Recommended

Recommended

More Related Content

Similar to Valuation Report on Siemens-Gamesa Renewable Power Pvt. Ltd Assets

Similar to Valuation Report on Siemens-Gamesa Renewable Power Pvt. Ltd Assets (20)

Recently uploaded

Recently uploaded (20)

Valuation Report on Siemens-Gamesa Renewable Power Pvt. Ltd Assets

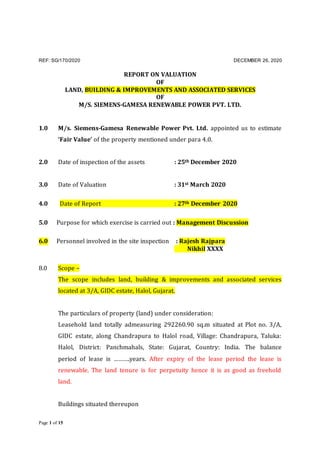

- 1. REF: SG/170/2020 DECEMBER 26, 2020 Page 1 of 15 REPORT ON VALUATION OF LAND, BUILDING & IMPROVEMENTS AND ASSOCIATED SERVICES OF M/S. SIEMENS-GAMESA RENEWABLE POWER PVT. LTD. 1.0 M/s. Siemens-Gamesa Renewable Power Pvt. Ltd. appointed us to estimate ‘Fair Value’ of the property mentioned under para 4.0. 2.0 Date of inspection of the assets : 25th December 2020 3.0 Date of Valuation : 31st March 2020 4.0 Date of Report : 27th December 2020 5.0 Purpose for which exercise is carried out : Management Discussion 6.0 Personnel involved in the site inspection : Rajesh Rajpara Nikhil XXXX 8.0 Scope – The scope includes land, building & improvements and associated services located at 3/A, GIDC estate, Halol, Gujarat. The particulars of property (land) under consideration: Leasehold land totally admeasuring 292260.90 sq.m situated at Plot no. 3/A, GIDC estate, along Chandrapura to Halol road, Village: Chandrapura, Taluka: Halol, District: Panchmahals, State: Gujarat, Country: India. The balance period of lease is ……….years. After expiry of the lease period the lease is renewable. The land tenure is for perpetuity hence it is as good as freehold land. Buildings situated thereupon

- 2. REF: SG/170/2020 DECEMBER 26, 2020 Page 2 of 15 The building services under the scope includes certain machinery assets. This includes HVAC system, solar power plant, RO plant, sewer water treatment plant, fire hydrants and electrical reticulation assets. The scope of the assets included certain assets from FAR. The scope is as following. Asset status Number of line entries Gross Value Assets under scope 478 1,957,399,304 Assets under scope but excluded - Consumables 3 46,637 Assets under scope but excluded - Disposed 4 738,063 Assets under scope but excluded - No acquisition costs 233 - Out of scope entries 1759 2,479,509,267 Total 2477 4,437,693,271 The valuation is a retrospective in nature as the date of valuation is in before the date of inspection. The valuation is based on the information that was known or available at the date of valuation. As the inspection on a retrospective basis is problematic, we have relied on the historical evidence, observations and notes regarding the asset’s condition where possible. We have endeavored to verify information relied upon. 9.0 Basis of Valuation: Cost approach 10.0 Premise of Value adopted Current use of the subject assets is the highest and best use. The estimation of the value the assets is carried out on ‘as is where is basis’ and the ‘value-in situ’.

- 3. REF: SG/170/2020 DECEMBER 26, 2020 Page 3 of 15 11.0 The report is based on scan copy of the following information furnished by the client and inspection carried out by us:- 11.1 Registered Lease deed. 11.2 Plan approvals / approved plan by local authority – Gujarat Industrial Development Corporation. 11.3 Fixed Asset Register 12.0 Definitions of various terms used : 12.1 Fair Value: As per IAS 113, Fair value is defined as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. 13.0 Procedure Adopted 13.1 Property has been inspected. The area of the land as per the lease deed and approved layout plans provided to us has been relied upon. 13.2 The built-up area statement given by the company officials have been relied upon. Random measurements have been carried out to check the authenticity of the built-up area statement. Wherever the built-up area of the building is not matching with the statement given we have considered the built-up area as per our measurements. 13.3 The Gross Historical Cost of the investment in the Land, building and Building services has been obtained from the Fixed Asset Register and discussions with the company official has been done on the site itself.

