2. Why do firms go public?

- In many cases a significant motivation is to raise fresh equity capital

- Taking a firm public offers a complete exit or diversification route for initial

owners

- Compared to a privately owned firm, a public firm is usually more visible to

investors

- Shares become considerably more liquid if they are traded in public markets

- Being a public firm means better access to capital markets and bank financing

- Being a public firms increases reputation in product markets and with suppliers

- Setting up stock and option-based compensation plans for employees becomes

easier

5. Initial Public Offerings (IPOs)

IPOs: An important exit route for the venture capital industry

Year

Total M&A

Deals

Deals with

Disclosed Values

Total Disclosed

Value

Average Value

($ mil)

Number

of IPOs

Total Offer

Amount

Average Offer

Size ($ mil)

2002 319 154 7586,7 49,3 22 2109,1 95,9

2003 284 119 7460,1 62,7 29 2022,7 69,8

2004 346 187 15919,6 85,1 94 11378 121

2005 351 166 17410,6 104,9 57 4485 78,7

2006 370 160 18693,6 116,8 57 5117,1 89,8

2007 360 160 28406,7 177,5 86 10326,3 120,1

2008 260 96 13915,4 145 6 470,2 78,4

Source: National Venture Capital Association

US Data, M&As and IPOs that involve venture capital backed entitites:

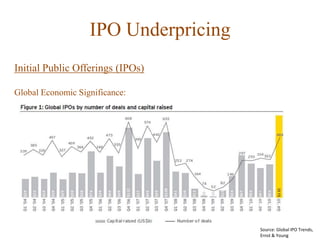

6. Initial Public Offerings (IPOs)

IPOs: An important exit route for the Venture Capital industry

Source: Bessler and Seim (2011)

European Data:

7. The costs of going public

These include direct costs such as underwriting fees and gross spread, legal and

accounting expenses. Since many of these costs are fixed, there are considerable

economies of scale. In the U.S., for example, issues raising $5 million or less incur

direct expenses of 18.2% while those raising over $100 million pay on average

6.8%.

More importantly, there is an indirect cost: initial underpricing of the shares offered.

An IPO is said to be underpriced if

(Closing price on day 1 in the stock market − offer price)/offer price > 0

Underpricing is a global phenomenon.

8. IPO underpricing – international evidence

Country Study Sample period Sample size Initial return (%)

