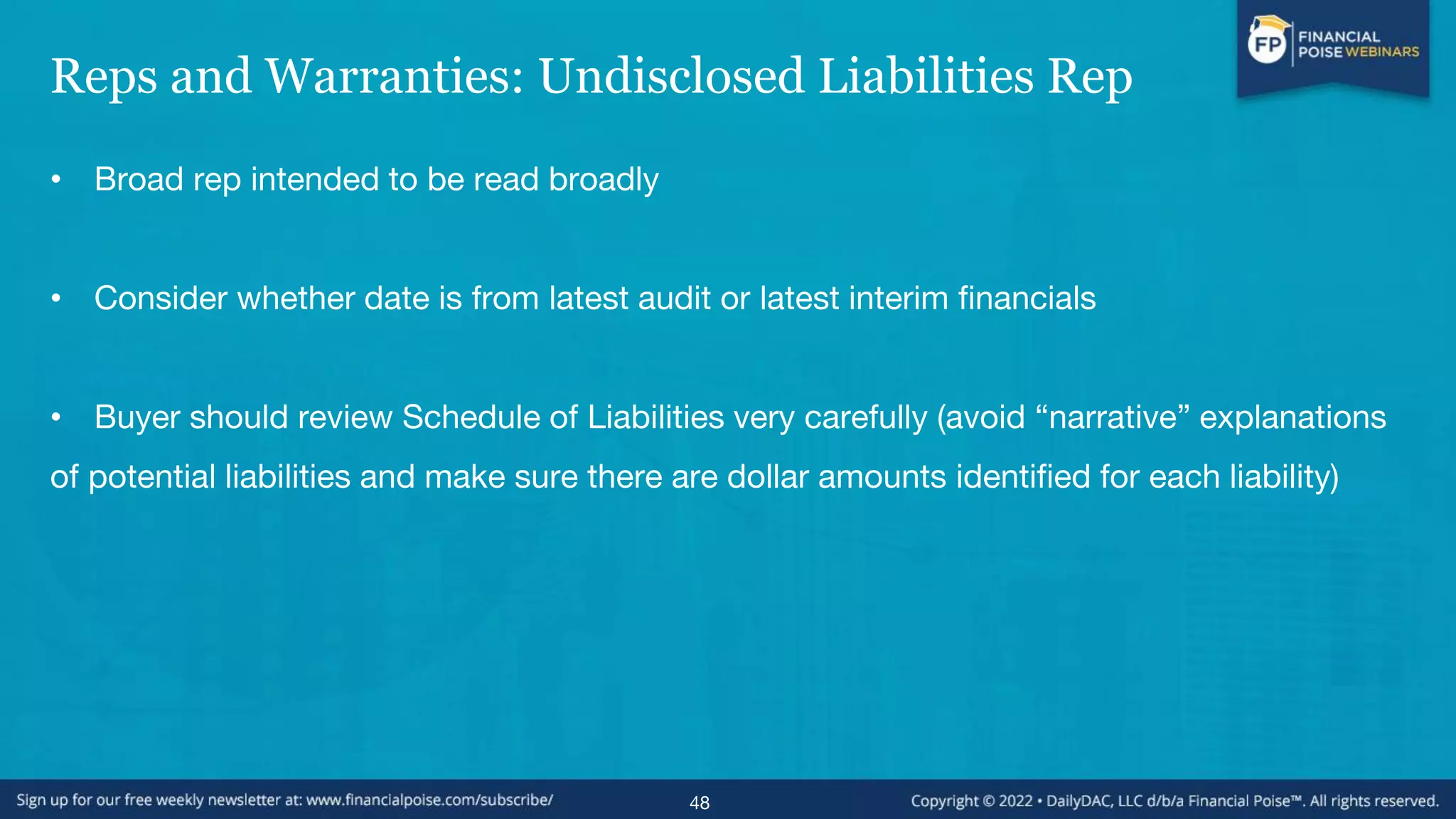

![Reps and Warranties: Undisclosed Liabilities Rep

(cont’d)

• Seller’s Perspective

✔ Seller should not guarantee the collection efforts of Buyer; or guarantee accounts

receivable (perhaps to the extent beyond a reserve set forth in financial statements (see

below))

✔ All accounts receivable of the Seller (i) represent valid obligations of customers of Seller

arising from bona fide transactions entered into in the ordinary course of business, (ii) are

current, [and (iii) are fully collectible, subject to any allowance for doubtful accounts.]”

50](https://image.slidesharecdn.com/1mabootcamp2022-structuringandplanningthematransaction1-220917190544-ba956ac6/75/Structuring-and-Planning-the-M-A-Transaction-50-2048.jpg)

This document outlines a webinar series on structuring and planning M&A transactions, emphasizing the importance of careful planning and understanding various deal aspects. It covers key topics such as transaction structures, tax implications, representations, warranties, and the roles of buyers and sellers. The first episode sets the stage for subsequent discussions aimed at educating attorneys, business owners, and professionals involved in private company mergers and acquisitions.