- 4. REF: SG/170/2020 DECEMBER 26, 2020 Page 4 of 15 13.3 Sale instances have been obtained from the various sources and data bank. 13.4 Enquiry with estate brokers and developers operating in the area to ascertain the current price. 14.0 Valuation methodology In determining the fair value of the subject assets we have adopted the market and cost approach as the valuation method for assets under scope. Cost approach - For the purpose of this analysis, the cost approach was used to value the subject assets. By using this approach we recognised the contributory value associated with the necessary installation, engineering, and set-up costs related to the installed complement of equipment. Market approach - The market approach was applied where we had sufficient information in respect of comparable sales and offering data in the marketplace. i.e. Land. 14.1 Cost approach has been considered. The land has been valued using the market approach. The depreciated replacement cost for the buildings have been estimated by reducing the depreciation from the replacement cost new. Land: Following factors have been taken into consideration:- Transactions recorded in the Office of Sub-Registrar of Documents. Condition, potential, location and marketability of the property.

- 5. REF: SG/170/2020 DECEMBER 26, 2020 Page 5 of 15 Asking price obtained by oral inquiry. Peculiarity of real estate market. Comparison of the subject land with the available sale instances and asking price instances. 14.2 It is pertinent to point out that ‘value to the seller’ and ‘value to the buyer’ are different. Due to subjective considerations of buyers and sellers, eagerness to complete transaction, negotiation skill, price at which transaction takes place differs from market value because price is a fact and value is an estimate of what price to be conducted ought to be. 15.0 Valuation 15.1 Locational Aspects : The subject property is situated at land bearing plot no. 3/A, GIDC estate, along Chandrapura to Halol road, Village Chandrapura, Taluka Halol, District Panchmahals, State: Gujarat, Country: India. Total land area is 292260.90 sq.m Demarcation of the land as per lease deed: On or towards East by Plot no. 3/B On or towards West by Estate boundary and Plot no. 4 On or towards North by Halol-Champaner road

- 6. REF: SG/170/2020 DECEMBER 26, 2020 Page 6 of 15 On or towards South by Champaner-Shivrajpur railway line Demarcation of the land as per actual: On or towards East by Plot no. 3/B, GIDC estate occupied by WINDAR On or towards West by Estate boundary and Plot no. 4 of GIDC estate On or towards North by Halol-Savli state highway road On or towards South by WalkChampaner-Shivrajpur railway line The subject property is situated within the limits of village Chandrapura and just situated opposite to the road leading to the ‘Gamthal’ of Chandrapura village. This subject property abuts state highway connecting Halol-Savli state highway. There is a very good industrial development in Chandrapura village and surrounding villages viz. Muvala, Khakhariya, Madhvas, Rampura etc. Large industrial units of many reputed companies are having their manufacturing facilities in this region to name a few CEAT, Saint-Gobain, The Supreme Industries Ltd., Sisecam Flat Glass India, ABB India Ltd., Valmont, MG Motors, TOTO, L M Wind Turbine etc. Many small scale units are situated within old GIDC estate at Halol which is situated about 2 km distance from the subject property The subject property abuts good motorable road of 24 m width that connects Chandrapura village with Madhvas and further to Halol-Godhra state highway.