USA Ibbotson et. al.(1994) 1960-92 10626 15.3

USA Ritter (1987) 1977-82 664 14.8

Australia Finn and Higham (1988) 1966-78 93 29.2

Australia Lee et. al. (1994) 1976-89 266 11.9

Canada Jog and Srivastava (1996) 1971-92 254 7.4

Finland Keloharju (1993) 1984-92 91 14.4

France Jacquillat (1986) 1972-86 87 4.8

Germany Ljungqvist (1996) 1970-93 180 9.2

G. Britain Jenkinson and Mayer (1988) 1983-86 143 10.7

Italy Cherubini and Ratti (1992) 1985-91 75 29.7

Japan Jenkinson (1990) 1986-88 48 54.7

Japan Kaneko and Pettway (1994) 1989-93 37 12.0

Sweden Rydqvist (1993) 1970-91 213 39.0

Korea Dhatt et. al. (1993) 1980-90 347 78.1

Taiwan Chen (1992) 1971-90 168 45.0

Turkey Kiymaz et. al. (2000) 1990-96 163 13.1

9. IPO underpricing – international evidence (continued)

2000-2006 IPOs from Banerjee et. al (2012) – initial returns

Mean % N Mean % N

Australia 16.59 696 Ireland 10.29 25

Austria 23.76 34 Israel 23.34 42

Belgium 10.36 32 Italy 7.87 215

Brazil 18.37 46 Japan 45.14 890

Canada 39.13 784 Luxembourg 26.68 15

China 57.14 590 Malaysia 31.18 295

Denmark 13.48 27 Netherlands 20.00 44

Finland 14.61 25 New Zealand 20.66 38

France 11.30 353 Norway 4.33 45

Germany 43.13 333 Philippines 17.27 19

Greece 14.44 53 Poland 45.50 23

Hong Kong 22.21 479 Russia 8.82 10

India 25.01 9 Singapore 24.88 296

Indonesia 52.25 48 South Africa 12.94 18

10. IPO underpricing – international evidence (continued)

2000-2006 IPOs from Banerjee et. al (2012) – initial returns

Mean % N

South Korea 54.57 192

Spain 10.98 45

Sweden 21.79 73

Switzerland 14.41 39

Taiwan 17.25 260

Thailand 19.15 143

United Kingdom 23.29 840

United States 24.00 1700

All 29.11 8776

12. IPO underpricing – Netscape example

Netscape’s August 1995 IPO

- Morgan Stanley, lead underwriter

- Preliminary price range $12-14

- Offer price was adjusted upwards by Morgan Stanley after the road shows, 5 million

shares were sold at $28 per share.

- First-day closing price $58.25 - $151 million was left on the table (($58.25 – $28) x 5m)

- Marc Andreessen, a co-founder of the firm, owned 1 million shares (2.7% of the firm).

The value of his stake went from an estimated $12-14 million to roughly $58 million as

of the first day of trading.

- whereas 2.7% of the $151 million left on the table is around $4 million.

13. IPO underpricing – theoretical explanations

Signaling-based theories (Grinblatt and Hwang (1989), Allen and Faulhaber (1989),

Welch (1989)): In order to signal firm quality so that they can subsequently issue seasoned

equity at more favorable prices, rational owners intentionally underprice.

Implication: there is a positive relationship between underpricing and both the probability

of SEO and the amount of SEO. Empirical evidence: mixed.

Principal-agent models (Baron (1989)): In order to compensate underwriters for the use of

their superior information, issuers rationally let underwriters underprice in an environment

in which underwriters have superior information about demand for the new shares.

Implication: IPOs of underwriting firms should not be underpriced. Empirical evidence:

Muscarella and Vetsuypens (1989) find that these IPOs are underpriced as well.

14. IPO underpricing – theoretical explanations

Asymmetric information-based theories (Rock (1986), Benveniste and Spindt (1989),

Benveniste and Wilhelm (1990)):

Rock (1986): In order to avoid the ‘lemons’ problem of adverse selection, issuers rationally

underprice, in an informational environment in which some investors are perfectly

informed.

Implication: underpricing returns tend to the riskless rate when rationing-adjusted.

Empirical evidence: mostly supportive for countries where book-building is not used.

Benveniste and Spindt (1989), Benveniste and Wilhelm (1990)): underwriters can entice

‘informed’ investors to truthfully reveal their superior information pre-sale; underpricing

ensures incentive-compatibility.

Implication: offers for which positive information is revealed will be priced towards or

beyond the upper end of the initial price range, however, the final price will be set below

the full-information price to allow regular investors to be compensated via underpricing.

Empirical evidence: supportive in the U.S. where book-building process is prevalent.

15. IPO underpricing – The Rock (1986) model in more detail

Consider a setting where the true value of shares that are offered in an IPO are known by

some investors, i.e. “informed investors”, while others, the “uninformed investors” do not

know this true value.

Suppose that informed investors have $100 to invest, uninformed investors also have $100

to invest and 10 IPO shares are offered at $8 per share while the true value is $10 per share.

This IPO is therefore underpriced. Informed investors would ask for a $100 allocation in

total, and uniformed ones, since they are assumed to not discriminate between IPOs, also

ask for $100 worth of shares. Hence, IPO shares would have to be rationed in this case as

there is only $80 worth of supply but $200 worth of demand in total for these shares.

With a pro rata allocation, informed investors would get $40 worth of shares, so 5 shares at

$8 per share and uninformed investors would also get 5 shares at that price. At the end of

the first day of trading when price goes up to $10 per share, each class of investor would

therefore attain a profit of $10 in total ($2 dollars per share * 5 shares).

