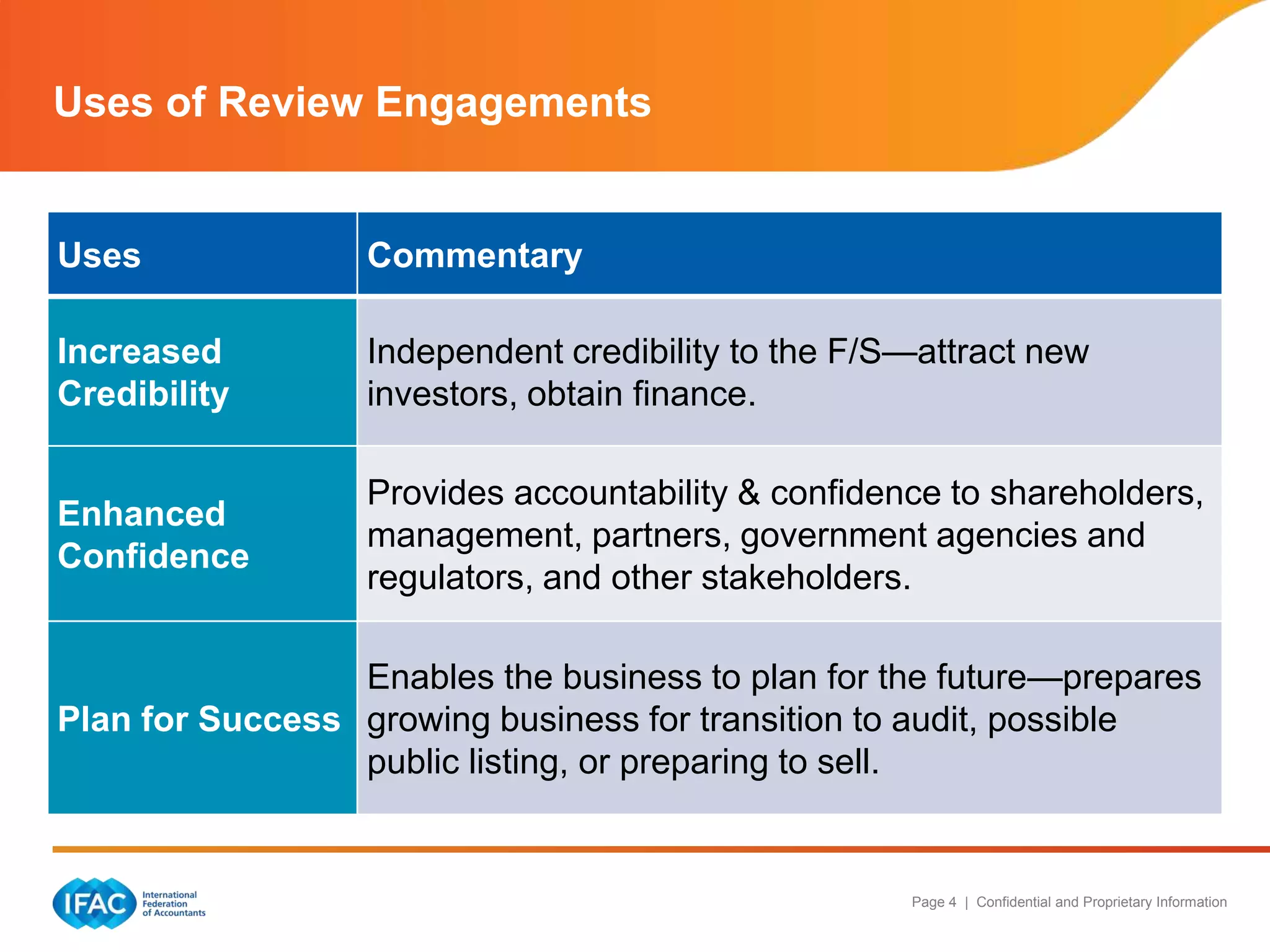

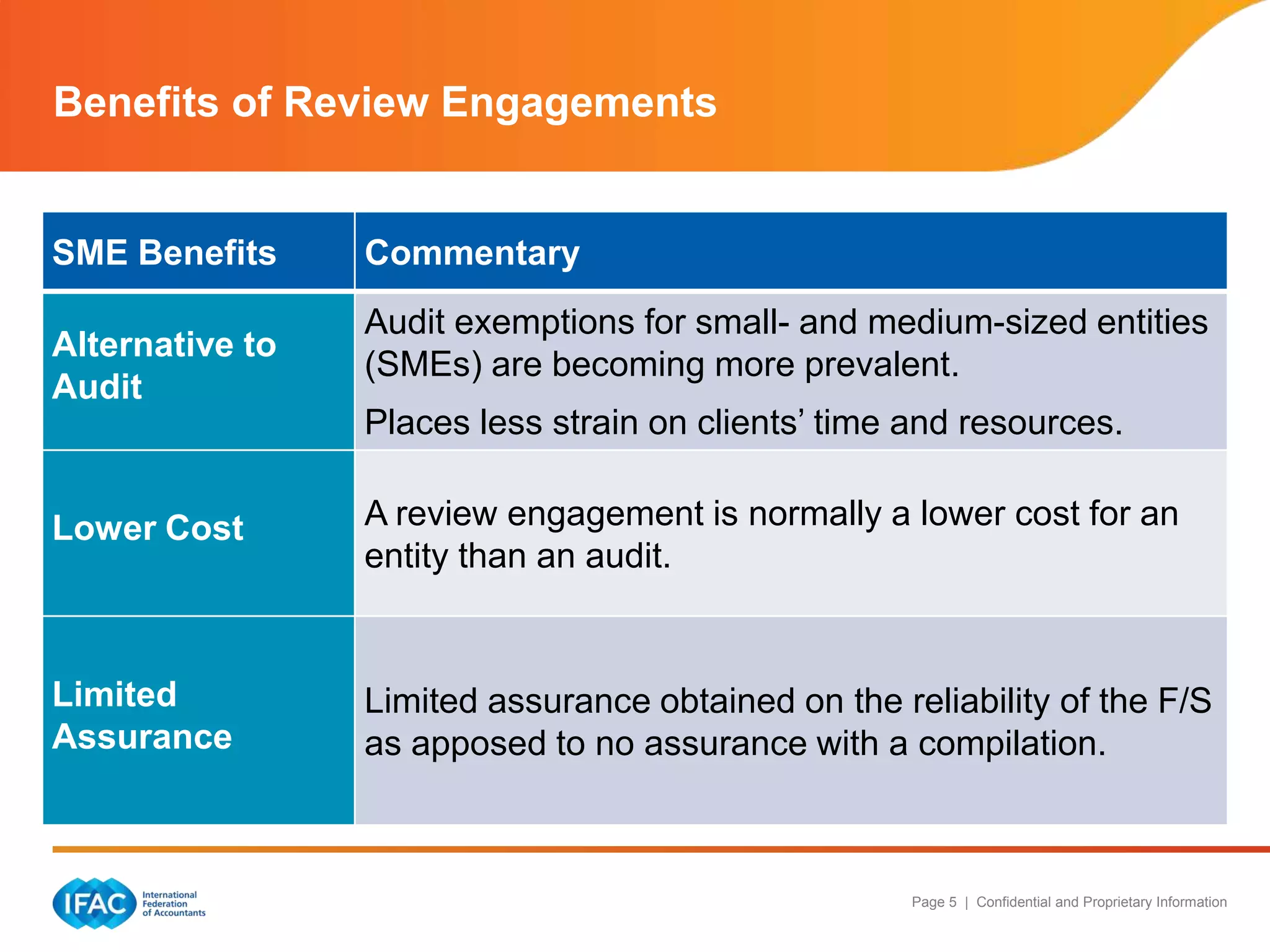

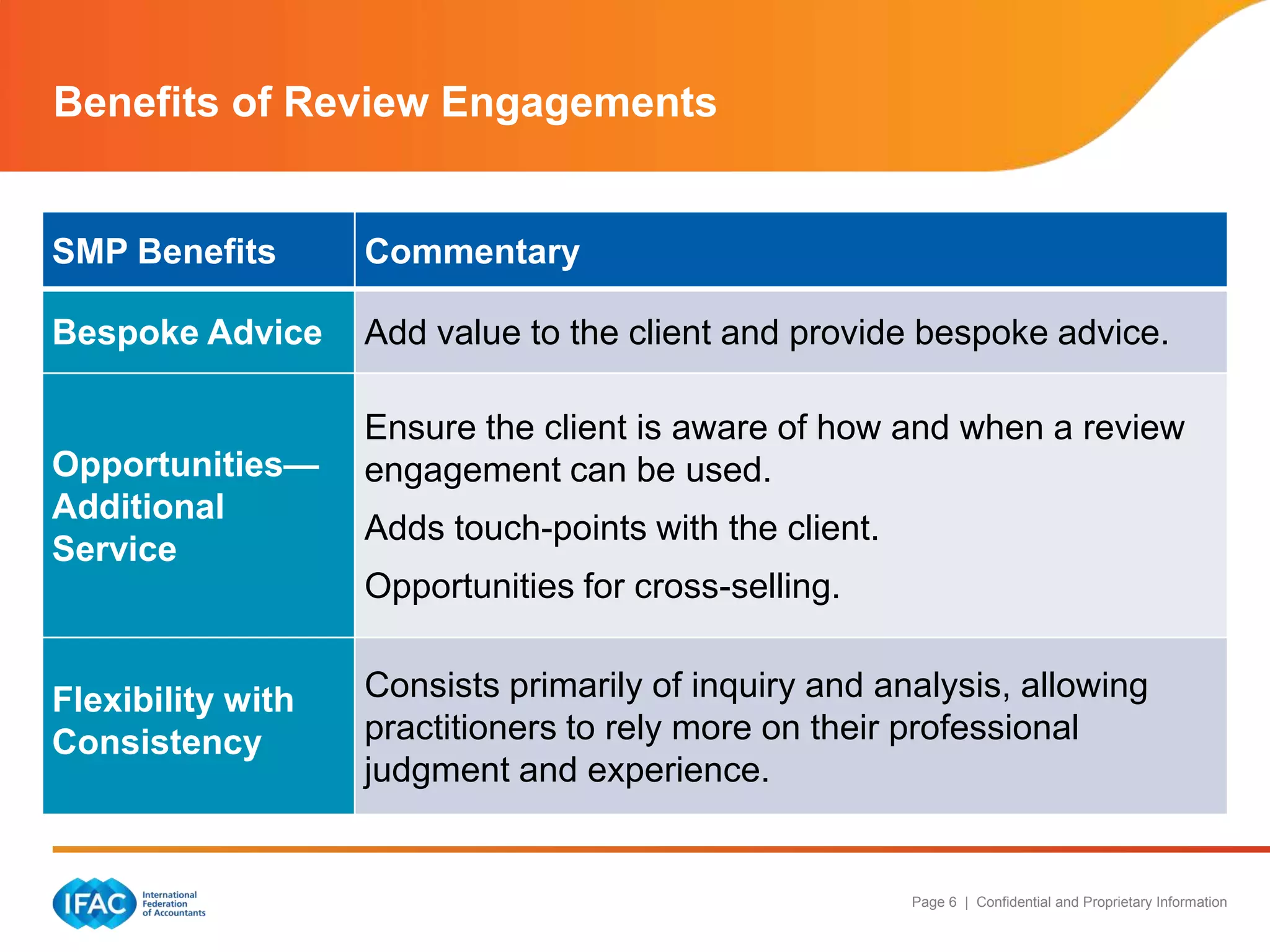