- 7. REF: SG/170/2020 DECEMBER 26, 2020 Page 7 of 15 It is situated about 4 kms away from the four cross roads near M G Motors along the Halol-Godhra highway. The skilled and unskilled workmen are available from nearby villages and towns within a comfortable distance of 10 kms to 20 kms The International Airport and Railway station at Vadodara are available within comfortable distance of 40 to 50 km from the subject property. The subject site is already connected with necessary power supply from MGVCL. The water is supplied by GIDC. Demand / Supply aspect : There is good demand for land in this region for using it for industrial purposes as can be judged from the land transactions occurred during the past 3 years recent past. Market Approach: Following information has been considered while estimating the market value of the subject land. 1. A leasehold land situated within GIDC estate which is being developed under the banner of ‘Mascot Industrial Park’ (earlier Navkar Industrial Park) situated along the Chandrapura to Savli road, totally admeasuring 49170.57 sq.m is available for purchase or on lease. The

- 8. REF: SG/170/2020 DECEMBER 26, 2020 Page 8 of 15 minimum plot size is 511 sq.m and the offer price is ₹ 6458 to ₹ 7535 per sq.m. These are the tentative offer price and subject to negotiations. The offer price is for a very small size of plots compared to the size of the subject property. 2. M/s. Shaily Engineering Plastics Ltd. had acquired a large piece of freehold land by executing four separate sale deeds in the month of July 2018. The land purchased is of agricultural nature for bonafied industrial use. The total area of land purchased is 72640 sq.m and the sale consideration paid is ₹ 13,45,95,143/-. The average rate yielded by these transactions is ₹ 1853 per sq.m. The subject land under valuation is 4 times bigger than this land. 3. M/s. Inabensa Bharat Private Ltd sold the industrial nature of land admeasuring 91712 sq.m along with 22616 sq.m of industrial shed type structures to M/s. Derit Infrastructure Private Ltd in the month of November 2017 for total sale consideration of ₹ 58,25,12,943/-. The subject land under valuation is 3 times bigger than this land. 4. M/s. Derit Infrastructure Private Ltd sold the industrial nature of land admeasuring 91712 sq.m along with 22616 sq.m of industrial shed type structures to M/s. Valmont Structures Private Ltd. in the month of August 2018 for total sale consideration of ₹ 67,14,05,430/-. The subject land under valuation is 3 times bigger than this land. Considering average depreciated rate of ₹ 16146 per sq.m of cost of construction of the structures the rate yielded by the land as per this transaction comes to ₹ 3339 per sq.m. Overall ₹ 7321 per sq.m is the rate yielded by the land (including building) as per this transaction.

- 9. REF: SG/170/2020 DECEMBER 26, 2020 Page 9 of 15 5. There is 15.26% appreciation in the asset value during past 9 months as per transactions mentioned at Sr. no. 3 and 4 above. The properties available for purchase as well as transaction of large pieces of lands as mentioned above are situated along the Halol (Chandrapura) to Savli main road. The location of the subject property on the same road and is slightly better than the sale instances. Considering the above information and analysis, I estimate the market value of the leasehold land at ₹ 2500 per sq.m which is fair and reasonable in my opinion. Market Value: Total Area of land : 292260.90 sq.m (as per Sale deeds) Estimated Rate of developed Land : ₹ 2500 per sq.m Market Value of land : 292260.90 sq.m x ₹ 2500/- : ₹ 73,06,52,250.00 Say ₹ 73,00,00,000.00 Transfer fee payable 15% of present Allotment price i.e. 15% of Rs. 1320 per sq.m = Rs. 198 per sq.m. Transfer fee Rs. 57867658.20 Say Rs.5,79,00,000/- Halol – Rs. 810 per sq.m Halol (New) – Rs. 1320 per sq.m (This is Chandrapura) Halol (Expansion) – Rs. 1590 per sq.m (This is Madhvas)

- 10. REF: SG/170/2020 DECEMBER 26, 2020 Page 10 of 15 10.0 General Remarks 12.1 The identification of the property was done by Mr. Balraj Kartikey of M/s. Siemens-Gamesa 12.2 At land is a leasehold land having total lease period of 99 years and unexpired period of lease 11.0 Assumptions and Limiting Conditions 11.1 This valuation exercise has been carried out on urgency basis as there is urgent requirement of estimation of value at the client’s end. 11.2 That we have totally relied on the representative of company and sketch plan provided to us for identification of property. 11.3 We have not done any site analysis related to conditions and services for the purpose for which property is developed or intended to be developed. 11.4 That we have not carried out land survey / soil testing / ground water availability and its quality and are unable to report that the property is free of any such fault, infestation or defect of any other nature including inherent weakness, If any investigation identifies any structural defect in the property our report may require revision; 11.5 That there are no dues towards any Government body or any other authority; 11.6 That there are no encumbrances, outgoings, elements, restriction or charges on property which may have detrimental effect upon the value or marketability; 11.7 That the subject property and its value are unaffected by any matters which would be revealed by inspection of property records or by statutory notice and that neither the property nor its condition, nor its use, nor its intended use, is or will be unlawful;