16. IPO underpricing – The Rock (1986) model in more detail (continued)

Now consider what happens when an IPO is overpriced. The critical assumption is that

uninformed investors do not condition their demand for IPO shares on whether the shares

are underpriced or overpriced, they submit indications of interest regardless. Informed

ones, on the other hand, shy away from overpriced shares.

Suppose as before that informed investors have $100 to invest, uninformed investors also

have $100 to invest and 10 IPO shares are offered at $12.50 per share while the true value

is $10 per share.

This IPO is therefore overpriced. Informed investors would not ask for any allocation, they

would simply walk away from the deal. Uninformed investors however, ask for $100 worth

of shares as before. Now, there is no rationing, the seller would be able to sell only 8 shares

and these all would go to the uninformed investors.

At the end of the first day of trading, the shares would be worth $10 each and uniformed

investors would lose in total $2.50 * 8 = 20 dollars.

17. IPO underpricing – The Rock (1986) model in more detail (continued)

So how should we think about IPO pricing on average in equilibrium in such a setting? The

crucial point is when IPOs are underpriced, uninformed investors are crowded out by

informed investors while when IPOs are overpriced, they get full allocations since

informed investors show no interest in shares they know are overpriced.

Note that if underpricing and overpricing happened with 50-50 probability and in equal

dollar amounts (e.g. in our first example the IPO was underpriced by 20 dollars in total (10

shares * $2) and in the second example it was overpriced by 20 dollars (8 shares * 2.50)),

uninformed investors would lose money on average.

If the underwriter wants to keep uninformed investors in the game, it will need to produce

underpricing in equilibrium, in which, uniformed investors would just break even and

informed investors would of course be consistently profitable.

Because of the disadvantageous asymmetry in allocation that uninformed investors face

that we just illustrated, the only way they could break even in equilibrium would be if IPO

shares on average were underpriced.

18. IPO underpricing – theoretical explanations

Behavioural theories

Loughran and Ritter (2002): If an IPO is underpriced, pre-issue stockholders are worse off

because their wealth has been diluted. If an entrepreneur receives the good news that he or

she is suddenly unexpectedly wealthy because of a higher than expected IPO price, the

entrepreneur doesn't bargain as hard for an even higher offer price. This is because the

person integrates the good news of a wealth increase with the bad news of excessive

dilution. The individual is better off on net. Underwriters take advantage of this mental

accounting and severely underprice these deals. It is these IPOs where the offer price has

been raised (a little) that leave a lot of money on the table when the market price when

trading starts goes up a lot.

19. Loughran and Ritter

(2002): “Prospect

theory argues that

when an individual is

faced with two

related outcomes, the

individual can either

treat them separately

or as one.” The case of

Netscape

20. IPO underpricing – the partial adjustment phenomenon

Hanley (1993) and Loughran and Ritter (2002) observe that there is a positive correlation

between the money left on the table and the adjustments made by the underwriter to the

expected offer price. They also note that a minority of offerings is responsible for most of

the average underpricing. This is reflected in the median underpricing being in most cases

much smaller than the mean underpricing in the Benarjee samples, for example:

Mean % Median % N

Australia 16.59 5.08 696

Italy 7.87 0.85 215

Japan 45.14 20.71 890

Canada 39.13 6.02 784

Malaysia 31.18 14.21 295

Netherlands 20.00 4.94 44

Germany 43.13 15.65 333

Poland 45.50 16.81 23

Hong Kong 22.21 5.26 479

Singapore 24.88 9.47 296

Indonesia 52.25 23.11 48

United Kingdom 23.29 9.21 840

United States 24.00 5.00 1700

All 29.11 8.18 8776

21. IPO underpricing – the partial adjustment phenomenon

Loughran and Ritter (2002) find that the mean underpricing for an offering whose final

offer price is below the offer range as anticipated by the underwriter in earlier stages is 4%.

On the other hand, for issues that manage to sell at prices that are greater than their offer

ranges, the mean underpricing is 32%.

