Maithan Alloys: A Multibagger; Buy for a medium term target of Rs300

•

0 likes•461 views

MAL has reported huge improvement in its performance for 9M FY15 wherein sales have gone up by 12% but PAT has ZOOMED by 410%. 9M Eps stands at Rs 28.50 which is more than Eps of entire FY14.

Recommended

Recommended

More Related Content

What's hot

What's hot (18)

Similar to Maithan Alloys: A Multibagger; Buy for a medium term target of Rs300

Similar to Maithan Alloys: A Multibagger; Buy for a medium term target of Rs300 (20)

More from IndiaNotes.com

More from IndiaNotes.com (20)

Recently uploaded

Recently uploaded (20)

Maithan Alloys: A Multibagger; Buy for a medium term target of Rs300

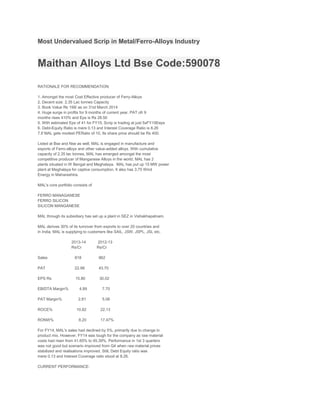

- 1. Most Undervalued Scrip in Metal/Ferro-Alloys Industry Maithan Alloys Ltd Bse Code:590078 RATIONALE FOR RECOMMENDATION: 1. Amongst the most Cost Effective producer of Ferry-Alloys 2. Decent size: 2.35 Lac tonnes Capacity 3. Book Value Rs 199/ as on 31st March 2014 4. Huge surge in profits for 9 months of current year. PAT ofr 9 months rises 410% and Eps is Rs 28.50 5. With estimated Eps of 41 for FY15, Scrip is trading at just 5xFY15Eeps 6. Debt-Equity Ratio is mere 0.13 and Interest Coverage Ratio is 8.26 7.If MAL gets modest PERatio of 10, Its share price should be Rs 400. Listed at Bse and Nse as well, MAL is engaged in manufacture and exports of Ferro-alloys and other value-added alloys. With cumulative capacity of 2.35 lac tonnes, MAL has emerged amongst the most competitive producer of Manganese Alloys in the world. MAL has 2 plants situated in W Bengal and Meghalaya. MAL has put up 15 MW power plant at Meghalaya for captive consumption. It also has 3.75 Wind Energy in Maharashtra. MAL's core portfolio consists of FERRO MANAGANESE FERRO SILICON SILICON MANGANESE MAL through its subsidiary has set up a plant in SEZ in Vishakhapatnam. MAL derives 30% of its turnover from exports to over 20 countries and in India, MAL is supplying to customers like SAIL, JSW, JSPL, JSL etc. 2013-14 2012-13 Rs/Cr Rs/Cr Sales 818 862 PAT 22.98 43.70 EPS Rs 15.80 30.02 EBIDTA Margin% 4.89 7.70 PAT Margin% 2.81 5.06 ROCE% 10.82 22.13 RONW% 8.20 17.47% For FY14, MAL's sales had declined by 5%, primarily due to change in product mix. However, FY14 was tough for the company as raw material costs had risen from 41.65% to 45.39%. Performance in 1st 3 quarters was not good but scenario improved from Q4 when raw material prices stabilized and realisations improved. Still, Debt Equity ratio was mere 0.13 and Interest Coverage ratio stood at 8.26. CURRENT PERFORMANCE:

- 2. N I N E MONTH E N D ED Y/ENDED 31/12/2014 31/12/2013 31/3/2014 Rs/Cr Rs/Cr Rs/Cr Sales 676 604 816 PAT 41.50 10.15 22.98 Equity 14.56 EPSRs 28.50 6.97 15.80 MAL has reported HUGE improvement in its performance for 9M FY15 wherein sales have gone up by 12% but PAT has ZOOMED by 410%. 9M Eps stands at Rs 28.50 which is more than Eps of entire FY14. 2014-15E Rs/Cr Sales 920 PAT 59 Equity 14.56 EPS Rs 41 For 2014-15, MAL can achieve sales of Rs 920 crores with PAT of 59 crores. With estimated Eps of 41 for FY15, Stock is trading at 5xFY15E Eps. Considering that MAL has very low debt and highly profitable producer of ferroy alloys, scrip is strongly undervalued at current PERatio of 5. Scrip is lying low as so far, it has been under-researched and not on the discussion radar of analysts/investing community. Investors may remember that in these columns only, this author had recommended Canfin Homes @ Rs 115 towards end of 2013 which now has gone up by 500% in a span of just 13-14 months. Even if MAL gets moderate PE Ratio of 10, its share price should be Rs 400/. Investors may buy big quantity and hold for medium term for multibagger appreciation Coming Days Target 300 EMAIL US AT—PROFITTRACK@REDIFF.COM Disclaimer: The author has taken due care and caution to compile and analyse the data. The opinions expressed above are only the views of the author, and not a recommendation to buy or sell. Neither the author nor IndiaNotes.com accept any liability whatsoever arising from the use of any of the above contents.