- 11. REF: SG/170/2020 DECEMBER 26, 2020 Page 11 of 15 11.8 Unless advised by the company or representative of the company, we do not normally make allowance for any liability already incurred, but not yet discharged, in respect of balance land cost, completed works, or obligations in favour of contractors, subcontractors or any other professional. 11.9 Any sketch, plan or map in this report is included to assist the reader in visualizing the property. We have made no land survey of the property and assume no responsibility in connection with such matters. 11.10 The property is valued on the assumption that it is free and clear of all mortgages encumbrances and other outstanding premiums and charges. 11.11 The ascertaining liability towards Government Authority or any third party is out of the scope of this assignment. If there exists any liability on the property the same need to be deducted from the Market Value of the property. 11.12 Market values are without taking into consideration any liability to taxation on sale or the costs involved in effecting a sale. 11.13 We are orally informed by the client that no notice has been served by any government body of acquiring the same for any public purpose. 11.14 Due to peculiarity of real estate transactions in our country oral information furnished by various agencies is relied in good faith. 11.15 The market is being impacted by the uncertainty caused by the COVID‐19 pandemic. As at the date of valuation we consider that there is market uncertainty resulting in significant valuation uncertainty. 11.16 This valuation is therefore reported on the basis of ‘significant valuation uncertainty’. As a result, less certainty exists than normal and a higher degree of caution should be attached to our valuation than normally would be the case. Given the unknown future impact that COVID‐19 might have on markets, we recommend that the user(s) of this report review this valuation periodically. 11.17 This valuation is current at the date of valuation only. The value assessed herein may change significantly and unexpectedly over a relatively short period of time (including as a result of factors that the Valuer could not

- 12. REF: SG/170/2020 DECEMBER 26, 2020 Page 12 of 15 reasonably have been aware of as at the date of valuation). We do not accept responsibility or liability for any losses arising from such subsequent changes in value.” 14.0 Caveat 14.1 Neither the whole nor any part of this valuation or report or any reference to it may be included in any published document, circular or statement nor published in any without the Valuer’s prior written approval of the form and context in which it may appear. 14.2 The report is confidential to the clients, their professional advisors for the specific purpose to which they refer. The valuer disclaims all responsibility and will accept no liability to any other party. 14.3 This valuation report is prepared for management information purpose hence it is valid for this purpose only and it should not be utilized for any other purpose. 14.4 The valuer is not required to give testimony or to appear in court by reason of this, as appearance in the court is out of scope of the assignment. 15.0 Conclusion: The Fair Value of the subject property, as on date of valuation, is estimated at ₹ 3,08,00,000/- (Rupees Three Crore Eight Lakh only) which is fair and reasonable in my opinion.

- 13. REF: SG/170/2020 DECEMBER 26, 2020 Page 13 of 15 Rajesh P. Rajpara Prop. Of Hem AssetValuers Govt. Regd. Valuer of Immovable Property Regd. No. Cat-I/333 Govt. Regd. Valuer of Machinery and Plant Regd. No. Cat-VII/79 Master of Valuation (Real Estate) Master of Valuation (Plant and Machinery) Fellow of Institution of Valuers, India. Member of Institution of Surveyors, India. Place: Vadodara. (Valuation Surveying) (M/1276/IS) Date: 04.05.2019 Founder Member of CVSRTA, India. ANNEXURE – I: SKETCH PLAN OF THE LAND

- 14. REF: SG/170/2020 DECEMBER 26, 2020 Page 14 of 15 ANNEXURE – II: GOOGLE IMAGE SHOWING LOCATION OF THE SUBJECT LAND

- 15. REF: SG/170/2020 DECEMBER 26, 2020 Page 15 of 15