22. Ljungqvist, Nanda and Singh (2004) – “Sentiment” investors

Another attempt at introducing behavioural dimensions to the explanation of the IPO

underpricing phenomenon comes in the form of a multi-period model by Ljungqvist,

Nanda and Singh (2004).

Key assumption: There are sentiment investors who hold excessively optimistic beliefs

about the future prospects for the IPO company alongside rational investors.

The issuer’s objective is to maximize the excess valuation over the fundamental value of

the stock.

Flooding the market with stock will depress the price, so the optimal strategy involves

holding back stock in inventory to keep the price from falling.

23. Ljungqvist, Nanda and Singh (2004) – (continued)

Eventually, nature reveals the true value of the stock and the price reverts to fundamental

value. That is, in the long-run IPO returns are negative, consistent with the empirical

evidence.

This assumes the existence of short sale constraints, or else arbitrageurs would trade in

such a way that prices reflected fundamental value even in the short term.

The optimal mechanism involves the issuer allocating stock to ‘regular’ institutional

investors for subsequent resale to sentiment investors, at prices the regulars maintain by

restricting supply. Because the hot market can end prematurely, carrying IPO stock in

inventory is risky, so to break even in expectation regulars require the stock to be

underpriced.

24. Ljungqvist, Nanda and Singh (2004) – (continued)

Related Empirical Results:

• Ofek and Richardson (2003) show that high initial returns occur when institutions sell

IPO shares to retail investors on the first day, and that such high initial returns are followed

by sizeable reversals to the end of 2000, when the ‘dot-com bubble’ eventually burst. This

is the pattern Ljungqvist, Nanda, and Singh (2004) predict.

• Using German data on IPO trading by 5,000 retail customers of an online broker, Dorn

(2003) documents that retail investors overpay for IPOs following periods of high

underpricing in recent IPOs, and for IPOs that are in the news. Consistent with the

Ljungqvist, Nanda, and Singh (2004) model, he also shows that ‘hot’ IPOs pass from

institutional into retail hands. Over time, high initial returns are reversed as net purchases

by retail investors subside, eventually resulting in underperformance over the first six to 12

months after the IPO.

25. Methods of selling shares

• Firm-commitment offers

• Best-efforts offers

• Offers for sale

• Private placements

• Book-building with when-issued trading

• Introductions

26. Methods of selling shares

• Firm-commitment offers

Widely used in the U.S., almost all IPOs over $10 million are firm-commitment.

The process: a syndicate of investment banks led by one or two lead banks agree to market

and sell the issue at a price that is determined after the ‘book-building’ process.

Book-building involves obtaining non-binding indications of interest from large, mostly

institutional, investors, at marketing meetings known as ‘road shows’.

• Best-efforts offers

Tend to be used only by small companies in the U.S.

The process: the investment bank does not underwrite the shares but agrees to distribute them.

If a certain proportion of shares remain unsold the issue may be withdrawn. The bank usually

has 90 days to sell the minimum amount.

• Offers for sale

Widely used in the U.K. in the 1990s, especially for larger offerings, currently rarely used..

The process: the company will sell all the shares to an issuing bank who in turn arranges the

issue to be sub-underwritten. The price is determined up to ten days in advance of the

distribution. The public then sends requests for allocation to the issuing bank. Allocations are

pro-rated in the event of over-subscription

27. Methods of selling shares

• Private placements

Used in the U.K. for smaller offerings.

The process: similar to a firm-commitment offer, but large investors are invariably the

clients of private placements.

• Book-building with when issued-trading

The prevalent method by far in Germany.

The process: similar to a firm-commitment offer, but has a when-issued trading stage in

which investors begin trading soon after the underwriter posts a preliminary range for the

price at which IPO shares will be offered in the primary market. The underwriter then uses

this trading information to set the final offer price, but the offer price is never set above the

preliminary range.

• Introductions

Used in the U.K. and continental Europe.

The process: the shares, if they meet the listing requirements, are simply listed on the

exchange and trading begins even though initially no shares are sold.