 MMBtu/d of natural gas and 12,200

Bbls/d of crude oil. From March 2015 through December 2016, Carrizo’s

27. Carrizo Oil and Gas (CRZO) April 21, 2015

27

FREEMAN

Reports

hedging position provides the company with solid downside protection

on 12,200 Bbls/d in 2015 and 4,000 Bbls/d in 2016 of crude oil at prices

below the floor of $50.00 per Bbl yet allow it to benefit from an increase

in crude oil prices up to the ceiling of $66.46 per Bbl in 2015 and $76.50

per Bbl in 2016. Carrizo’s hedging program helps ensure stable cash flow

and reduces financial risks.

Table 7: Financial Risk Ratios

Source: Bloomberg (As of 4/20/2015)

Table 8: Carrizo Historical Leverage

Source: Bloomberg (As of 4/20/2015)

SHAREHOLDER

ANALYSIS &

CORPORATE

GOVERNANCE

As of April 20, 2015, Carrizo Oil and Gas has 90 million shares

authorized, 51.45 million shares outstanding and 42.8 million (92

percent) of which trade as public float. Institutional investors own 69

percent, mutual funds own 28 percent, and insiders own 7 percent of the

company’s equity. Carrizo has not issued dividends in over a year and

has not announced plans to do so in the immediate future. The company

has not repurchased common stock in recent years. Investors are

currently selling 4,110,000 shares short which is about 9.80 percent of

the float. Short selling on Carrizo’s stock has decreased by 20.92 percent

over the last quarter as a result of falling oil prices. According to

Morningstar data on mutual fund investing styles, 49 percent of funds

bought Carrizo as a growth stock while only 7 percent bought Carrizo as

a value stock. Investor perception that Carrizo is a growth stock reflects

high expectations for the company’s recent investment in the Marcellus

and Eagle Ford Shale.

Institutional

Shareholders

Institutional investors own over 97 percent of Carrizo Oil and Gas equity.

Table 9 shows the top ten institutional investors that control 38.74

percent of the company. Individual investors favor an ownership

structure of this type because of the ‘managers overseeing managers’

effect. Large institutional investment companies watch over Carrizo’s

board carefully because they have a stake in Carrizo’s success. Individual

investors look favorably on the additional third party oversight of

Carrizo’s management. The total number of shares owned by these ten

28. Carrizo Oil and Gas (CRZO) April 21, 2015

28

FREEMAN

Reports

highly involved institutions has increased by approximately three percent

since 2014, which indicates confidence in future stock performance.

Table 9: Top Ten Institutional Investors

Source: Bloomberg (As of 4/20/2015)

Insider

Shareholders

As of April 21, 2015, insider holdings represent 7.69 percent of total

shares outstanding, a decrease of 7.8 percent since February 2, 2014.

Over the past six months, Carrizo reported 36 insider transactions,

including 29 selling and 7 buying. On the open market, four insider

shareholders sold a total amount of 83,292 shares, but no insider

shareholder has made any open market purchase since August 2014.

Steven A. Webster, the largest insider shareholder of Carrizo, did not

report any position change over the past six months. Table 10 lists the top

five insider shareholders.

Table 10: Top Five Insider Shareholders

Source: Bloomberg (As of 4/20/2015)

Corporate

Governance

Carrizo’s current leadership structure is Mr. Johnson serving as Chief

Executive Officer, Mr. Webster serving as Chairman of the Board, and

Mr. Parker serving as Lead Independent Director. Mr. Parker is a

Financial Advisor for multiple companies in the Houston, Texas area. He

has owned and operated Parker Investments since 1984 and has been

involved in structuring private and venture capital investments for the

past 15 years. Table 11 shows a brief summary of the board and its sub-

committees.

29. Carrizo Oil and Gas (CRZO) April 21, 2015

29

FREEMAN

Reports

Table 11: The Board and Sub-Committees

Source: Bloomberg (As of 4/20/2015)

Since the company became a publicly traded company in 1997, several

separate individuals have held roles of Chairman of the Board and Chief

Executive Officer. Because today’s company directors have more

oversight responsibilities than ever before, having a separate Chairman

who has the responsibility of leading the Board is beneficial. In addition,

by having an independent director serve as Chairman of the Board, the

company’s Chief Executive Officer is able to focus on leading the

company. The company’s Lead Independent Director’s responsibility is

to preside over meetings at which the Chairman is not present, to serve as

a liaison between the Chairman (and management) and the independent

directors. The Lead Independent Director has the right to call meetings of

independent directors and vote for the company’s decision, which

benefits both the company’s operation effectiveness and shareholder

interest.

The Audit Committee mainly takes responsibility for the appointment,

retention, compensation and oversight of the independent registered

public accounting firm for the purpose of preparing the Company’s

annual audit reports or performing other audit, review or attest services

for Carrizo. The Board has determined that all of the members of the

Audit Committee satisfy the independence standards under the NASDAQ

Listing Rules and Rule 10A-3 of the Securities Exchange Act. In

addition, the Board has determined that Mr. Parker is an ‘audit committee

financial expert’ who is a certified public accountant and served as

partner at a major accounting firm.

30. Carrizo Oil and Gas (CRZO) April 21, 2015

30

FREEMAN

Reports

The primary responsibilities of the Compensation Committee are to

review and approve the compensation of the Chief Executive Officer and

other executive officers and oversee and advise the Board on the policies

that govern Carrizo’s compensation programs. The Nominating and

Corporate Governance Committee works on identifying, evaluating and

recommending, for the approval of the entire Board of Directors,

potential candidates to become members of the Board of Directors. It

also recommends membership on standing committees of the Board of

Directors. Overall, Carrizo has an optimal management with independent

Board members and regulated Board sub-committees structure, which are

well prepared for the company’s operating efficiency.

