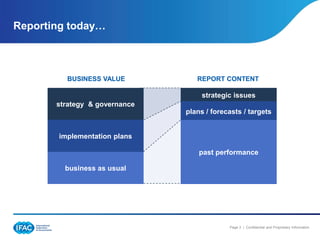

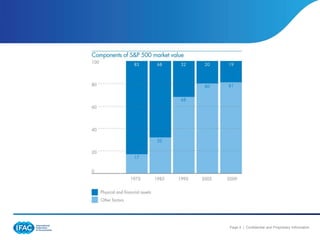

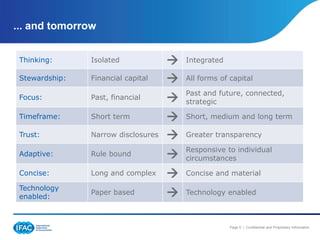

The document discusses integrated reporting for small and medium enterprises (SMEs) in Africa, highlighting South Africa's leadership in this area through initiatives such as King III and the Johannesburg Stock Exchange's requirements. It outlines the significance of integrated reporting in enhancing business strategies, risk management, and stakeholder engagement, emphasizing its relevance for SMEs as vital economic contributors. Additionally, it provides an SME action plan to facilitate the adoption of integrated reporting practices.