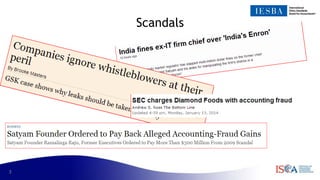

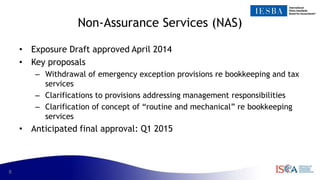

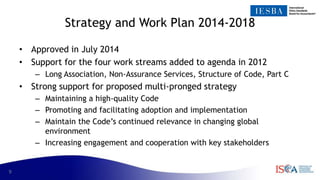

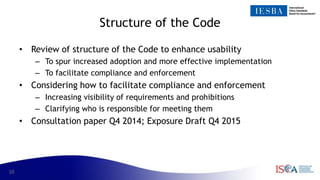

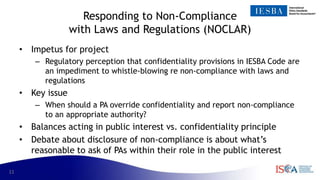

The document summarizes updates and future plans regarding the International Ethics Standards Board for Accountants' (IESBA) Code of Ethics. It discusses expectations for the accounting profession to respond to public scandals by continuing to strengthen ethics standards globally. Key ongoing projects aim to address issues like long partner rotations, non-assurance services, responding to illegal acts, and improving the structure and implementation of the Code. The IESBA is seeking input on proposed changes and working to balance ethics and confidentiality while acting in the public interest.