FINANCIAL

PERFORMANCE

&

PROJECTIONS

Our Team’s Projections for Carrizo’s financial performance are heavily

dependent on the current low oil pricing environment and cost

effectiveness of shale oil plays as oil prices change. Carrizo’s ability to

thrive in the current oil pricing environment, differentiates it from its

peers.

Production Based on company presentations and management conversations we

assumed that Carrizo would have a fairly flat run rate from Q4 2014

production into 2015 with slow growth in the three years following as

commodity prices slowly improve according to our price deck. We

assume the majority of Carrizo’s drilling efforts will be focused on the

Eagle Ford Shale for the next four years and no other material production

will be added during that time. In addition, we Carrizo’s gas production

will decrease year over year and its oil production will increase as the

company moves assets from its gas plays to its oil based sweet spots.

Carrizo gave guidance that it plans to drill 54 new wells in 2015 and exit

2015 with the same number (22) wells waiting to be completed as 2014.

Therefore, guidance for total wells completed in 2015 is 54. In Q1 2015,

only 1 rig will be operating in Eagle Ford therefore production numbers

will be lower than the following three quarters. In the February press

release, CZRO stated average quarterly production for 2015 will be fairly

close to Q4 2014. Also, total year-over-year growth from 2014 to 2015

will be 17 percent due to Q4 2014 being the strongest of the four trailing

quarters.

In the following years we assumed that if commodity price remain

depressed, Capex will be similar to the $495 million laid out in 2015

moving forward. Management will drill a similar amount of wells and

continue to focus on Eagle Ford. Three rigs will be operated and

production will be evenly spread across four quarters and production will

remain stable. Farther into the future, our team assumed that management

will need to move assets from other gas and uneconomical oil plays to

the Eagle Ford play in order to keep up with current production.

31. Carrizo Oil and Gas (CRZO) April 21, 2015

31

FREEMAN

Reports

Oil & Gas Pricing

Assumptions

The pricing forecast used in our intrinsic valuation is based on the

NYMEX oil prices for WTI oil as of April 20, 2015, which was $55/Bbl.

At $55/Bbl oil pricing, Carrizo’s Eagle Ford assets generate a rate of

return of 29 percent. Our gas price projections are based on a Henry Hub

price of $3/Mcf. We used a 30 percent discount to the price of oil and gas

to account for Carrizo’s unsuccessful drilling projects that would occur in

the event the company attempted to produce its remaining proved,

probable, and possible reserves at current commodity prices.

Operational

Expenses

SGA will decrease by five percent every year after 2015 because as oil

prices decline Carrizo will be forced to cut costs. Interest expense will

increase by five percent every year after 2015 because the company will

draw down debt on its RLOC and have to pay interest on that debt. We

assume that Carrizo will pay a consistent percentage of stock based

compensation based on total compensation in next three years because

stock. Total compensation is tied to overall company performance, the

current oil and gas price environment, and Carrizo’s commitment to cost

reductions. We assume Income tax rate is 36 percent and that all taxes

will be deferred during 2015 and in perpetuity.

Lifting Costs will stay in the range of $6.75 and $7.50 in 2015 according

to management guidance. We project lifting costs will remain stable

thereafter. Production taxes are four percent of production which is the

average of last four quarters. Ad valorem taxes will remain fairly in line

with the previous period minus a small differential because ad valorem

taxes are based on the value of the minerals a company is leasing, and

reserve property value will fall with falling oil prices.

Gain/Loss on derivatives is based on a four quarter trailing average

because this number will be a large gain until Carrizo’s existing hedges

expire and new, less profitable hedges take effect. DD&A will be roughly

$25.50 per barrel of oil equivalent in production. Because Carrizo plans

to scale back its capex we assumed this percentage will remain flat.

Financing Our major assumptions were that Carrizo would need to draw down $65

million in debt in each quarter of 2015 which will come directly from

Carrizo’s revolving line of credit (RLOC). This is the amount that

Carrizo will need in cash to be able to continue its operations. After

2015, Carrrizo will decrease its borrowing to $50 million per year in

order reduce total debt. The debt needed above is based on our cash on

hand projections and will come from Carrizo’s revolving credit facility as

well. This cash will be used to fund drilling and production operations. In

addition, we assumed that there will be no change in income tax

percentage and that all taxes will remain deferred for all periods

projected.

Carrizo will remain 60 percent hedged in gas and NGL, and 44 percent

hedged in oil for 2015. Carrizo has approximately 20 percent of 2016 oil

32. Carrizo Oil and Gas (CRZO) April 21, 2015

32

FREEMAN

Reports

production hedged with no other gas or oil hedges in place thereafter. In

addition we assumed that the company differentials from the benchmarks

will remain the same for the next four years.

33. Carrizo Oil and Gas (CRZO) April 21, 2015

33

FREEMAN

Reports

Carrizo Oil & Gas Inc. (CRZO)

Annual and Quarterly Income Statement

34. Carrizo Oil and Gas (CRZO) April 21, 2015

34

FREEMAN

Reports

Carrizo Oil & Gas Inc. (CRZO)

Discretionary Cash Flow

35. Carrizo Oil and Gas (CRZO) April 21, 2015

35

FREEMAN

Reports

Carrizo Oil & Gas Inc. (CRZO)

Annual and Quarterly Balance Sheets

36. Carrizo Oil and Gas (CRZO) April 21, 2015

36

FREEMAN

Reports

Carrizo Oil & Gas Inc. (CRZO)

Annual and Quarterly Statement of Cash Flows

37. Carrizo Oil and Gas (CRZO) April 21, 2015

37

FREEMAN

Reports

Carrizo Oil & Gas Inc. (CRZO)

Ratios