Accounting for Lease, Income Tax, and Consolidation Entries

•Download as DOCX, PDF•

1 like•94 views

Hello Sir We are a premier academic writing agency with industry partners in UK, Australia and Middle East and over 15 years of experience. We are looking to establish long-term relationships with industry partners and would love to discuss this opportunity further with you. Thanks & Regards visit our website. www.onlineassignmenthelp.com.au www.freeassignmenthelp.com www.btechndassignment.cheapassignmenthelp.co.uk www.cheapassignmenthelp.com www.cheapassignmenthelp.co.uk/ http://www.cheapassignmenthelp.net/

Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Similar to Accounting for Lease, Income Tax, and Consolidation Entries

Similar to Accounting for Lease, Income Tax, and Consolidation Entries (20)

More from Nicole Valerio

More from Nicole Valerio (20)

Recently uploaded

Recently uploaded (20)

Accounting for Lease, Income Tax, and Consolidation Entries

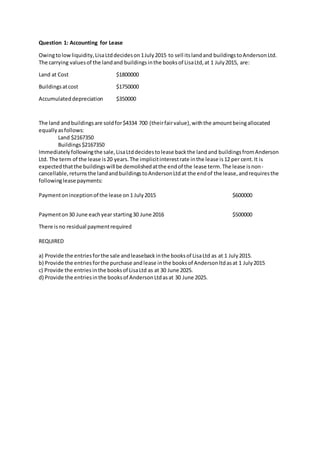

- 1. Question 1: Accounting for Lease Owingtolowliquidity,LisaLtddecideson1July2015 to sell itslandand buildingstoAndersonLtd. The carrying valuesof the landand buildingsinthe booksof LisaLtd,at 1 July2015, are: Land at Cost $1800000 Buildingsatcost $1750000 Accumulateddepreciation $350000 The land andbuildingsare soldfor$4334 700 (theirfairvalue),withthe amountbeingallocated equallyasfollows: Land $2167350 Buildings$2167350 Immediatelyfollowingthe sale,LisaLtddecidestolease backthe landand buildingsfromAnderson Ltd. The term of the lease is20 years.The implicitinterestrate inthe lease is12 per cent.It is expectedthatthe buildingswill be demolishedatthe endof the lease term.The lease isnon- cancellable,returnsthe landandbuildingstoAndersonLtdat the endof the lease,andrequiresthe followinglease payments: Paymentoninceptionof the lease on1 July2015 $600000 Paymenton30 June eachyear starting30 June 2016 $500000 There isno residual paymentrequired REQUIRED a) Provide the entriesforthe sale andleasebackinthe booksof LisaLtd as at 1 July2015. b) Provide the entriesforthe purchase andlease inthe booksof Andersonltdasat 1 July2015 c) Provide the entriesinthe booksof LisaLtd as at 30 June 2025. d) Provide the entriesinthe booksof AndersonLtdasat 30 June 2025.

- 2. Question 2: Accounting for Income Tax MR Limitedcommencesoperationson1 July2014 andpresentsitsfirst statementof comprehensive income andfirststatementof financial positionon30 June 2015. The statementsare prepared before consideringtaxation.The followinginformationisavailable: Statement of comprehensive income for the year ended 30 June 2015 Gross Profit 730000 Expenses: Administration expenses 80000 Salaries 200000 Long-serviceleave 20000 Warranty expenses 30000 Depreciationexpense-plant 80000 Insurance 20000 430000 Accounting profit before tax 300000 Assets and liabilities as disclosed in the statement of financial position as at 30 June 2015. Assets Cash 20000 Inventory 100000 Accounts receivable 100000 Prepaid insurance 10000 Plant-cost 400000 Less Accumulated depreciation 80000 320000 Total assets 550000 Liabilities Accounts payable 80000 Provision for warranty expenses 20000 Loan payable 200000 Provision for long-service leave expenses -20000 Total liabilities 320000 Net assets 230000 Otherinformation • All administrationandsalariesexpensesincurredhave beenpaidasat yearend. • None of the long-service leave expense hasactuallybeenpaid.Itisnotdeductible untilitis actuallypaid. • Warranty expenseswere accruedand,atyearend,actual paymentsof $10000 had beenmade (leavinganaccruedbalance of $20000). Deductionsare available onlywhenthe amountsare paid and notas theyare accrued. • Insurance wasinitiallyprepaidtothe amountof $30 000. At yearend,the unusedcomponentof the prepaidinsurance amountedto$10000. Actual amountspaidare allowedasa tax deduction. • Amountsreceivedfromsales,includingthose oncreditterms,are taxedatthe time the sale is made.

- 3. • The plantis depreciatedoverfive yearsforaccountingpurposes,butoverfouryearsfortaxation purposes. • The tax rate is 30 percent. REQUIRED Provide the journalentriesto accountfortax in accordancewithAASB 112. Question3: Consolidation SandyLtd acquired100 per centof the issuedcapital of BeachLtd on 30 June 2014 for$900 000, whenthe statementof financial positionof BeachLtd wasas follows: Assets $000 $000 Accounts receivable 70 Loan 300 Inventory 100 Land 400 Share holders' equity Property, plant and equip. 700 Share capital 500 Accumulated depreciation -270 Retained earnings 200 1000 1000 Additionalinformation • The tax rate is 30 percent. • Asat the date of acquisition,all assetsof BeachLtdwere at fairvalue,otherthanthe property, plantand equipment,whichhadafairvalue of $530000. Beach Ltd adoptsthe cost model for measuringitsproperty,plantandequipment.The property,plant andequipmentisexpectedto have a remainingusefullifeof 10 years,and noresidual value. • One yearfollowingacquisitionitwasconsideredthatBeachLtd's goodwill hadarecoverable amountof $60000. • BeachLtd declareda dividendof $40000 on 10 July2014, withthe dividendsbeingpaidfrompre- acquisitionretainedearnings. • The statementsof financial positionandstatementsof comprehensiveincome of SandyLtdand Beach Ltd one yearafteracquisitionare asfollows: Statements of financial position of Sandy Ltd and Beach Ltd as at 30 June 2015 Sandy Ltd Beach Ltd $000 $000 Assets Cash 80 40 Accounts receivable 50 50 Inventory 140 123 Land 600 400 Property, plant and equipment 900 700 Accumulated depreciation -300 -313 Investment in Beach Ltd 900

- 4. Total assets 2370 1000 Liabilities Accounts payable 100 10 Dividends payable 100 50 Loan 670 140 Shareholders' equity Share capital 1000 500 Retained earnings 500 300 2370 1000 Reconciliation of opening and closing retained earnings Profit after tax 400 190 Retainedearnings- 30June2014 300 200 Interim dividend -90 -40 Final dividend -110 -50 Retainedearnings- 30June2015 500 300 REQUIRED Prepare the consolidatedstatementof financial positionforthe above entitiesasat30 June 2015.