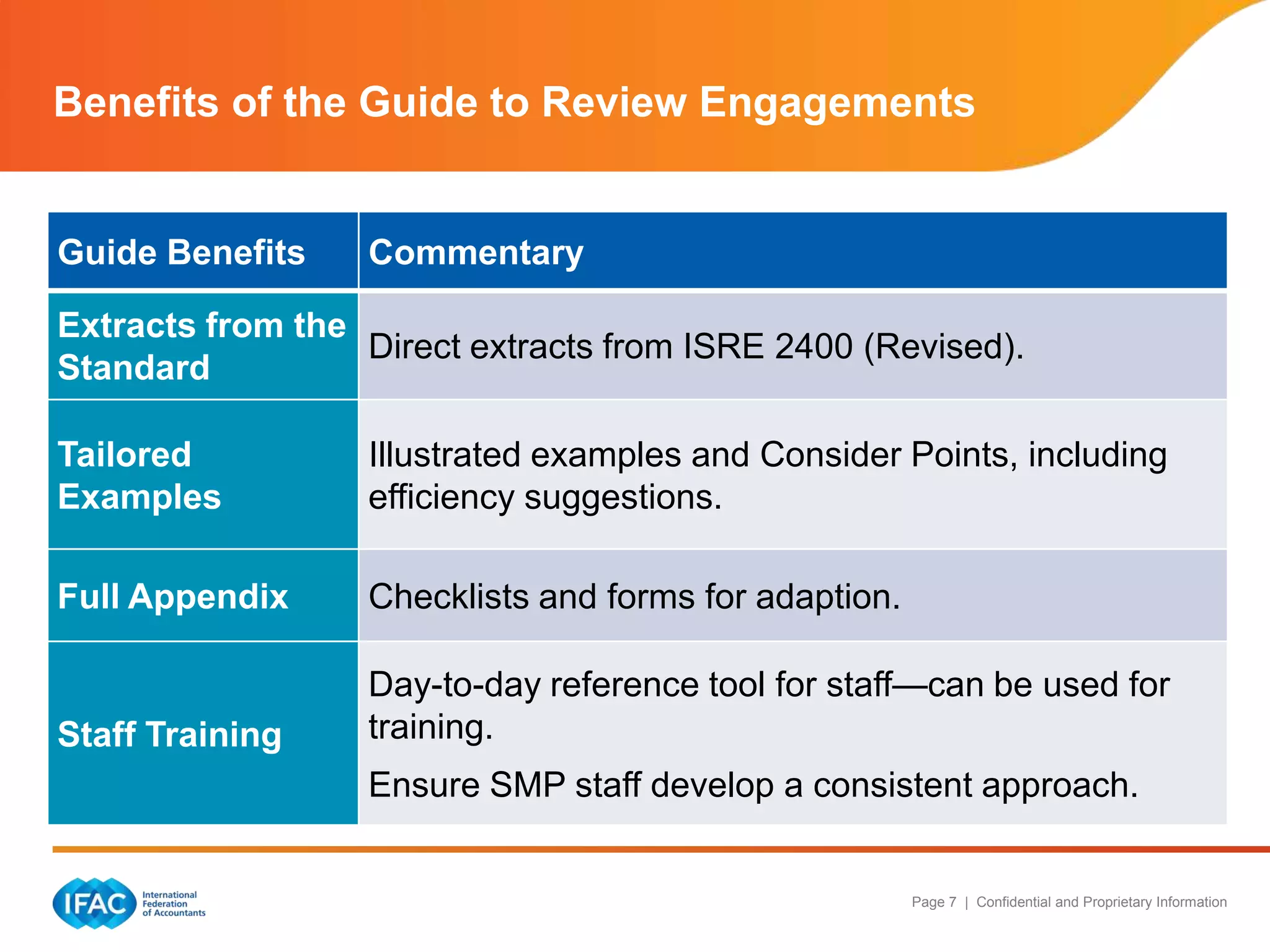

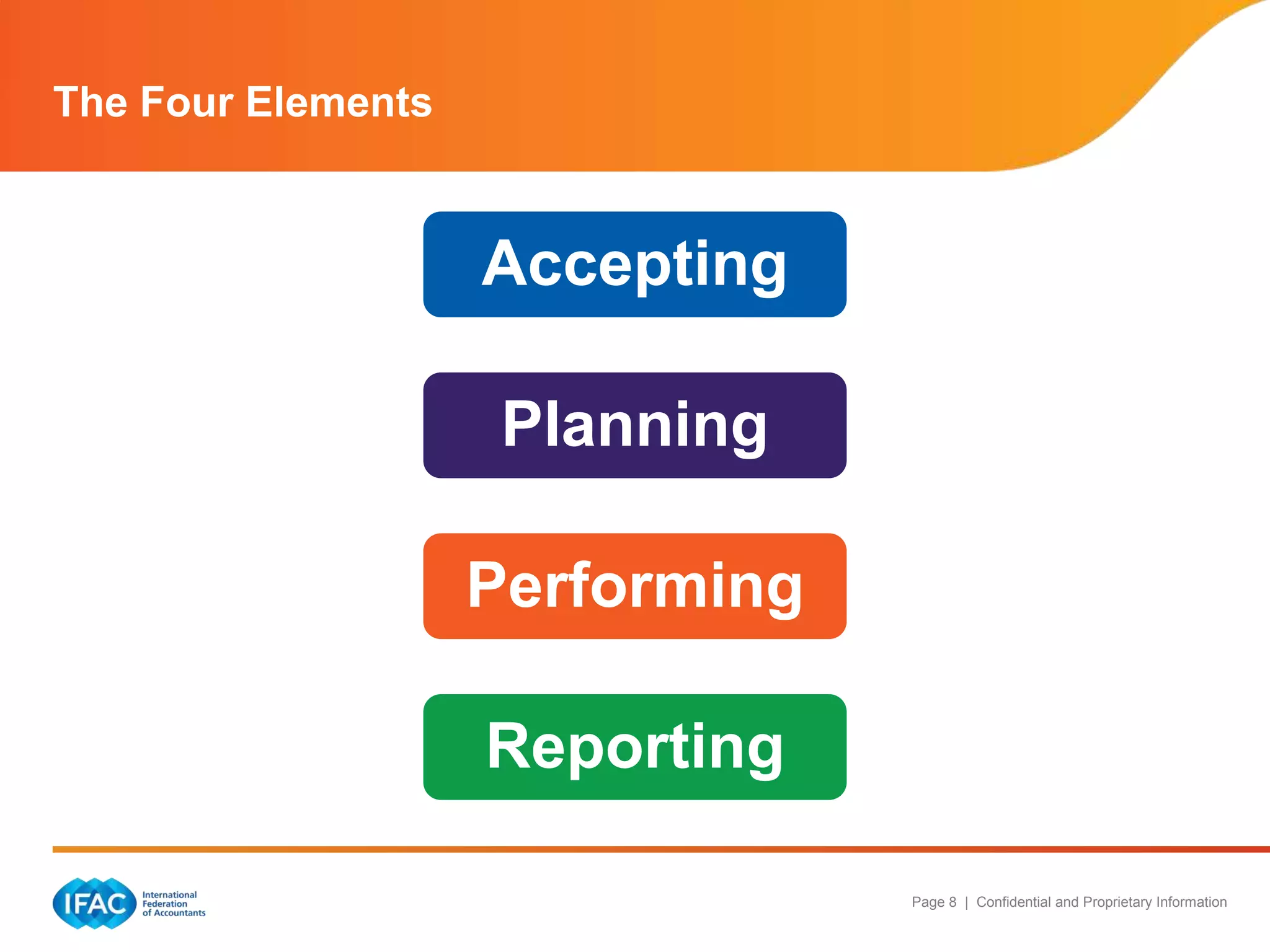

The IFAC guide to review engagements outlines the roles and benefits of review engagements for small and medium-sized practices (SMPs) and small and medium-sized entities (SMEs). It emphasizes the significance of independent credibility, enhanced confidence, and various advantages such as lower costs and the potential for bespoke advice. The guide serves as a reference tool for practitioners, offering resources and insights to ensure a consistent approach in review engagements.