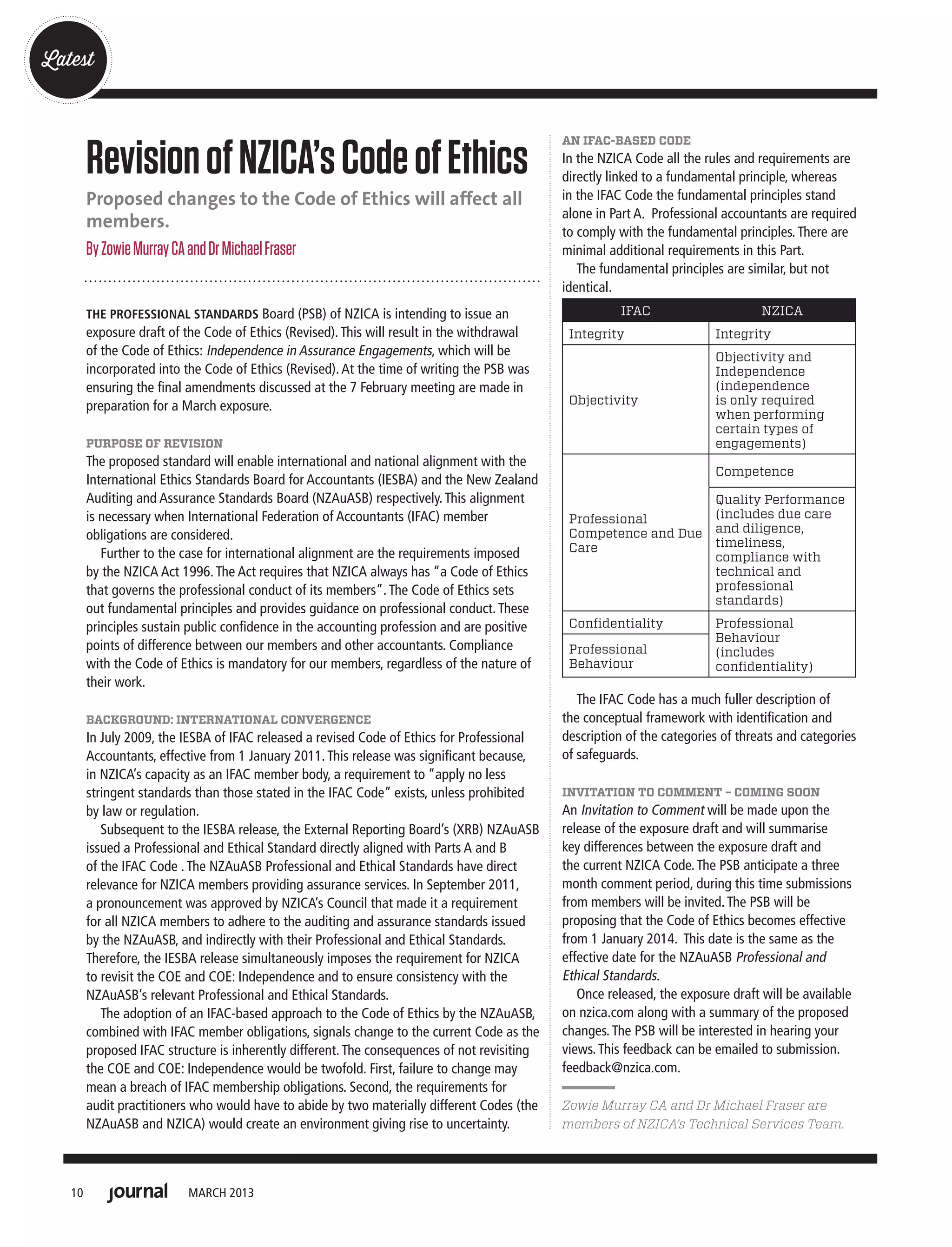

The Professional Standards Board of NZICA intends to issue an exposure draft of the revised Code of Ethics, which will incorporate and withdraw the existing Code of Ethics on Independence in Assurance Engagements. This revision aims to align the Code of Ethics with international standards from IESBA and national standards from NZAuASB. As an IFAC member, NZICA is required to apply ethical standards no less stringent than IESBA, and members must also comply with NZAuASB standards for assurance services. The proposed changes will affect all members and an invitation to comment on the exposure draft will be issued for a three month period.