Nigeria More Vulnerable vs Saudi on Breakeven Oil

•

0 likes•93 views

NIGERIA, SAUDI: after IMF’s caution on GCC’s rising fiscal break-even oil price, note greater vulnerability of Nigeria, compared to Saudi, to falling oil p & QE taper. Particularly given its equities have outperformed. Last year: MSCI Nigeria +31% vs Saudi +24%, Frontier +20%. See attached Frontier Alpha graphic.

Recommended

More Related Content

Viewers also liked

Viewers also liked (15)

Similar to Nigeria More Vulnerable vs Saudi on Breakeven Oil

Similar to Nigeria More Vulnerable vs Saudi on Breakeven Oil (20)

Recently uploaded

Recently uploaded (20)

Nigeria More Vulnerable vs Saudi on Breakeven Oil

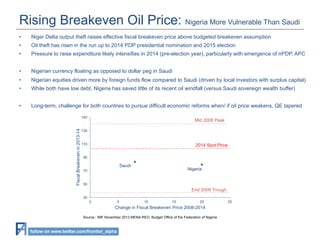

- 1. Rising Breakeven Oil Price: Nigeria More Vulnerable Than Saudi • Niger Delta output theft raises effective fiscal breakeven price above budgeted breakeven assumption • Oil theft has risen in the run up to 2014 PDP presidential nomination and 2015 election • Pressure to raise expenditure likely intensifies in 2014 (pre-election year), particularly with emergence of nPDP, APC • Nigerian currency floating as opposed to dollar peg in Saudi • Nigerian equities driven more by foreign funds flow compared to Saudi (driven by local investors with surplus capital) • While both have low debt, Nigeria has saved little of its recent oil windfall (versus Saudi sovereign wealth buffer) • Long-term, challenge for both countries to pursue difficult economic reforms when/ if oil price weakens, QE tapered Fiscal Breakeven in 2013-14 150 Mid 2008 Peak 130 110 2014 Spot Price 90 Saudi Nigeria 70 50 End 2008 Trough 30 0 5 10 15 20 25 Change in Fiscal Breakeven Price 2008-2014 Source:: IMF November 2013 MENA REO, Budget Office of the Federation of Nigeria follow on www.twitter.com/frontier_alpha

- 2. Frontier Alpha Recent Reports follow on www.twitter.com/frontier_alpha Bangladesh Unrest Priced In 27 October 2013 Nigeria Political Risks Not Priced In 23 September 2013 Zimbabwe Election to Succession 4 August 2013 Egypt Stalemate Broken 4 July 2013 Egypt Value in Distress 22 June 2013 Kuwait Elections and Tribe 17 June 2013 Zimbabwe Value Despite the Run and Risks 10 June 2013 Nigeria, Kenya Northern Rocks 21 May 2013 Saudi Dune 9 June 2013 Pakistan Evolution, Not Revolution Yet 13 May 2013 Saudi CMA, Government at Euromoney 7 May 2013 Zimbabwe Rally Through the Risks 2 May 2013 Saudi Margins Reveal Top Down Risk 22 April 2013 Pan-Frontier Arab Spring: Pakistan Pointer 9 April 2013 Ethiopia Merits More Attention 8 April 2013 Nigeria 2015 Calculus 2 April 2013 Egypt US Disengagement 26 March 2013 Lebanon, Syria Pessimism Put 25 March 2013 Kenya Sensitive Moment 21 March 2013 Dubai Different This Time Why? 13 March 2013 Qatar LNG: Less No Risk Growth 11 March 2013 Egypt CoupE2? 7 March 2013 MENA Persian and Arabian Gulf 6 March 2013 Saudi Old versus New Media 24 February 2013 Saudi Regulator Changes 23 February 2013 Egypt Not (Quite) Pakistan 22 February 2013 Pakistan Balochistan Vortex 21 February 2013 Bahrain Drain 14 February 2013 Saudi Still a Play on Global 12 February 2013 Kuwait Deteriorates Again 10 February 2013 Disclaimer Frontier Alpha provides professional independent research services. Frontier Alpha does not make recommendations on listed securities and is not a regulated entity. The conclusions and opinions expressed in the research accurately reflect the views of Frontier Alpha. While the information in the research is believed to be correct, this cannot be guaranteed. Frontier Alpha or the analysts responsible for this research do not own shares in the companies mentioned. They do not hold any other securities or derivatives (including options and warrants) in these companies. Frontier Alpha does not transact corporate finance and therefore does not earn corporate finance fees. It does not buy or sell shares, and does not undertake investment business anywhere globally. Our research is issued in good faith but without legal responsibility and is subject to change or withdrawal without notice. This research is provided for the use of the professional investment community, market counterparties and sophisticated and high net worth investors as defined in the rules of the regulatory bodies. It is not intended for unsophisticated investors. This research is not an offer to buy or sell any security. Past performance is not necessarily a guide to the future and the price of shares, and the income derived from them, may fall as well as rise and the amount realized might be less than the original sum invested. The risk of shares in Frontier markets may be higher than those in more developed markets. Furthermore the marketability of these shares is often restricted. Our documents must not be accessed or used in any way that would be illegal in any jurisdiction. In some cases research is only issued electronically and in some cases printed research will be received by those on our distribution lists later than those receiving research electronically. Reports may not be reproduced either whole or in part and Frontier Alpha accepts no liability whatsoever for the actions of third parties in this respect.